1. What are the major growth drivers for the Irrigation Industry in India market?

Factors such as Need for Custom Product Development; Use of CROs for Regulatory Services are projected to boost the Irrigation Industry in India market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

Irrigation Industry in India

Irrigation Industry in India+1 2315155523

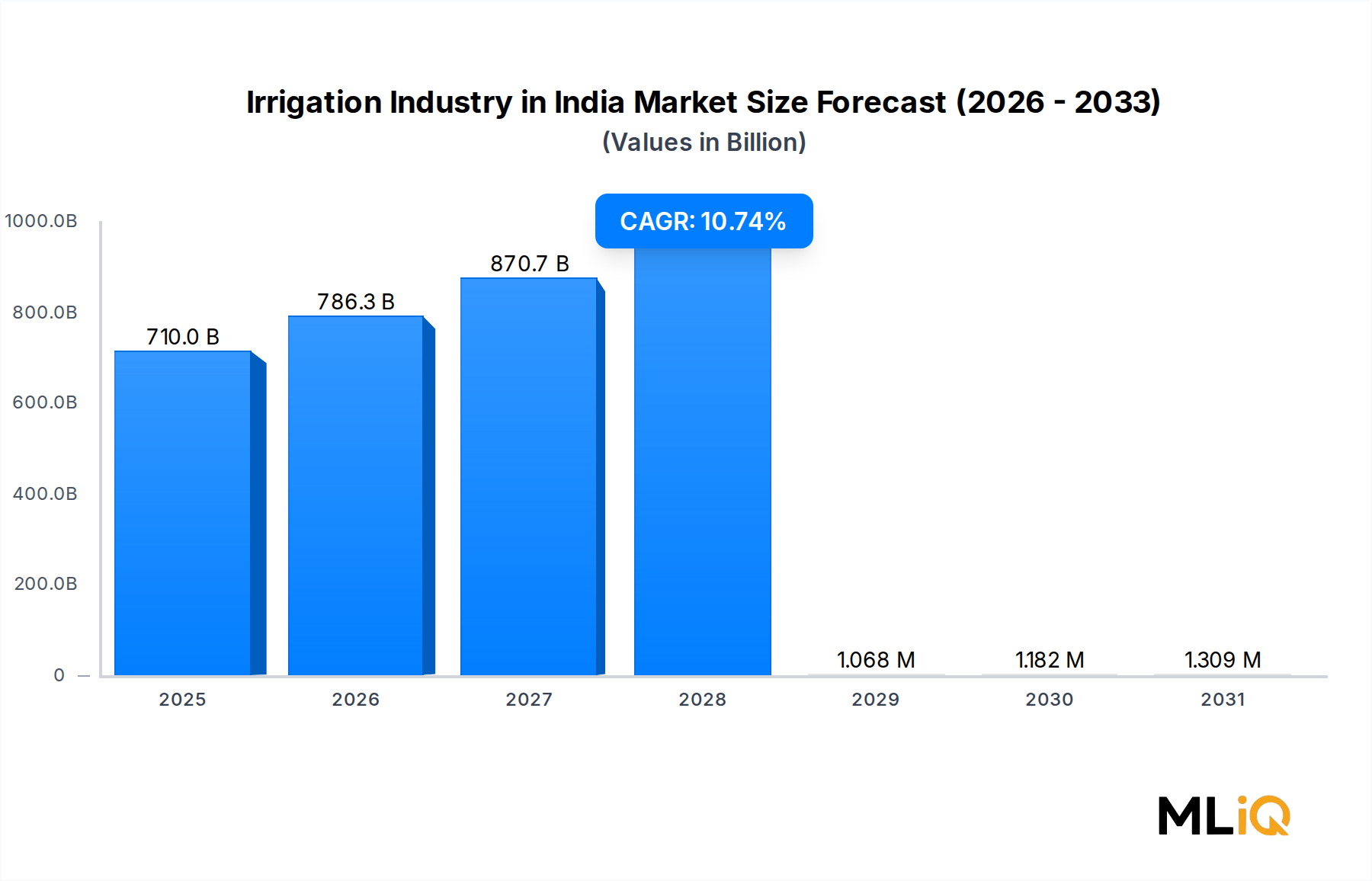

The Irrigation Industry in India Market is positioned at a pivotal inflection point, underpinned by structural demand from the country's expansive agricultural base, government-led infrastructure commitments, and accelerating adoption of water-efficient technologies. As of the base assessment period, the market is valued at approximately $710 billion (in terms of total addressable sector scope inclusive of public and private capital deployed), and is forecast to expand at a compound annual growth rate (CAGR) of 10.74% through the 2025–2033 forecast window. This trajectory reflects both the urgency of water conservation and the scale of modernization investment flowing into Indian agriculture.

India commands the world's largest irrigated area, yet irrigation efficiency remains structurally low — flood and furrow techniques still dominate significant portions of agricultural land. This inefficiency gap creates a powerful economic imperative. Government initiatives such as the Pradhan Mantri Krishi Sinchayee Yojana (PMKSY) and the "More Crop Per Drop" sub-program continue to channel substantial budgetary allocations toward micro-irrigation infrastructure, directly stimulating demand for drip and sprinkler systems at the farm level.

Key demand drivers include the escalating incidence of erratic monsoon patterns, growing water stress across peninsular and semi-arid zones, and the demonstrated yield improvement — often ranging between 20% and 50% — attributable to precision irrigation versus traditional methods. Subsidy frameworks offered by the National Mission for Sustainable Agriculture (NMSA) further incentivize smallholder adoption, particularly in states like Maharashtra, Rajasthan, and Gujarat.

On the supply side, the market is witnessing rapid integration of sensor-based automation, IoT-enabled scheduling platforms, and satellite-guided water management systems, all of which command higher average selling prices and expand the total revenue pool beyond hardware alone. The convergence of the Drip Irrigation Market and precision agri-tech is reshaping competitive dynamics, attracting both multinational players and domestic startups.

Macro tailwinds — including rising food demand from a population projected to exceed 1.5 billion, climate-adaptation urgency, and expanding export-oriented horticulture — reinforce a sustained growth narrative. Corporate investment in R&D, strategic mergers, and new product launches (detailed in subsequent sections) signal that incumbents and new entrants alike are competing aggressively for market share.

Looking ahead to 2033, the Irrigation Industry in India Market is expected to consolidate around technology-differentiated offerings, with smart automation, fertigation integration, and data-analytics platforms emerging as primary growth vectors. The transition from volume-based market expansion to value-based service ecosystems will define the competitive frontier across the forecast period.

Within the Irrigation Industry in India Market, the drip irrigation segment stands out as the largest revenue-generating mechanism type, commanding a disproportionate share of both government subsidy allocations and private capital investment. The segment's dominance is rooted in agronomic performance, policy alignment, and scalable commercial infrastructure built over more than two decades.

Drip irrigation operates by delivering water directly to the root zone of plants through a network of emitters, laterals, and mainlines, achieving field application efficiencies of 85%–95% compared to 40%–60% for surface irrigation methods. This efficiency advantage is not merely theoretical — measurable crop yield improvements, reduction in weed proliferation, and decreased fertilizer leaching make the economic case compelling for farmers cultivating high-value crops such as sugarcane, cotton, grapes, pomegranates, and vegetables.

Maharashtra remains the epicenter of drip adoption in India, owing to its water-scarce geography and the state government's aggressive subsidy disbursements. Karnataka, Andhra Pradesh, Telangana, and Gujarat collectively constitute the next tier of adoption density. In these states, drip systems are deeply integrated into plantation crops, orchards, and vineyards — segments where return on irrigation investment is highest and where the Drip Irrigation Market commands premium pricing.

Jain Irrigation Systems Ltd is unequivocally the market leader in this segment, leveraging its vertically integrated manufacturing base spanning pipes, emitters, filters, and fertigation equipment, alongside an extensive dealer and after-sales service network. The company's June 2022 merger with Rivulis to form a global irrigation and climate leader further solidified its technological and geographic reach. Netafim, the Israeli multinational, operates as the second most significant player, bringing precision drip technology and agronomic advisory services tailored to large-scale and commercial growers. Mahindra EPC Industries Ltd also maintains a strong drip irrigation portfolio, benefiting from its parent conglomerate's distribution infrastructure.

Domestic challengers such as Finolex Plasson Industries Pvt Ltd and Kothari Agritech Pvt Ltd compete aggressively on price points targeted at smallholder segments, where affordability determines adoption rates more than technological sophistication. Avanijal Agri Automation Pvt Ltd and Agsmartic Technologies Pvt Ltd are emerging competitors integrating smart sensing and automation into drip system design, targeting the premium farmer segment.

The segment's market share is not merely holding — it is consolidating. Subsidy reforms have increasingly tilted disbursements toward drip over flood irrigation as state governments face mounting groundwater depletion data. The Sprinkler Irrigation Market, while the second-largest mechanism segment, struggles to match drip's water efficiency metrics in many crop categories, reinforcing drip's primacy.

Future growth within the drip segment will be catalyzed by fertigation adoption — where soluble nutrients are co-applied with irrigation water — and the integration of automated scheduling based on soil moisture sensors. These value-added layers increase system-level revenue per installation significantly, creating a natural upselling pathway for established players. As subsidy penetration deepens into eastern and central India — regions where drip adoption remains nascent — the segment's geographic expansion runway remains substantial through 2033.

The growth trajectory of the Irrigation Industry in India Market is shaped by a constellation of quantifiable drivers operating alongside structural constraints that temper pace and uniformity of expansion.

On the demand-driver side, government policy is the most potent force. The PMKSY has allocated over ₹93,068 crore across its integrated program phases, with a specific sub-component — Per Drop More Crop — dedicated to micro-irrigation expansion. This fiscal commitment has directly enabled adoption among marginal farmers who would otherwise face prohibitive upfront capital barriers. The subsidy can cover 45%–55% of installation cost for small and marginal farmers, materially lowering the payback period.

Custom product development has emerged as a secondary but accelerating driver. As articulated in the report data, the need for tailored solutions — crop-specific emitter designs, terrain-adapted layout configurations, and climate-responsive scheduling algorithms — is pulling manufacturers toward modular, configurable product architectures. This trend is particularly evident in the integration of CRO (contract research organization)-style service models for precision agri-analytics, mirroring pharmaceutical industry outsourcing structures. Manufacturers leveraging these customization capabilities command 15%–25% price premiums over commodity system suppliers.

Greenhouse cultivation expansion is a documented trend driving the market. India's protected cultivation area has grown materially, and greenhouse environments require precision irrigation to optimize humidity, nutrient delivery, and crop uniformity. This sub-use case commands higher-specification equipment and recurring service contracts, boosting per-farm revenue. The intersection with the Greenhouse Horticulture Market is commercially significant, as these installations typically deploy drip and mist systems at above-average system complexity and value.

On the constraint side, data and cybersecurity concerns are increasingly relevant as IoT-enabled smart irrigation systems proliferate. Farm-level sensor networks, cloud-based scheduling platforms, and satellite-integrated management tools create data exposure risks that both enterprise buyers and government procurement agencies are beginning to scrutinize. Lack of robust cybersecurity frameworks for agricultural IoT deployments represents a regulatory and reputational risk that could slow Smart Irrigation Technology Market adoption in institutional channels.

The shortage of trained agronomists, irrigation engineers, and field technicians capable of installing, calibrating, and maintaining advanced systems constrains deployment velocity, particularly in remote agricultural zones. This skills gap is a structural restraint that no subsidy program directly addresses, creating a bottleneck between product availability and functional adoption.

The Irrigation Industry in India Market features a competitive landscape comprising multinational technology leaders, large domestic conglomerates, mid-tier specialists, and agile startups. The following profiles capture each player's strategic positioning:

Jain Irrigation Systems Ltd: The undisputed domestic market leader with vertically integrated manufacturing across pipes, emitters, fittings, and agri-services. Its 2022 merger with Rivulis expanded its global footprint and added satellite-based precision tools to its portfolio.

Netafim: The Israeli precision irrigation giant operates in India through a dedicated subsidiary, focusing on technology-intensive drip and sprinkler solutions for commercial horticulture and field crops. Its AlphaDisc filter launch and Flexi Sprinkler Kit signal continued R&D investment in the Indian market.

Avanijal Agri Automation Pvt Ltd: A technology-forward domestic player specializing in automated irrigation controllers and smart water management systems, targeting precision agriculture applications in horticulture and greenhouse cultivation.

Agsmartic Technologies Pvt Ltd: Focuses on integrating agri-tech software with physical irrigation hardware, positioning itself at the intersection of the Smart Irrigation Technology Market and conventional infrastructure deployment.

Kothari Agritech Pvt Ltd: A mid-tier specialist in drip and sprinkler system components, maintaining competitive pricing to serve smallholder farmers across central and western India.

Finolex Plasson Industries Pvt Ltd: Leverages Finolex's established pipe manufacturing heritage to supply irrigation fittings and drip components, competing primarily on supply chain scale and distribution reach.

Blurain: An emerging player focused on solar-powered and low-energy irrigation solutions, catering to off-grid rural farming communities where energy access constraints limit conventional system adoption.

Ecoflo India: Specializes in sustainable water management and subsurface drip systems, targeting environmentally focused agricultural enterprises and export-oriented farms.

Niagara Automation & Company: Provides automation and control systems for large-scale irrigation infrastructure, particularly in government-sponsored canal command area modernization projects.

Galcon: An international automation specialist with a presence in India's smart irrigation segment, offering programmable controllers and IoT-enabled water management hardware.

Flybird Farm Innovations Pvt Ltd: A startup leveraging mobile-controlled irrigation technology for smallholder farmers, competing in the entry-level smart irrigation tier with affordable GSM-based controllers.

Mahindra EPC Industries Ltd: Backed by the Mahindra conglomerate, this player combines drip and sprinkler system manufacturing with EPC project execution capabilities for large government and commercial contracts.

June 2022: Jain Irrigation Systems Ltd completed its merger with International Irrigation Business Rivulis, creating a combined global irrigation and climate solutions leader with significantly expanded R&D capabilities, manufacturing footprint, and technology portfolio spanning precision drip, sprinkler, and digital water management.

December 2021: Netafim India unveiled the Flexi Sprinkler Kit, a purpose-engineered field crops sprinkler irrigation system designed for broad-acre deployment. The company targeted coverage of 15,000 hectares and outreach to 15,000 farmers across India within the launch year, signaling a strategic push into the field crops segment beyond its traditional horticultural stronghold.

August 2021: Rivulis Irrigation India Ltd launched 'Manna,' a satellite-based software solution enabling growers to optimize irrigation scheduling and water management through remote sensing data integration. This launch positioned Rivulis at the forefront of the Smart Irrigation Technology Market convergence within Indian agriculture.

May 2021: Netafim Limited introduced the AlphaDisc Filter, a filtration innovation designed to prevent clogging from organic contaminants within irrigation systems. The product supports uniform water distribution across drip networks, directly improving crop productivity metrics for adopting farmers. This launch reinforced Netafim's strategy of selling complete system solutions rather than standalone hardware components.

The Irrigation Industry in India Market exhibits pronounced regional heterogeneity driven by agro-climatic conditions, crop mix, state government subsidy intensity, and water scarcity profiles.

Maharashtra is the most mature and highest-revenue state market, accounting for an estimated 25%–30% of national micro-irrigation installations. Its semi-arid geography, high concentration of water-intensive crops (sugarcane, grapes, pomegranates, onions), and a long history of state subsidy programs have created a deeply penetrated market where growth is now driven by system upgrades and precision technology overlays rather than first-time adoption.

Rajasthan is the fastest-growing state market within the irrigation modernization framework, propelled by acute groundwater depletion, desert-fringe agriculture, and significant PMKSY fund disbursements. The state's vast agricultural area and rising horticulture aspirations create a high-volume addressable market for drip and sprinkler systems. Adoption rates among smallholders are accelerating as subsidy accessibility improves through digital disbursement mechanisms.

Andhra Pradesh and Telangana collectively represent a high-growth cluster, particularly for field crops irrigation (cotton, chili, turmeric) and plantation crops. Both states have maintained active subsidy programs and have become significant testing grounds for satellite-based and IoT-enabled smart irrigation deployments. Their combined contribution to the national market is estimated in the 15%–20% range.

Gujarat and Karnataka are established, mid-maturity markets with strong horticultural orientations — Gujarat in cotton and groundnut, Karnataka in floriculture, coffee, and spices. Both states demonstrate consistent year-on-year growth in micro-irrigation coverage, with Gujarat being a notable early adopter of solar-powered pump-drip integrated systems.

Tamil Nadu and Madhya Pradesh represent the emerging tier. Tamil Nadu's rice-paddy dominance has historically limited micro-irrigation penetration, but shifting crop patterns toward horticulture and the state's progressive agri-infrastructure investments are changing the calculus. Madhya Pradesh is emerging as a major soybean and wheat belt where large-scale sprinkler adoption is gaining momentum with central government support.

The Rest of India — encompassing northeastern states, eastern India (Bihar, Odisha, Jharkhand), and Uttar Pradesh — constitutes the highest-potential underpenetrated market. Low historical adoption, lack of dealer infrastructure, and subsidy access complexity have constrained growth, but structured government intervention and private-sector channel development initiatives are progressively opening these geographies to volume-scale deployment.

The Irrigation Industry in India Market has attracted a diversifying mix of capital flows — M&A consolidation at the multinational tier, venture investment at the agri-tech startup layer, and public sector capital through government program disbursements.

The most structurally significant M&A event of the recent period was the June 2022 merger of Jain Irrigation's international irrigation business with Rivulis, creating one of the world's largest dedicated irrigation companies. This transaction reflects a global consolidation thesis: as water scarcity intensifies internationally, scale economies in R&D, manufacturing, and distribution become decisive competitive advantages. For the Indian market specifically, the combined entity brings enhanced satellite analytics and precision water management tools that complement Jain's existing dominance in hardware supply.

At the venture capital and startup investment layer, agri-tech platforms intersecting with irrigation — particularly those targeting the Precision Agriculture Market and Smart Irrigation Technology Market — have attracted meaningful funding. Investors are backing companies that offer subscription-based water management services, soil moisture intelligence platforms, and mobile-controlled irrigation controllers, recognizing recurring revenue potential that transcends hardware margin cycles.

The sub-segments attracting disproportionate capital attention include: IoT-enabled irrigation automation (given hardware-to-software margin expansion potential), solar-integrated pump-drip

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.74% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as Need for Custom Product Development; Use of CROs for Regulatory Services are projected to boost the Irrigation Industry in India market expansion.

Key companies in the market include Jain Irrigation Systems Ltd, Netafim, Avanijal Agri Automation Pvt Ltd, Agsmartic Technologies Pvt Ltd, Kothari Agritech Pvt Ltd, Finolex Plasson Industries Pvt Ltd, Blurain, Ecoflo India, Niagara Automation & Company, Galcon, Flybird Farm Innovations Pvt Ltd, 1 Mahindra EPC Industries Lt.

The market segments include Mechanism Type, Application Type, End Users, States Analysis.

The market size is estimated to be USD 710 billion as of 2022.

Need for Custom Product Development; Use of CROs for Regulatory Services.

Increase in Greenhouse Cultivation is Driving the Market.

Data and Cyber Security Concerns; Lack of Experts and Professionals in this Industry.

June 2022: Jain Irrigation has merged with International Irrigation Business Rivulis to create a global Irrigation and climate leader.

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Irrigation Industry in India," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Irrigation Industry in India, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.