1. What are the major growth drivers for the China Pesticide Industry market?

Factors such as Demand For Landscaping Maintenance; Adoption of Green Spaces and Green Roofs are projected to boost the China Pesticide Industry market expansion.

+1 2315155523

China Pesticide Industry

China Pesticide Industry

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

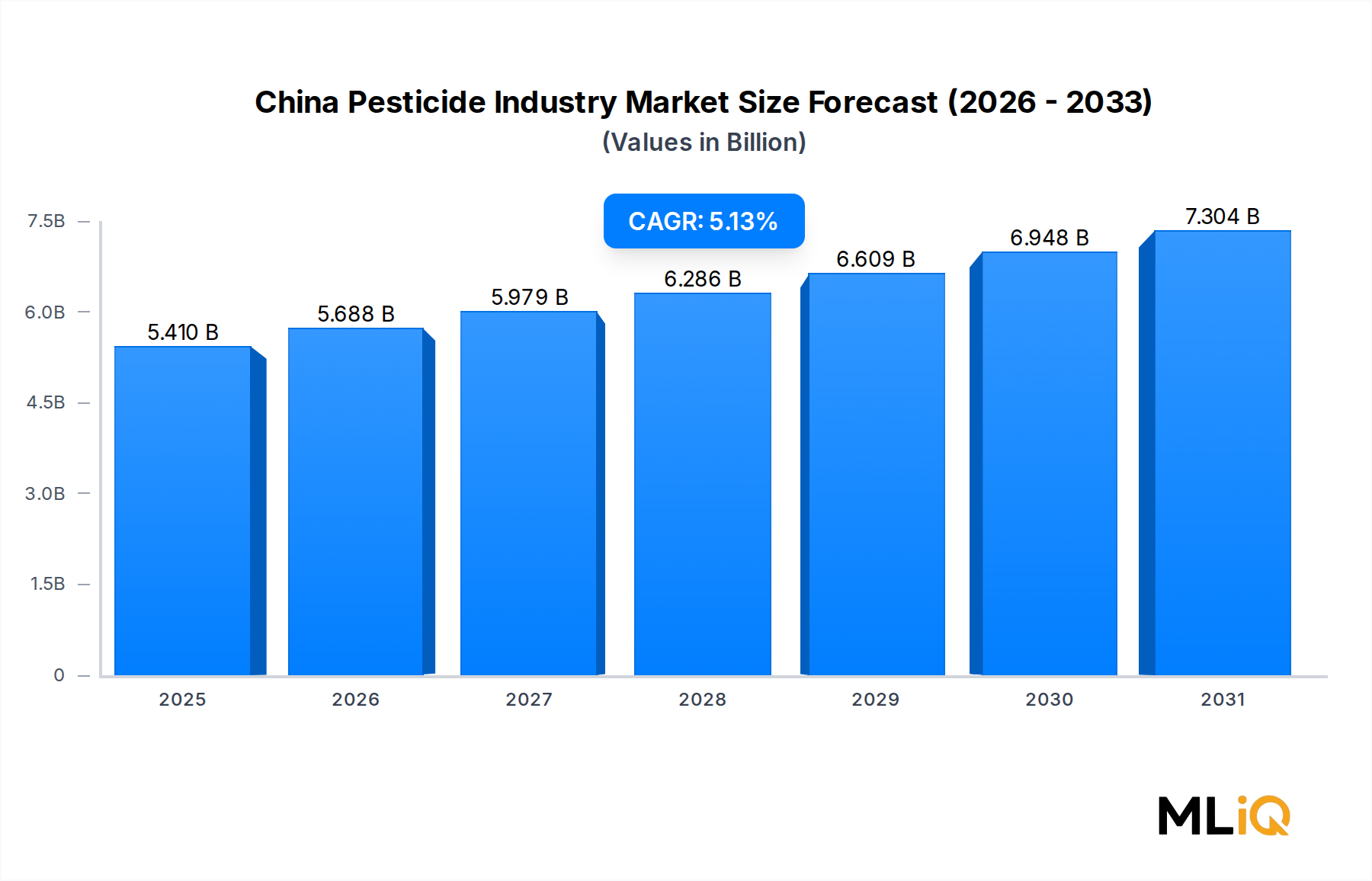

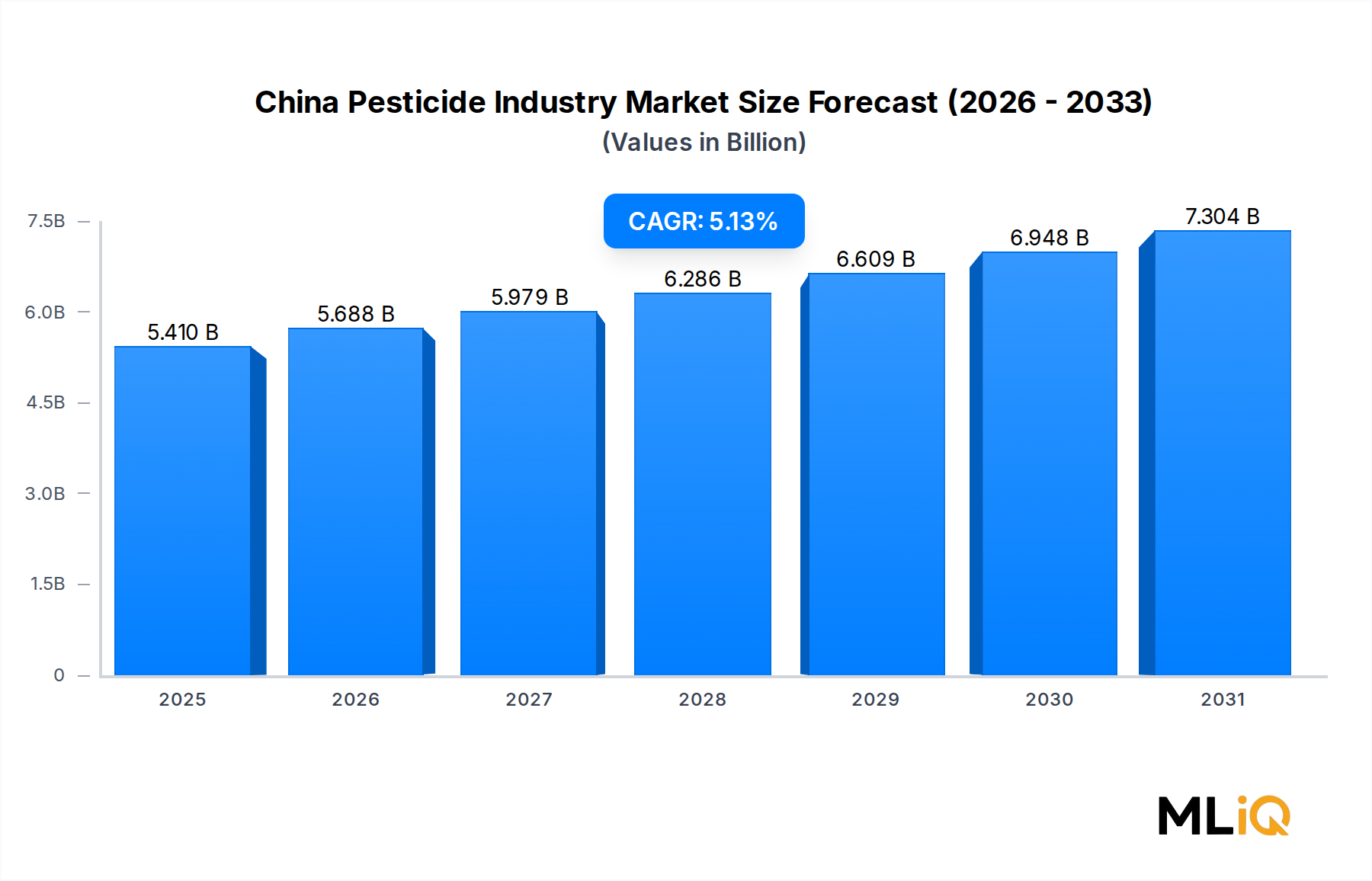

The China Pesticide Industry Market is valued at $5.41 billion as of the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 5.13% over the forecast horizon. China occupies a singular position in the global agrochemical landscape, functioning simultaneously as the world's largest pesticide producer and one of its most significant consumers. This dual role creates a self-reinforcing demand cycle that underpins sustained market expansion even amid tightening environmental regulations.

Several macro tailwinds are propelling the market forward. China's agricultural sector continues to face acute pressure to maximize yields on a shrinking per-capita arable land base — currently estimated at roughly 0.09 hectares per person — making chemical crop protection indispensable for food security. The government's ongoing push to achieve 95% self-sufficiency in staple grains sustains domestic consumption of herbicides, insecticides, and fungicides across vast cereal-growing regions.

Sustained urbanization, at an annual rate approaching 1 percentage point, is simultaneously shrinking the agricultural labor force and catalyzing demand for labor-saving chemigation and foliar spray applications. This transition incentivizes the adoption of formulation technologies that reduce application frequency without compromising efficacy, nudging the product mix toward higher-value, differentiated actives.

Export dynamics add another dimension. China accounts for an estimated 30–35% of global pesticide active ingredient (AI) manufacturing capacity. Tightening environmental inspections, however, have constrained output from smaller, non-compliant facilities, concentrating production among larger registered manufacturers and ultimately supporting domestic price stability for compliant AIs.

On the demand side, the rapid expansion of China's fruit and vegetable acreage — driven by rising per-capita income and dietary diversification — is shifting the end-use mix toward higher-margin specialty crop applications. These segments command premium formulations and create natural upsell opportunities for the leading multinationals and domestic champions operating in the market.

Looking ahead, the market is expected to be shaped by four converging forces: digital precision application technologies that optimize input use; the accelerating registrations of bio-rational and reduced-risk chemistries; consolidation among domestic formulators; and continued regulatory harmonization with international standards for maximum residue limits (MRLs). Together, these forces will bifurcate the competitive landscape between scale-driven commodity producers and differentiated solution providers, with value creation accruing disproportionately to the latter segment through the forecast period.

Within the China Pesticide Industry Market, herbicides represent the single largest functional segment by revenue share, a position that is both structurally entrenched and still marginally expanding. This dominance reflects the intersection of China's crop mix, labor economics, and the global competitiveness of Chinese glyphosate and paraquat substitute producers.

China cultivates approximately 120 million hectares of arable land, a large proportion of which is planted to labor-intensive row crops — rice, wheat, corn, and soybeans — where weed pressure directly translates into yield loss. The economics are compelling: a single herbicide application can prevent yield reductions of 15–40% in heavily infested fields, delivering returns on input investment that justify consistent annual spend even in price-sensitive smallholder contexts.

The Herbicide Market in China is anchored by glyphosate, which remains the dominant active ingredient by volume despite recurring price volatility. Chinese manufacturers collectively account for approximately 65–70% of global glyphosate production capacity, giving domestic companies a structural cost advantage in both home and export markets. Syngenta Group, following its acquisition by ChemChina, has leveraged integrated supply chains to maintain leading positions in premium herbicide formulations, particularly for rice paddy and corn belt applications. Jiangsu Yangnong Chemical Co Ltd is a prominent domestic player, supplying both AI and formulated products to cooperatives and distributors across Jiangsu and Heilongjiang provinces.

The herbicide segment is also benefiting from the push to replace the now-banned paraquat. The search for effective paraquat substitutes has generated significant R&D investment and new product launches, with diquat, glufosinate-ammonium, and several proprietary mixtures gaining traction. Glufosinate-ammonium demand in particular has surged, and Chinese producers including Wynca Group (Wynca Chemicals have scaled capacity to capture both domestic and export demand.

Beyond row crops, the expanding Herbicide Market for turf and ornamental applications in China's rapidly developing urban landscaping sector constitutes an incremental but fast-growing sub-segment. Municipalities investing in green infrastructure are procuring selective herbicides for sports turf, roadway corridors, and ornamental gardens, adding a non-agricultural demand layer that partially insulates the segment from farm-level commodity price cycles.

Formulation innovation is reshaping the competitive dynamics within the herbicide segment. Oil dispersion (OD), suspension concentrate (SC), and water-dispersible granule (WDG) formats are displacing legacy emulsifiable concentrate (EC) formulations, driven by worker safety regulations and buyer preference for reduced-solvent products. This shift toward advanced formulation platforms is consistent with trends observed in the broader Agrochemical Formulation Market, where value migration from actives to formulated end products is a defining competitive dynamic.

In terms of share trajectory, herbicides are consolidating their lead rather than experiencing displacement. While biological alternatives are gaining registrations, their efficacy profiles in high-pressure weed environments and their cost per hectare treated have not yet reached parity with synthetic herbicides at scale. This gap ensures that conventional herbicides will continue to dominate revenue metrics through at least the medium-term forecast window, even as their proportion of the overall pesticide mix gradually adjusts.

The China Pesticide Industry Market is governed by a set of structural drivers and material constraints that collectively define its growth trajectory and risk profile.

Primary Driver — Demand for Landscaping Maintenance and Green Spaces: China's urban greening policies have allocated substantial public budgets to park construction, roadside planting, and corporate campus landscaping. Municipal procurement of turf care inputs, including selective herbicides and fungicides, has grown at an estimated 8–10% annually in Tier-1 and Tier-2 cities. This reflects the broader adoption of green spaces and green roofs in new urban development codes, which mandate minimum vegetated surface ratios in commercial construction projects. The cumulative effect is a reliable institutional demand stream that complements volatile smallholder agricultural purchasing.

Secondary Driver — Food Security and Yield Protection Policy: The central government's No. 1 Document priorities have consistently emphasized grain self-sufficiency, translating into direct subsidies for certified pesticide inputs used in staple crop production. These subsidies effectively underpin demand floors for herbicides, fungicides, and insecticides applied in designated grain protection zones, reducing price elasticity at the end-user level.

Primary Constraint — Labor Shortage in Landscaping: The rural-to-urban labor migration trend has created a structural shortfall of trained pesticide applicators, particularly in landscaping maintenance contexts. Surveys from industry associations indicate that 35–40% of commercial landscaping operators cite skilled labor availability as a top operational constraint. This shortage paradoxically drives demand for systemic, long-residual formulations that reduce application frequency, but it constrains absolute volume growth in labor-intensive application modes such as manual backpack spraying.

Secondary Constraint — High Maintenance Cost of Lawn Mowers and Application Equipment: Capital expenditure for compliant application machinery — motorized sprayers, precision chemigation equipment, and drone-spray platforms — remains prohibitive for smallholder and small-scale landscaping operators. Equipment cost per hectare for drone-based application can exceed ¥150–300, limiting adoption to larger commercial farms and municipalities with dedicated infrastructure budgets.

Regulatory pressure on older active ingredients constitutes a third constraint, as the Ministry of Agriculture and Rural Affairs has accelerated the phase-out schedule for high-toxicity organophosphates, imposing re-registration costs and market access uncertainty on affected product lines.

The competitive landscape of the China Pesticide Industry Market is characterized by the coexistence of global multinationals with integrated discovery capabilities and large-scale domestic Chinese producers that compete primarily on formulation efficiency and supply chain integration.

BASF SE: A global leader in fungicide and herbicide innovation, BASF maintains a robust China commercial organization supported by local formulation facilities. Its collaboration with Corteva Agriscience on soybean weed control exemplifies its strategy of leveraging partnership networks to extend portfolio reach in specialized crop segments.

Bayer AG: Bayer's Crop Science division holds strong positions in seed treatment technologies and insecticides across China's corn and rice belts. Its January 2023 partnership with Oerth Bio signals a strategic pivot toward biologicals integration within its conventional crop protection portfolio.

Corteva Agriscience: Corteva competes through differentiated herbicide and fungicide brands targeting the premium segment of China's commercial crop market. Its BASF collaboration on next-generation weed control reflects a broader trend of co-development to share regulatory and R&D costs in a complex registration environment.

FMC Corporation: FMC has built a notable insecticide franchise in China, particularly around diamide chemistry. The company's market development strategy emphasizes distributor enablement and grower education to drive adoption of its newer AI classes across rice and vegetable crop systems.

Jiangsu Yangnong Chemical Co Ltd: One of China's most significant domestic agrochemical producers, Yangnong is a leading exporter of pyrethroids and other insecticide AIs. Its scale manufacturing operations in Jiangsu province give it a structural cost position in both domestic sales and international supply agreements.

Lianyungang Liben Crop Technology Co Ltd: A mid-tier domestic specialist focusing on herbicide and insecticide formulations for grain and vegetable crops. Liben competes through regional distribution depth and rapid new product registration cycles tailored to local pest spectrums.

Rainbow Agro: Rainbow operates across the full value chain from AI synthesis to retail-packaged formulations, targeting smallholder farmers through extensive rural distribution networks. Its broad product portfolio covers herbicides, fungicides, and insecticides for rice, wheat, and corn.

Syngenta Group: Post-ChemChina acquisition, Syngenta has executed an accelerated China market expansion, investing in local formulation capacity and digital agronomy platforms. It holds leading commercial positions in fungicide, herbicide, and seed treatment segments.

UPL Limited: UPL's global insecticide portfolio, including its Spirotetramat licensing agreement with Bayer, positions it as an integrated solutions provider in China's sucking pest management segment. Its model of acquiring and distributing off-patent generics alongside differentiated actives gives it broad market coverage.

Wynca Group (Wynca Chemicals: A major glyphosate and organophosphate producer, Wynca is a cornerstone of China's AI export infrastructure. The company has been actively expanding into higher-value formulated products to capture margin beyond commodity AI volumes.

January 2023: Bayer AG formed a new strategic partnership with Oerth Bio to advance crop protection technology, specifically targeting the development of eco-friendly crop protection solutions that integrate biological mode-of-action platforms with conventional chemistry frameworks. This collaboration is expected to accelerate the pipeline of reduced-risk products relevant to the China market.

August 2022: BASF SE and Corteva Agriscience announced a collaborative initiative to provide soybean farmers with next-generation weed control solutions. The partnership is aimed at satisfying farmer demand for specialized weed management tools that are chemically and mechanistically distinct from currently available or in-development herbicides, addressing the critical challenge of resistance evolution in major weed species across Asia-Pacific soybean belts.

May 2022: UPL Limited entered into a long-term global data access and supply agreement with Bayer AG specifically covering Spirotetramat insecticide. Under the agreement, UPL will develop, register, and distribute new unique solutions utilizing Spirotetramat as a key active, leveraging its international research and development network to address farmer demands related to resistance management in difficult-to-control sucking pest complexes across multiple crop systems including those prevalent in China.

2022–2023 (Regulatory Cycle): China's Ministry of Agriculture and Rural Affairs continued to advance re-registration requirements for older pesticide active ingredients, with an estimated 15–20 high-toxicity organophosphate and carbamate compounds facing accelerated phase-out timelines, reshaping the competitive landscape for domestic formulators dependent on legacy chemistry portfolios.

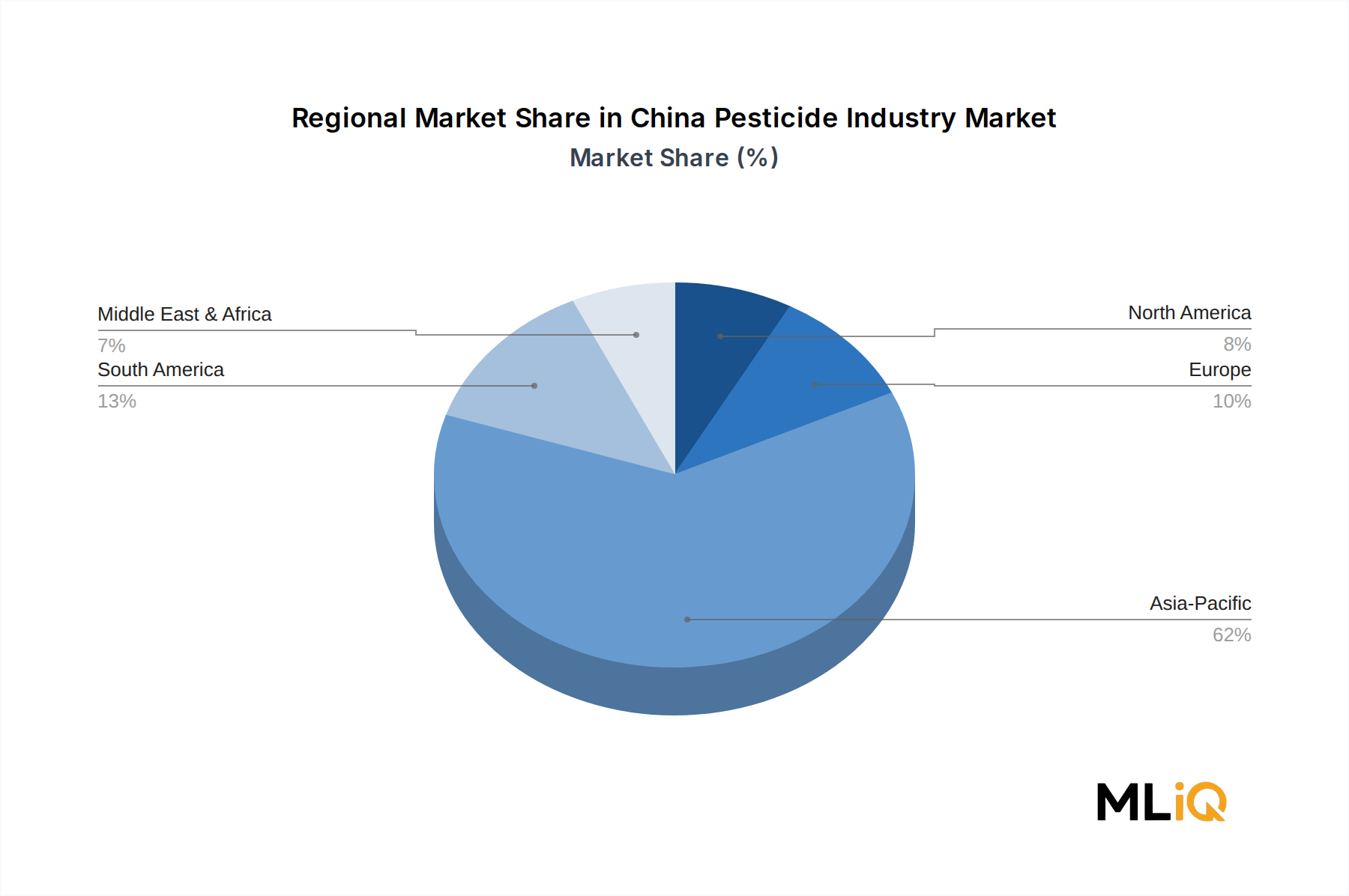

The China Pesticide Industry Market exhibits pronounced regional heterogeneity, driven by differences in crop mix, climate, arable land concentration, and regulatory enforcement intensity.

North China Plain (including Hebei, Henan, and Shandong): This region constitutes the largest revenue-generating zone by absolute value, underpinned by intensive wheat and corn cultivation across approximately 30 million hectares. Herbicide and fungicide demand is elevated, with wheat stripe rust and corn borer being the primary pest management challenges. Mature distribution infrastructure and a high density of agricultural cooperatives create efficient procurement channels. Regional market growth is estimated at approximately 4.5–5.0% CAGR, reflecting the region's maturity and relatively stable crop acreage.

Yangtze River Delta and South China (including Jiangsu, Zhejiang, Guangdong): This region commands the highest pesticide spend per hectare owing to the dominance of high-value horticultural crops, rice double-cropping systems, and intensive vegetable production. Fungicide application rates are particularly high due to humid subtropical conditions. Growth is estimated at 5.5–6.0% CAGR, driven by expanding fruit and vegetable acreage and a rising preference for premium SC and WDG formulations aligned with export MRL requirements for the Southeast Asian and EU markets.

Northeast China (Heilongjiang, Jilin, Liaoning): The soybean and corn breadbasket of China, this region is the primary growth frontier for herbicide consumption as mechanized large-scale farming displaces smallholder production. Glyphosate and glufosinate-ammonium applications are expanding rapidly. Regional CAGR is projected at 6.0–6.5%, making Northeast China the fastest-growing regional segment in the market.

Southwest and Northwest China (Sichuan, Yunnan, Xinjiang): These regions present the highest variability in adoption rates. Xinjiang's cotton and specialty crop sectors drive meaningful insecticide and growth regulator demand, while Yunnan's floriculture industry is an emerging niche for fungicide applications. Combined CAGR for these regions is estimated at 4.0–4.5%, constrained by lower infrastructure density and higher logistics costs that inflate delivered formulation costs for end users.

Asia Pacific as a broader context: China anchors the Asia Pacific Crop Protection Chemical Market, accounting for an estimated 40–45% of regional revenue, and its production surplus substantially influences pricing benchmarks across ASEAN and South Asian markets.

The customer base of the China Pesticide Industry Market is stratified across five primary buyer typologies, each with distinct procurement criteria, price sensitivity profiles, and channel preferences.

Smallholder farmers, who collectively manage an estimated 70% of cultivated land parcels, remain the most price-sensitive buyer segment. Their purchasing decisions are predominantly driven by local word-of-mouth, retailer recommendations from agrochemical stores, and the influence of village-level agronomists employed by distributors. Brand loyalty in this segment is shallow, with switching behavior triggered by marginal price differences as low as 5–8% between comparable formulations. Subsidized procurement channels administered through rural credit cooperatives play a meaningful role in this segment.

Agricultural cooperatives and large-scale farms, which are growing rapidly following land consolidation policies, exhibit more sophisticated procurement behavior. These buyers issue annual supply tenders, conduct field efficacy trials before committing to multi-season contracts, and increasingly specify formulation type, residue profile, and pre-harvest interval (PHI) compliance

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.13% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as Demand For Landscaping Maintenance; Adoption of Green Spaces and Green Roofs are projected to boost the China Pesticide Industry market expansion.

Key companies in the market include BASF SE, Bayer AG, Corteva Agriscience, FMC Corporation, Jiangsu Yangnong Chemical Co Ltd, Lianyungang Liben Crop Technology Co Ltd, Rainbow Agro, Syngenta Group, UPL Limited, Wynca Group (Wynca Chemicals.

The market segments include Function, Application Mode, Crop Type.

The market size is estimated to be USD 5.41 billion as of 2022.

Demand For Landscaping Maintenance; Adoption of Green Spaces and Green Roofs.

Herbicides dominate the market.

Shortage of Labor In Landscaping; High Maintenance Cost of Lawn Mowers.

January 2023: Bayer formed a new partnership with Oerth Bio to enhance crop protection technology and create more eco-friendly crop protection solutions.August 2022: BASF and Corteva Agriscience collaborated to provide soybean farmers with the weed control of the future. By working together, BASF and Corteva aim to satisfy farmers' demand for specialized weed control solutions that are distinct from those that are currently available or being developed.May 2022: UPL partnered with Bayer for Spirotetramat insecticide to develop new pest management solutions. Through this long-term global data access and supply agreement with Bayer, specifically for addressing farmer demands regarding resistance management and difficult-to-control sucking pests, UPL will develop, register, and distribute new unique solutions, including Spirotetramat, using its experience in insecticides and worldwide research and development network.

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "China Pesticide Industry," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the China Pesticide Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.