1. What are the major growth drivers for the Green Pepper Market market?

Factors such as are projected to boost the Green Pepper Market market expansion.

Green Pepper Market

Green Pepper Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

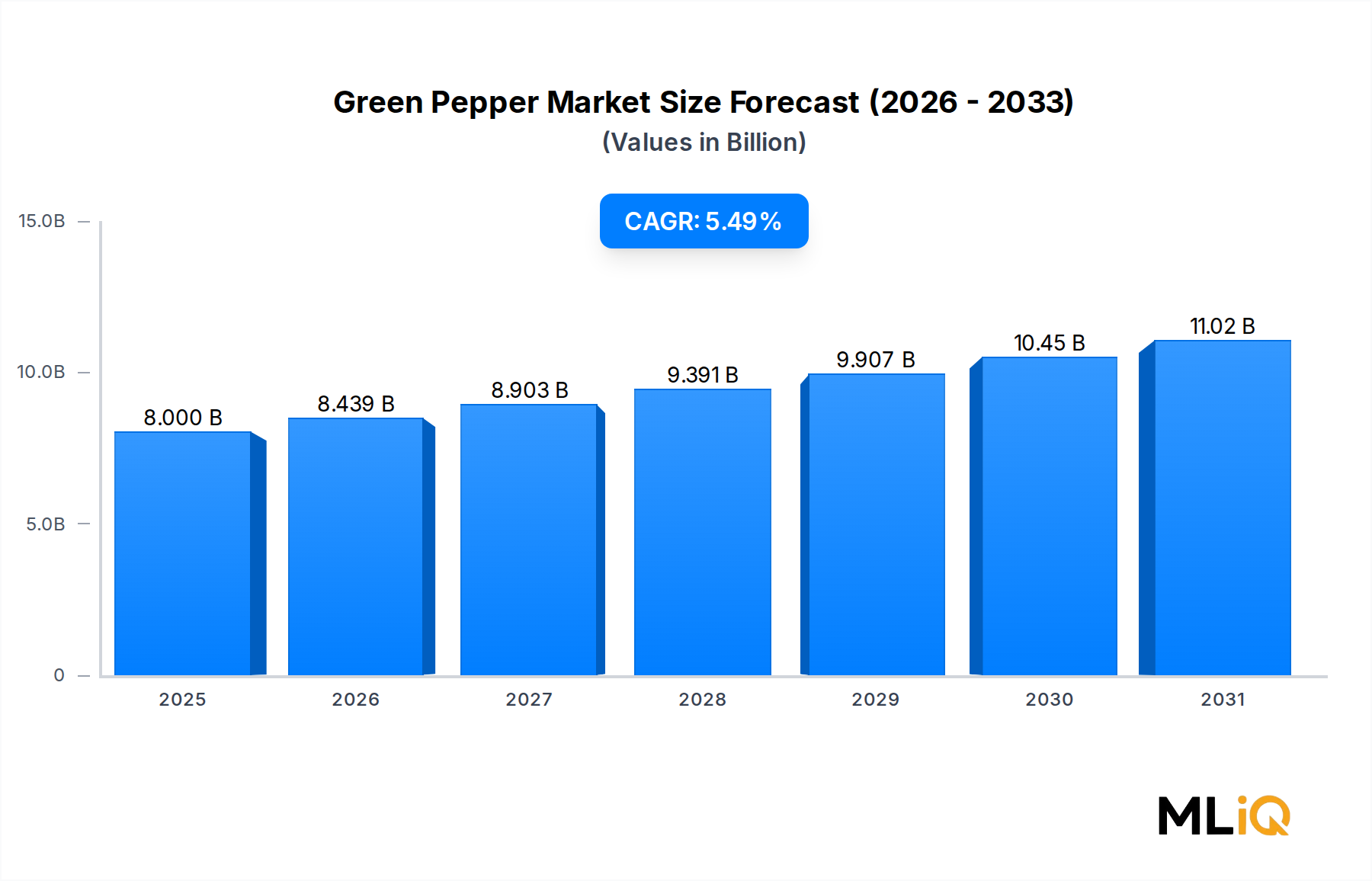

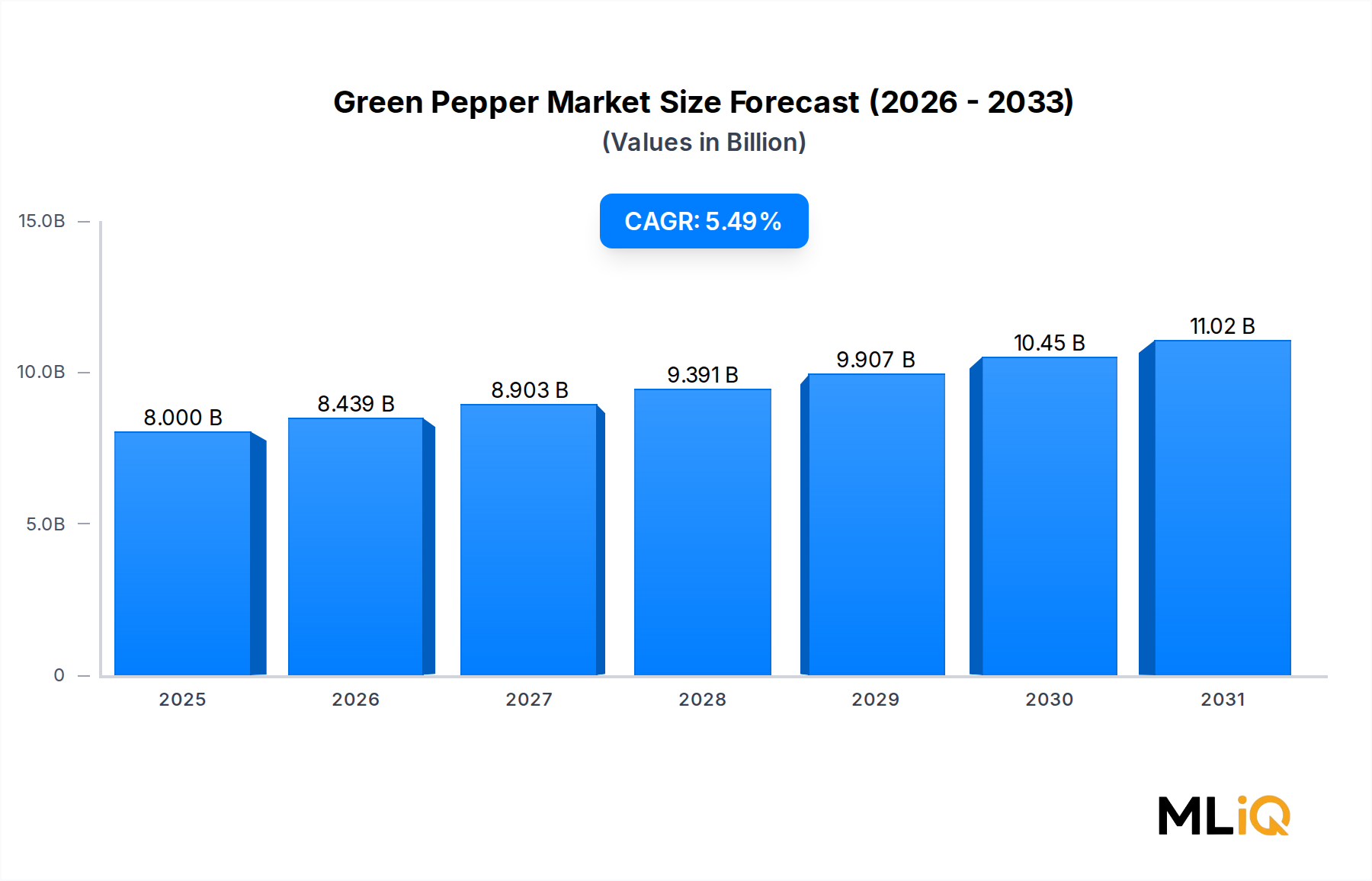

The global Green Pepper Market is valued at $8 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 5.49% through 2033, reflecting robust and sustained demand across culinary, industrial, and pharmaceutical end-use segments. This growth trajectory is underpinned by a confluence of macro-level tailwinds including rising global food consumption, accelerating urbanization, and the expanding influence of ethnic and international cuisines across developed and emerging economies alike.

Green pepper, harvested at an immature stage from the Piper nigrum vine or from Capsicum annuum cultivars, occupies a strategically important position in the global spice and vegetable supply chain. Its distinctive flavor profile — fresher, lighter, and less pungent than black or red pepper — makes it a preferred ingredient in daily cooking, processed food formulations, and increasingly in pharmaceutical applications where capsaicinoid compounds are valued for their bioactive properties.

Demand drivers are multi-dimensional. First, the global food processing industry continues to expand at a pace that outstrips overall GDP growth in several emerging market economies, pulling substantial volumes of green pepper into industrial flavor systems, ready-meal formulations, and condiment manufacturing. Second, health-conscious consumer trends are elevating the status of pepper-derived compounds within the Nutraceuticals Market, where capsaicinoids and antioxidant-rich pepper extracts are being incorporated into dietary supplements and functional food products. Third, the ongoing premiumization of culinary ingredients in North America, Europe, and East Asia is driving demand for specialty and certified-organic green pepper variants, commanding higher per-unit values and widening revenue pools.

From a supply-side perspective, concentrated production in Asia Pacific — particularly India, Vietnam, and China — provides cost-competitive raw material availability, while investments in cold-chain logistics infrastructure are progressively reducing post-harvest losses and enabling longer shelf-life products to reach distant consumer markets. At the same time, climate variability presents a structural risk to consistent supply, reinforcing the need for geographic diversification of sourcing strategies among large-scale buyers.

Looking ahead through 2033, the market is expected to benefit from increased penetration of dried and powdered pepper formats in the institutional food service sector, growing pharmaceutical industry offtake, and expanding e-commerce channels that are democratizing access to premium and specialty pepper products globally. The convergence of these demand vectors positions the Green Pepper Market as a high-growth segment within the broader Food and Beverages category.

Within the type-based segmentation of the Green Pepper Market, the fresh segment commands the largest revenue share and continues to consolidate its leadership position as of 2025. This dominance is attributable to several structural and behavioral factors that collectively reinforce fresh green pepper as the default product form across both retail and institutional procurement channels.

Fresh green pepper benefits from its immediate culinary utility — it requires no rehydration or processing prior to use, making it the preferred choice for daily cooking across residential households, restaurants, hotels, and food service operators worldwide. The sensory attributes of fresh green pepper, including its vibrant color, crisp texture, and bright vegetal flavor, are difficult to replicate in dried or powdered formats, creating a persistent preference premium that sustains volume and value leadership in this sub-segment.

From a distribution standpoint, fresh green pepper is deeply embedded in global supply chains for fresh produce. The Fresh Produce Market infrastructure — encompassing modern retail chains, wet markets, wholesale distribution hubs, and increasingly direct-to-consumer farm box services — provides extensive last-mile accessibility for fresh pepper across both developed and developing economies. In Asia Pacific, where fresh vegetable consumption per capita is among the highest globally, fresh green pepper accounts for a disproportionately large share of total pepper purchases, with China and India representing the two largest national markets by volume.

Key players operating prominently within the fresh segment include Beidahuang Group, which leverages its large-scale agribusiness infrastructure in Northeast China to supply fresh vegetables including pepper varieties to domestic and export markets. Adams Group similarly maintains supply chain capabilities oriented toward fresh vegetable distribution across regional markets. Borges Mediterranean Group, while more diversified across Mediterranean agricultural products, maintains exposure to fresh pepper supply chains through its broader agricultural sourcing network.

The fresh segment's share is not merely stable — it is actively growing in specific high-value sub-channels. Premium and organic fresh green pepper is gaining significant shelf space in specialty grocery retailers across the United States, Germany, the United Kingdom, and Japan, where consumers are willing to pay a meaningful price premium for certified-organic, pesticide-residue-free, or locally sourced variants. This premiumization dynamic is expanding the average selling price within the fresh segment, thereby growing its revenue contribution even in markets where volume growth may be more modest.

However, the fresh segment faces structural constraints related to perishability. Post-harvest losses for fresh green pepper can reach 20–30% in supply chains lacking adequate cold storage and refrigerated transport, particularly in South and Southeast Asian markets. This challenge is driving investment in cold-chain infrastructure by both private operators and government-backed agribusiness development programs, with the dual effect of reducing supply-side losses and enabling market expansion into previously underserved geographies.

The dominance of the fresh segment also has implications for pricing dynamics. Unlike dried or powdered pepper, which can be inventoried and traded as commodities, fresh green pepper prices are highly sensitive to seasonal production cycles, weather events, and transportation disruptions. This volatility creates procurement risk for large food service and processing industry buyers, incentivizing some to diversify sourcing across the fresh and processed formats — a dynamic that modestly supports growth in the dried segment as a complementary hedging mechanism.

The Green Pepper Market's 5.49% CAGR through 2033 is shaped by identifiable drivers and constraints that operate at different intensities across regions and end-use segments.

Driver 1: Expansion of the Global Food Processing Industry. The food processing sector — a primary off-taker of both fresh and dried green pepper for flavor systems, sauces, marinades, and ready meals — has been growing at approximately 4–6% annually in key emerging markets including India, Brazil, and Southeast Asia. This creates a durable industrial demand base that is less cyclical than retail consumer demand. The Food Processing Ingredients Market, which includes pepper-derived compounds, is expanding in lockstep with this trend, providing a structural volume pull for green pepper suppliers.

Driver 2: Rising Health and Wellness Consciousness. Consumer awareness of the bioactive compounds in green pepper — including vitamin C (green pepper contains up to 120 mg per 100g, exceeding orange content), vitamin B6, and capsaicinoids — is driving incorporation into health-oriented food products and supplements. This intersects with broader growth in the Functional Food Ingredients Market, where natural, plant-derived bioactives command significant commercial interest.

Driver 3: Pharmaceutical and Nutraceutical Industry Demand. Green pepper-derived oleoresins and extracts are gaining traction in pharmaceutical formulations for analgesic, anti-inflammatory, and metabolic health applications. This is a high-margin demand vector that complements the commodity-volume dynamics of the food segment.

Constraint 1: Climate and Agricultural Yield Volatility. Green pepper cultivation is sensitive to rainfall patterns, temperature extremes, and soil conditions. El Niño-related weather disruptions have historically caused supply shortfalls of 15–25% in key producing regions, creating price spikes that compress processor margins and dampen demand in price-sensitive markets.

Constraint 2: Regulatory Complexity in Pesticide Residue Standards. Tightening Maximum Residue Levels (MRLs) in the European Union and Japan — two of the world's most stringent regulatory environments — create compliance costs for exporters and can result in shipment rejections, effectively constraining market access for suppliers unable to meet evolving standards.

The competitive landscape of the Green Pepper Market is characterized by a mix of diversified agribusiness conglomerates, regional processing specialists, and vertically integrated agricultural companies. The following profiles capture the strategic positioning of leading participants:

Fuji Vegetable Oil Inc.: A Japan-based agribusiness player with capabilities spanning vegetable oil processing and spice-related ingredient manufacturing, Fuji Vegetable Oil Inc. leverages its processing expertise to serve both domestic Japanese food manufacturers and export markets across Asia.

Bunge Limited: One of the world's largest agribusiness and food companies, Bunge Limited operates across grain and oilseed value chains with diversified exposure to vegetable-derived commodities including pepper-related ingredients, serving industrial food processing clients globally.

Beidahuang Group: A state-owned agribusiness conglomerate based in China's Heilongjiang province, Beidahuang Group brings significant scale in agricultural production and distribution, positioning it as a key upstream supplier of pepper and vegetable products across Asian markets.

Adani Wilmar Ltd.: An Indian joint venture between Adani Group and Wilmar International, Adani Wilmar Ltd. has expanded beyond edible oils into broader food ingredients and spices, capitalizing on India's position as a leading pepper producer and exporter.

Associated British Foods (Ach): Through its grocery and ingredients divisions, Associated British Foods (Ach) maintains exposure to spice and flavor ingredient markets, with supply chain capabilities spanning multiple continents and product categories.

Cargill Inc.: As one of the largest privately held corporations in the United States, Cargill Inc. operates extensive agricultural commodity sourcing, processing, and distribution networks that encompass pepper and related spice ingredients across global food manufacturing supply chains.

Ruchi Soya Industries Ltd: An Indian agribusiness company with a significant presence in edible oils and food products, Ruchi Soya Industries Ltd has diversified into broader food ingredient categories, leveraging its distribution infrastructure across India's large consumer market.

Archer Daniels Midland Company: A global leader in agricultural processing and food ingredient supply, Archer Daniels Midland Company sources, processes, and distributes a wide range of plant-based ingredients including spice derivatives, serving multinational food manufacturers worldwide.

Adams Group: Focused on agricultural commodity distribution and supply chain management, Adams Group operates across fresh and processed vegetable segments, maintaining sourcing relationships with pepper producers in key growing regions.

Borges Mediterranean Group: Specializing in Mediterranean agricultural products including oils, nuts, and spices, Borges Mediterranean Group brings premium positioning and European distribution expertise to the specialty and organic green pepper segments.

January 2024: The European Food Safety Authority (EFSA) updated its Maximum Residue Level guidelines for capsicum-family vegetables including green pepper, tightening chlorpyrifos limits to near-zero thresholds, prompting exporters in India and Vietnam to accelerate transitions to integrated pest management systems.

March 2024: Cargill Inc. announced expanded sourcing agreements with certified-sustainable pepper farms in Vietnam, targeting a 30% increase in its certified-sustainable pepper procurement volume by 2026 as part of its broader agricultural sustainability commitments.

June 2024: India's Agricultural and Processed Food Products Export Development Authority (APEDA) reported a 12% year-over-year increase in green pepper export volumes from India in the fiscal year ending March 2024, driven by strong demand from Middle Eastern and European markets.

September 2024: A major European retail consortium announced new private-label organic green pepper product lines sourced from certified farms in Spain and the Netherlands, reflecting accelerating premiumization trends in the region.

November 2024: Adani Wilmar Ltd. launched a new retail-packaged green pepper product line targeting the Indian urban consumer segment, leveraging its extensive nationwide distribution network across modern trade and e-commerce channels.

February 2025: Research published in the Journal of Agricultural and Food Chemistry identified novel antioxidant compounds in immature Capsicum annuum varieties including green pepper, providing scientific validation for growing nutraceutical industry interest.

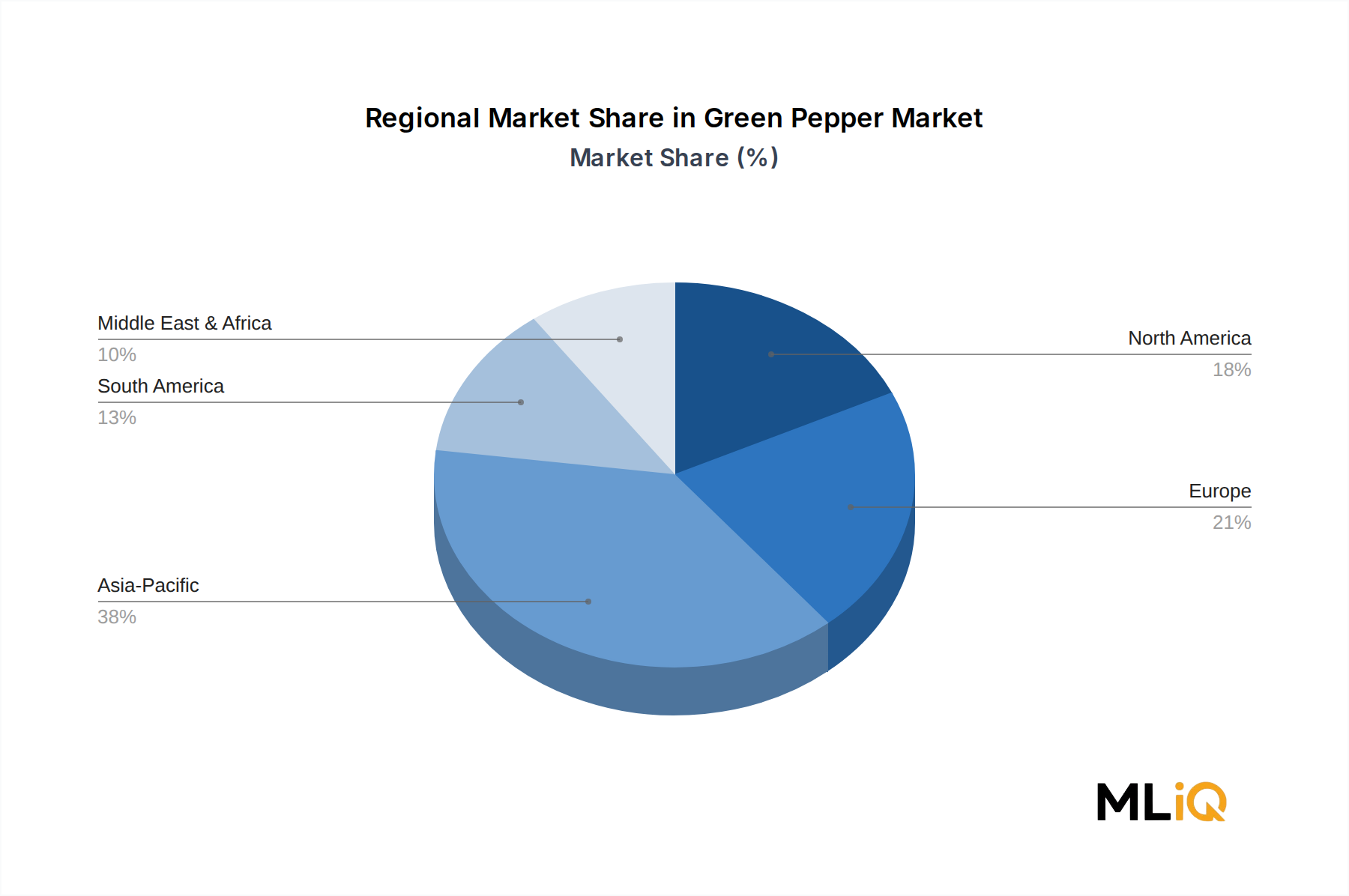

The Green Pepper Market exhibits pronounced regional differentiation in terms of growth rates, demand drivers, and maturity levels, with Asia Pacific occupying the central position in both production and consumption.

Asia Pacific is both the largest and the fastest-growing regional market, accounting for an estimated 42–45% of global revenue in 2025 and growing at a regional CAGR of approximately 6.8% through 2033. China and India together represent the dominant production and consumption centers, with India being the world's largest pepper producer and exporter. Rapid urbanization, a large and growing middle class with expanding food service expenditure, and the deep embedding of pepper in regional cuisines are the primary demand drivers. The Bell Pepper Market within this region is also expanding rapidly, often developed alongside green pepper cultivation infrastructure.

North America represents a mature but steadily growing market, with a regional CAGR estimated at 4.2% through 2033. The United States is the primary national market, driven by the food processing industry's demand for green pepper in sauces, salsas, and ready meals, as well as strong retail demand. The growing Hispanic population is a notable demographic driver, increasing household pepper consumption. The Chili Pepper Market in North America shares supply chain infrastructure with green pepper, and companies operating across both segments benefit from distribution synergies.

Europe holds a significant market share, estimated at approximately 22–24% of global revenue in 2025, with a regional CAGR of approximately 3.8% through 2033, making it the most mature region. Germany, the United Kingdom, France, and Spain are the largest national markets. Demand is underpinned by a sophisticated food processing industry and growing consumer preference for premium and organic pepper products. The Spices and Seasonings Market in Europe is closely linked to green pepper trade flows, with significant intra-European import activity.

Middle East and Africa is an emerging high-growth region with a regional CAGR estimated at 5.9% through 2033, driven by population growth, expanding food retail infrastructure, and strong culinary traditions incorporating pepper. Turkey and GCC countries are key markets.

South America, led by Brazil and Argentina, contributes approximately 8–10% of global revenue, with a CAGR of approximately 5.1% through 2033, supported by domestic production capabilities and growing food processing industry demand.

The customer base of the Green Pepper Market is segmented across four primary end-user categories: residential consumers, food service operators, industrial food processors, and pharmaceutical and nutraceutical manufacturers. Each segment exhibits distinct purchasing criteria, price sensitivity profiles, and procurement channel preferences.

Residential consumers represent the broadest segment by participant count but are highly fragmented and price-sensitive. Purchasing decisions are predominantly driven by freshness, appearance, and price, with brand loyalty relatively low in this segment. Procurement occurs primarily through modern retail (supermarkets, hypermarkets), traditional wet markets, and increasingly through online grocery platforms. A notable behavioral shift in recent cycles is the rising share of organic and certified-sustainable green pepper purchases within the residential segment in developed markets, where premium price tolerance has increased as health consciousness grows. The Capsicum Oleoresin Market indirectly benefits from residential demand for pepper-derived products in packaged foods.

Food service operators — including restaurants, hotels, caterers, and institutional food service providers — prioritize consistency of supply, volume reliability, and product standardization over price minimization. Procurement is typically conducted through contracted wholesale distributors or directly from regional produce wholesalers, with annual or seasonal purchase agreements common among larger operators. This segment has demonstrated strong recovery and growth post-pandemic, driving incremental volume demand.

Industrial food processors are the most procurement-sophisticated segment, with rigorous supplier qualification processes, stringent quality and food safety certifications (including FSSC 22000, BRC, and SQF standards), and multi-year supply contracts. Price negotiation occurs at scale, and buyers frequently diversify sourcing across multiple geographies to manage supply risk. The Vegetable Oil Market and broader food ingredient procurement functions often overlap organizationally within these companies, enabling integrated supplier management.

Pharmaceutical and nutraceutical manufacturers represent a smaller but rapidly growing and high-margin customer segment. Purchasing criteria center on phytochemical standardization, traceability, and compliance with Good Manufacturing Practice (GMP) standards. This segment sources primarily through specialized ingredient distributors and directly from certified extraction facilities, with a preference for documented

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.49% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Green Pepper Market market expansion.

Key companies in the market include Fuji Vegetable Oil Inc., Bunge Limited, Beidahuang Group, Adani Wilmar Ltd., Associated British Foods (Ach), Cargill Inc., Ruchi Soya Industries Ltd, Archer Daniels Midland Company, Adams Group, Borges Mediterranean Group.

The market segments include Type, Application, Form.

The market size is estimated to be USD 8 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Green Pepper Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Green Pepper Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.