1. What are the major growth drivers for the Coffee Beans Market market?

Factors such as are projected to boost the Coffee Beans Market market expansion.

+1 2315155523

Coffee Beans Market

Coffee Beans Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

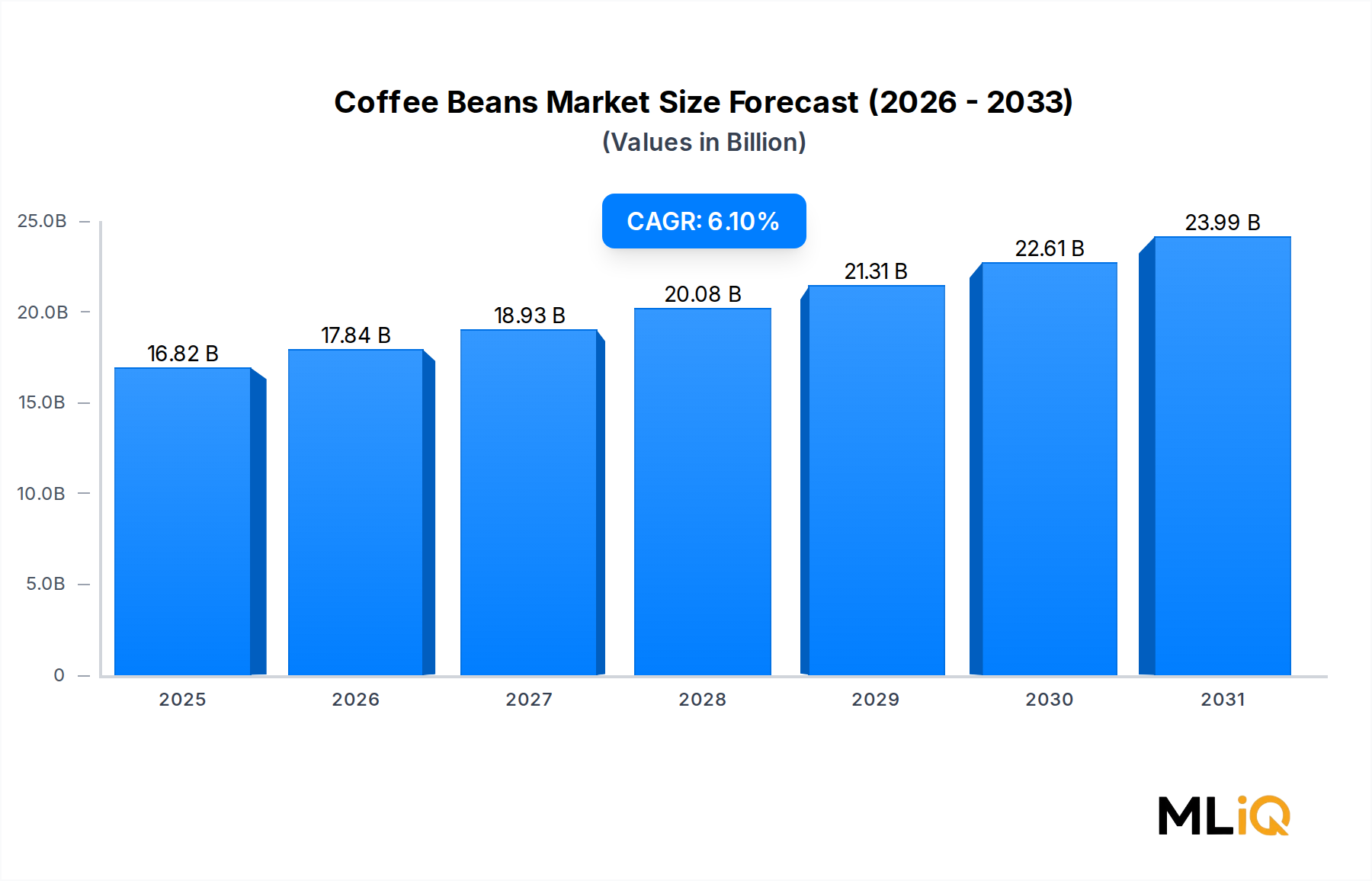

The global Coffee Beans Market is valued at $16,815.56 million as of the base assessment period and is projected to expand at a compound annual growth rate of 6.1% over the forecast horizon. This trajectory reflects robust and broad-based demand across consumer, industrial, and pharmaceutical end-use channels, positioning coffee beans as one of the most strategically significant agricultural commodities in the global food and beverage sector.

Several structural tailwinds are converging to accelerate market expansion. The proliferation of specialty coffee culture across North America, Europe, and emerging Asia Pacific markets has elevated per-capita consumption volumes while simultaneously shifting consumer preferences toward premium, single-origin, and ethically sourced bean variants. Urbanization rates exceeding 55% globally have catalyzed café culture expansion, while at-home brewing adoption—accelerated by pandemic-era behavioral shifts—has created durable demand for whole-bean and ground coffee products at the retail level.

Macroeconomic dynamics further amplify market momentum. Rising disposable incomes in developing economies, particularly across ASEAN nations, India, and Brazil's domestic market, are converting traditional tea-drinking populations into consistent coffee consumers. The global middle class, expected to encompass over 5.3 billion people by 2030, represents a structural demand reservoir that market participants are actively targeting through accessible price-point products and experiential retail formats.

From a supply-side perspective, the dominance of Arabica and Robusta varieties continues to shape production geography, with Brazil, Vietnam, Colombia, and Ethiopia collectively accounting for the majority of global output. However, climate-related disruptions, including irregular rainfall patterns, temperature anomalies, and the spread of coffee leaf rust, are introducing volatility into supply chains and exerting upward pressure on farmgate prices.

In terms of application diversity, coffee beans are no longer confined to beverage production. Their incorporation into personal care formulations—leveraging caffeine's vasoconstrictive and antioxidant properties—and pharmaceutical preparations has broadened end-market demand. The food processing segment continues to absorb significant volumes through flavoring agents, confectionery, and dairy blends.

Looking forward, the Coffee Beans Market is poised for sustained growth through 2031, with innovation in processing technologies, sustainable sourcing certifications, and direct-trade models serving as key differentiators. Vertical integration strategies among major roasters and the emergence of precision fermentation in post-harvest processing are expected to reshape competitive dynamics over the medium term.

Within the product segmentation framework of the Coffee Beans Market, Arabica remains the unambiguous revenue leader, commanding an estimated 60–65% of global market value. This dominance is rooted in a combination of organoleptic superiority, consumer brand associations, and the structural preferences of specialty coffee roasters who drive premium pricing power across the value chain.

Arabica beans (Coffea arabica) are cultivated primarily at high altitudes—typically between 600 and 2,200 meters above sea level—across the bean belt nations of Latin America, East Africa, and select Asian highland regions. The sensory profile of Arabica, characterized by lower bitterness, higher acidity, and complex aromatic notes ranging from fruity to floral and nutty, aligns closely with evolving consumer sophistication in mature Western markets. This sensory advantage translates directly into premium pricing, with specialty-grade Arabica fetching farmgate premiums of 20–40% over standard commodity grades on the ICE Futures exchange.

Brazil, the world's largest coffee producer, generates approximately 40% of global Arabica output, supported by its vast cerrado and matas de minas growing regions. Colombia, with its renowned mountain-grown reputation and denomination-of-origin marketing infrastructure, contributes a further 10–12% of Arabica supply. Ethiopia, widely recognized as the genetic birthplace of Coffea arabica, commands disproportionate market influence through its diverse heirloom cultivar portfolio, which underpins the specialty segment's obsession with provenance and traceability.

Key players operating within the Arabica segment include Luigi Lavazza S.P.A, which has built a century-long brand equity around Italian espresso blends heavily weighted toward high-grade Arabica. Illycaffè S.p.A. similarly anchors its entire product portfolio around 100% Arabica sourcing, differentiating through proprietary pressurized packaging and a direct-sourcing model that spans nine origin countries. La Colombe Torrefaction has positioned itself as a craft premium operator, leveraging single-origin Arabica SKUs to capture high-margin specialty retail and food service channels across the United States.

The Arabica segment's share is not merely holding steady—it is actively consolidating as premiumization accelerates. Consumer willingness to pay a quality premium has grown measurably in the post-pandemic era, with retail scanner data from the U.S. and Western Europe indicating that premium coffee segment dollar sales are outpacing volume sales growth by a factor of approximately 1.4x. This decoupling of price and volume growth is a hallmark indicator of premiumization-driven market maturation.

However, the Arabica segment faces structural supply-side vulnerabilities. Climate change projections suggest that suitable Arabica cultivation zones could contract by as much as 50% by 2050 under high-emissions scenarios, according to modeling published by research institutions affiliated with the CGIAR network. This supply risk is prompting leading roasters and commodity traders to invest in climate-resilient Arabica cultivar development, shade-grown agroforestry systems, and geographic sourcing diversification toward emerging origins such as Rwanda, Myanmar, and Honduras.

The competitive response to these pressures is also driving blending innovation, with many mainstream brands quietly increasing Robusta ratios in espresso blends to manage cost structures while maintaining Arabica-forward marketing narratives. This dynamic underscores the strategic importance of the Arabica Coffee Market as the premium anchor of the broader coffee ecosystem, and its ongoing evolution will materially shape pricing, sourcing, and branding strategies across the global value chain through the forecast period.

The Coffee Beans Market is propelled by a well-defined set of quantifiable demand drivers while simultaneously navigating structural constraints that require strategic mitigation.

Primary driver: Premiumization and specialty coffee expansion. The Specialty Coffee Association estimates that specialty coffee now accounts for approximately 55% of total U.S. coffee consumption by volume, up from roughly 40% a decade prior. This category upgrade cycle generates disproportionate revenue growth relative to volume growth, supporting the market's 6.1% CAGR trajectory.

Secondary driver: Emerging market penetration. Coffee consumption growth in Asia Pacific is running at approximately 8–10% annually in key markets such as China and Vietnam's domestic market, compared to the global average. China's coffee shop count surpassed 170,000 outlets as of 2024, making it one of the fastest-expanding café markets globally and a structural volume driver for imported specialty beans.

Tertiary driver: Multi-sector application expansion. End-use diversification into personal care—leveraging caffeine as an active cosmetic ingredient—and pharmaceutical-grade caffeine extraction from spent coffee grounds are creating incremental demand channels beyond traditional beverage applications. This cross-sector penetration adds demand floor stability to an otherwise cyclical agricultural commodity.

Primary constraint: Climate-induced supply volatility. The 2021 Brazilian frost event and subsequent drought cycle reduced Brazilian Arabica output by approximately 25–30% in crop year 2021/22, triggering a spike in ICE Arabica futures to multi-year highs above $2.50/lb. These events highlight the endemic price volatility risk that constrains procurement planning for industrial buyers.

Secondary constraint: Sustainability compliance costs. The European Union Deforestation Regulation (EUDR), effective from 2025, mandates supply chain due diligence for coffee imports, adding compliance cost burdens estimated at $0.03–0.08 per kilogram across the value chain and creating market access barriers for smaller origin producers lacking traceability infrastructure.

Death Wish Coffee: Positions itself as the world's strongest coffee brand, targeting high-caffeine-seeking consumers through direct-to-consumer e-commerce channels and a premium whole-bean portfolio anchored in Robusta-Arabica blends.

Kicking Horse Whole Beans: A Canadian organic and fair-trade certified roaster with strong distribution across North American natural and specialty grocery channels, leveraging sustainability credentials as a core brand differentiator.

La Colombe Torrefaction: A Philadelphia-based craft roaster known for its direct-trade sourcing model and innovation in ready-to-drink coffee formats, competing effectively in both specialty retail and food service segments.

Caribou Coffee: A Minneapolis-based specialty coffee chain and retail brand with significant Midwest U.S. market penetration, operating both licensed café outlets and a growing packaged coffee retail presence.

Luigi Lavazza S.P.A: An Italian heritage brand and one of the world's largest coffee roasters by volume, with a diversified portfolio spanning espresso capsules, whole beans, and professional equipment for the food service sector.

La Colombe Corsica Blend: A flagship SKU within La Colombe's blended espresso line, formulated for high-pressure extraction environments and positioned at premium price tiers within specialty café and retail channels.

Peet's Coffee & Tea: A pioneering specialty coffee roaster based in California, credited with influencing the American specialty coffee movement, maintaining strong brand loyalty and a vertically integrated retail and wholesale model.

Illycaffè S.p.A.: An Italian ultra-premium brand distinguished by its 100% Arabica commitment, proprietary pressurized tin packaging technology, and global restaurant and fine dining channel presence across more than 140 countries.

Coffee Beans International: A B2B-focused green coffee importer and roaster serving industrial food service accounts and private-label customers across North America, competing on supply chain reliability and volume pricing.

Hawaiian Isles Kona Coffee Company: Specializes in Kona-origin and Hawaiian-grown coffee, leveraging geographic denomination premiums and agri-tourism integration to command significant per-unit price premiums in the luxury coffee segment.

March 2024: The European Union formally confirmed the enforcement timeline for the EU Deforestation Regulation applicable to coffee imports, requiring full supply chain geolocation data from all operators placing coffee on the EU market, impacting an estimated €4.5 billion in annual coffee trade flows.

January 2024: ICE Arabica futures surpassed $2.20/lb for the first time since the 2022 supply shock, driven by El Niño-related weather concerns in key Brazilian and Colombian growing regions, signaling renewed commodity price pressure across the value chain.

September 2023: Luigi Lavazza S.P.A announced a multi-year direct-sourcing partnership with cooperatives in Honduras and Peru to secure climate-resilient Arabica supply chains, committing over $15 million in farmer support and agroforestry investment.

June 2023: Illycaffè S.p.A. received B-Corp certification, joining a growing cohort of premium coffee brands formalizing environmental and social governance commitments as a competitive differentiator in sustainability-conscious consumer segments.

February 2023: Peet's Coffee & Tea launched an expanded single-origin whole-bean line targeting the North American specialty retail channel, introducing five new origin SKUs including Ethiopian Yirgacheffe and Colombian Huila variants.

November 2022: Death Wish Coffee secured a new round of growth capital to expand its direct-to-consumer subscription infrastructure, targeting 30% year-over-year revenue growth through digital acquisition channel optimization.

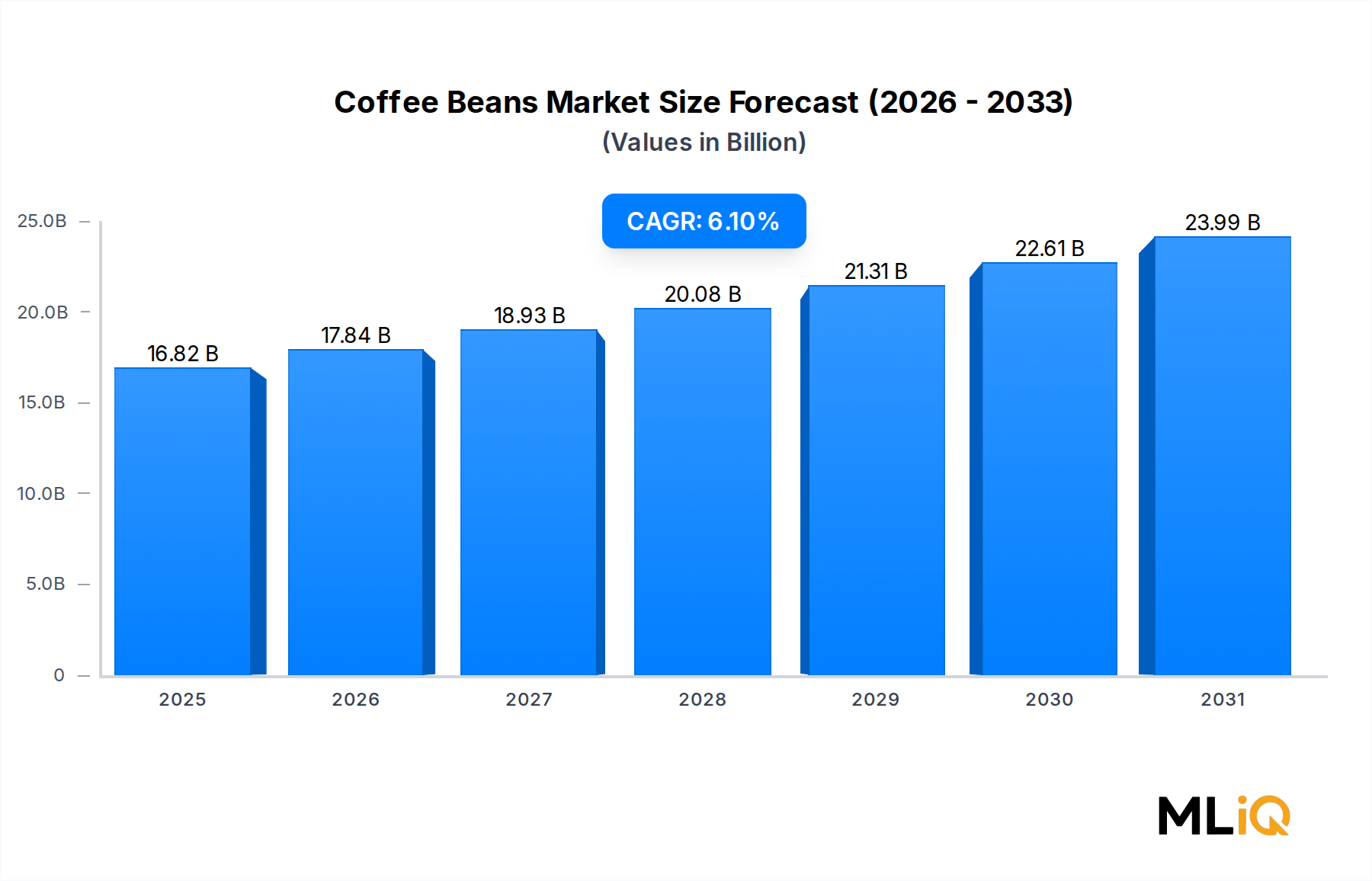

The Coffee Beans Market exhibits distinct regional demand and supply dynamics across five primary geographies, each characterized by differentiated growth rates, consumption patterns, and structural market drivers.

North America represents the most mature regional market, accounting for an estimated 28–30% of global revenue. The United States, as the single largest national consumer market, generates sustained demand through a deeply embedded café culture, a robust at-home premium segment, and continued premiumization of mainstream retail coffee. Regional CAGR is estimated at approximately 4.5–5.0%, reflecting a decelerating but stable growth profile. Canada contributes incrementally through strong specialty coffee adoption in urban centers.

Europe holds a comparable revenue share at approximately 25–27% of global value, with Italy, Germany, France, and the Nordic countries serving as the primary consumption hubs. The European market is characterized by high per-capita consumption—Nordic countries lead globally at over 10 kg per capita annually—and a sophisticated espresso and filter coffee culture. Regional CAGR is estimated at 3.5–4.5%, constrained by demographic maturity but supported by continued premiumization and the EUDR-driven emphasis on certified sustainable sourcing.

Asia Pacific is the fastest-growing regional market, with an aggregate CAGR estimated at 9–11%, driven by China's rapid café sector expansion, India's emerging specialty coffee consumer segment, and continued growth across ASEAN markets including Vietnam, Indonesia, and Thailand. The region is transitioning from a supply-dominant role—Vietnam is the world's second-largest coffee producer—toward a dual role as both major producer and rapidly expanding consumer market.

South America, anchored by Brazil and Argentina, contributes approximately 15–18% of global revenue. Brazil's domestic market has grown significantly, with per-capita consumption rising to approximately 6 kg annually, making it the second-largest consuming nation globally. Regional CAGR is estimated at 5.5–6.5%, supported by domestic income growth and urbanization.

Middle East & Africa presents a high-potential emerging market with CAGR estimated at 7–8%, driven by Gulf Cooperation Council urbanization, Ethiopia's growing domestic consumption, and Turkey's historically robust coffee culture transitioning toward specialty formats.

The Coffee Beans Market operates across a complex, multi-tiered pricing architecture in which commodity-grade benchmarks interact with specialty premiums to produce widely divergent margin structures across the value chain.

At the commodity level, Arabica and Robusta prices are benchmarked against ICE Futures U.S. (contract "C") and the London International Financial Futures Exchange (LIFFE) respectively. These benchmark prices are highly volatile—Arabica spot prices ranged from approximately $0.92/lb to above $2.50/lb across the 2018–2023 period—creating procurement cost volatility that compresses roaster margins during supply shocks. The 2021 Brazilian frost cycle demonstrated how a single climatic event can trigger a +80% price surge within a single crop year, leaving roasters with fixed-price retail commitments exposed to significant margin erosion.

Farmgate-to-export margins in origin countries are typically thin, with smallholder farmers capturing an estimated 5–15% of final retail value in commodity-grade supply chains. Fair trade and direct-trade models partially address this imbalance, transferring incremental value to producers while simultaneously enabling roasters to charge retail premiums of 15–25% for certified products.

At the retail level, specialty coffee commands average selling prices that are 2–4x mainstream commodity coffee on a per-unit basis. This premium segment generates gross margins for roasters in the 45–60% range, compared to 25–35% for mainstream private-label accounts. However, raw material cost volatility, energy costs for roasting operations, and rising logistics expenses are compressing net margins across both tiers.

The rise of private-label coffee in European grocery channels—where retailer own-brand coffee holds 30–40% shelf share in markets such as Germany and the UK—is intensifying price competition in the mainstream segment and forcing branded players to concentrate investment in premium differentiation. Capsule and single-serve format proliferation has partially offset this pressure by creating higher-margin, format-locked revenue streams insulated from direct commodity price comparisons.

The Robusta Coffee Market's cost advantage—Robusta prices trade at a structural discount of 30–50% relative to

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.1% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Coffee Beans Market market expansion.

Key companies in the market include Death Wish Coffee, Kicking Horse Whole Beans, La Colombe Torrefaction, Caribou Coffee, Luigi Lavazza S.P.A, La Colombe Corsica Blend, Peets Coffee & Tea, Illycaff S.p.A., Coffee Beans International, Hawaiian Isles Kona Coffee Company, Ltd.

The market segments include Product, End Use.

The market size is estimated to be USD 16815.56 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3456, USD 5769, and USD 10995 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Coffee Beans Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Coffee Beans Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.