1. What are the major growth drivers for the Atomic Clock Market market?

Factors such as are projected to boost the Atomic Clock Market market expansion.

Atomic Clock Market

Atomic Clock Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

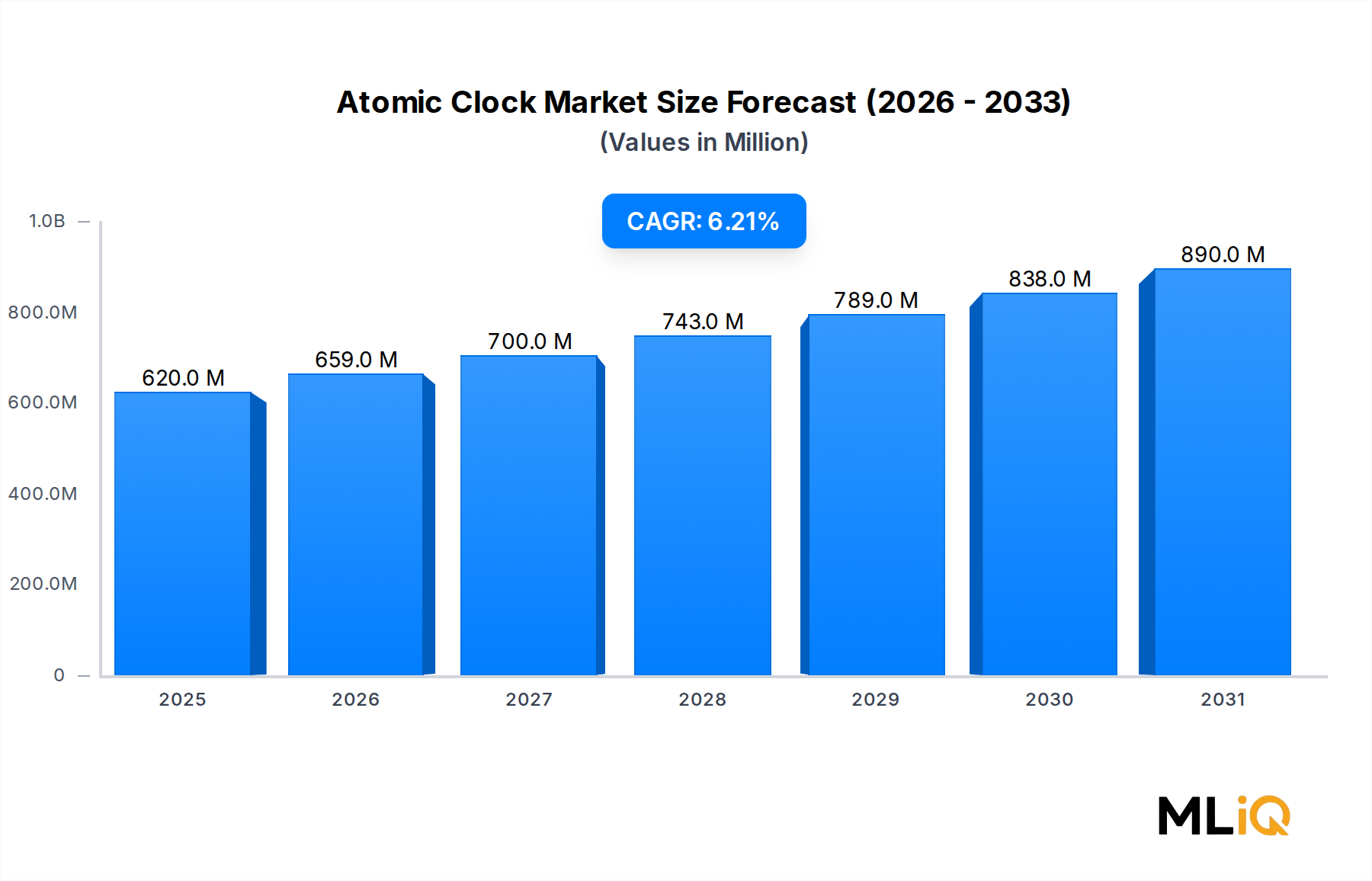

The global Atomic Clock Market is valued at $0.62 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 6.22% through the forecast period, driven by intensifying demand for ultra-precise timekeeping across defense, telecommunications, scientific research, and satellite-based navigation applications. The confluence of next-generation network infrastructure rollouts, expanding global navigation satellite system (GNSS) programs, and escalating defense modernization budgets across major economies creates a structurally favorable macro environment for atomic clock manufacturers and system integrators alike.

The fundamental value proposition of atomic clocks — frequency stability measured in parts per quadrillion — positions them as irreplaceable infrastructure components wherever timing errors translate directly into operational failures or mission-critical system degradation. The proliferation of 5G base station deployments, which demand phase accuracy at the nanosecond level, represents one of the most significant near-term demand catalysts. Telecom carriers across North America, Europe, and Asia Pacific are rapidly upgrading synchronization architectures, creating sustained procurement cycles for rubidium and cesium-based timing units.

On the defense and aerospace front, the shift toward GPS-denied environment operations is compelling military procurement agencies to source high-performance holdover oscillators and chip-scale atomic clocks (CSACs) at volume. Counter-jamming requirements and autonomous navigation for unmanned aerial vehicles (UAVs) are expanding the addressable market well beyond traditional government metrology laboratories.

Scientific metrological institutions worldwide continue to push the boundaries of optical lattice and ion-trap atomic clock technology, with national time laboratories in the United States, Germany, Japan, and China investing in next-generation primary frequency standards. These developments carry downstream commercial implications as miniaturized, lower-cost derivatives reach industrial and telecommunications markets.

From a competitive standpoint, the market remains moderately consolidated, with a handful of established players controlling key intellectual property in resonance cell design, frequency locking loops, and environmental compensation algorithms. However, the emergence of chip-scale and micro-atomic clock platforms is gradually lowering barriers to entry, inviting new participants from the broader semiconductor and MEMS industries. The Rubidium Oscillator Market and the Cesium Frequency Standard Market collectively represent the two most commercially mature sub-segments, while hydrogen maser technology serves premium scientific and space applications. Looking ahead, the integration of atomic clock functionality into system-on-chip architectures and the ongoing commercialization of optical clock technology are expected to introduce meaningful product disruption before the end of the decade.

Within the Atomic Clock Market, rubidium-based atomic clocks constitute the largest and most commercially active segment by revenue share, a position that reflects a well-established balance between performance, cost, size, and power consumption. Rubidium frequency standards operate by locking an oscillator to the hyperfine transition frequency of rubidium-87 atoms at 6.834682610904 GHz, delivering frequency stabilities in the range of 10⁻¹¹ to 10⁻¹² per day — performance that far exceeds quartz oscillators but at a fraction of the cost of cesium beam or hydrogen maser units.

The dominance of rubidium clocks is primarily attributable to their suitability for a wide spectrum of mid-tier precision applications. Telecom network synchronization, GPS receiver holdover, military-grade navigation systems, and broadcasting infrastructure all leverage rubidium units because they offer adequate precision at commercially viable price points, typically ranging from a few hundred to several thousand USD per unit depending on specification grade. Volume-scale procurement by telecom operators and defense contractors has enabled manufacturers to achieve production efficiencies that further entrench rubidium technology's cost advantage.

The miniaturization trend has been particularly transformative for this segment. Chip-scale atomic clocks (CSACs) based on rubidium technology, pioneered in significant part through DARPA-funded research programs, have reduced form factors to just a few cubic centimeters while maintaining timing stability adequate for GPS-denied navigation. Microchip Technology Inc. commercialized this technology through its acquisition of Symmetricom's timing product lines and has since become a key volume supplier of rubidium-based CSACs to defense and industrial markets globally.

Orolia, now part of Safran, maintains a strong product portfolio spanning portable rubidium oscillators to rack-mounted precision timing servers, serving both military and telecommunications verticals. IQD Frequency Products Ltd. and AccuBeat ltd. are also recognized rubidium segment participants, offering catalog and custom-engineered rubidium oscillators for OEM integration across avionics, scientific instrumentation, and industrial timing applications.

The competitive intensity within the rubidium segment has increased meaningfully as Asian manufacturers, particularly from China and Japan, have entered the market with cost-competitive offerings targeting mid-tier telecom and industrial end-users. Chinese state-backed entities have made substantial investments in rubidium cell manufacturing and frequency standard development, creating pricing pressure in segments that previously enjoyed stable margins.

Despite this competitive pressure, the segment's revenue share is expected to remain dominant through the forecast period, supported by the structural expansion of 5G and future 6G network timing requirements, the proliferation of GNSS infrastructure, and ongoing defense procurement of man-portable and vehicle-mounted timing units. The addressable market for rubidium clocks is further augmented by emerging applications in quantum communication network synchronization, autonomous vehicle positioning systems, and power grid phasor measurement units (PMUs), all of which require holdover timing performance in the microsecond-to-nanosecond range that only atomic frequency references can reliably provide.

The Precision Timing Device Market, of which rubidium oscillators form a central pillar, is itself undergoing structural growth as digital infrastructure density increases globally, reinforcing the outlook for sustained volume demand in this dominant segment.

Several high-impact drivers and material constraints define the current growth trajectory of the Atomic Clock Market, each anchored in quantifiable trends drawn from technology deployment cycles, defense spending data, and infrastructure investment patterns.

The foremost demand driver is the global rollout of 5G telecommunications infrastructure. The International Telecommunication Union (ITU) specifies phase accuracy requirements of ±1.5 microseconds for 5G time-division duplex (TDD) networks, a standard that legacy GPS-disciplined oscillators alone cannot reliably meet under signal-degraded conditions. This has driven mobile network operators and tower companies to integrate rubidium holdover clocks at thousands of base station sites, representing a measurable uplift in unit demand. The Telecom Synchronization Market is directly intertwined with atomic clock adoption, amplifying procurement volume across major deployment geographies.

Defense budget expansion constitutes a secondary but high-value driver. NATO member states committed to maintaining defense spending at or above 2% of GDP as of 2023, with electronic warfare, positioning-navigation-timing (PNT), and autonomous systems absorbing a growing share of these budgets. Atomic clocks are classified as critical PNT components, and procurement programs for GPS-alternative navigation and anti-jam timing systems have accelerated substantially since 2022.

The expansion of GNSS constellations — including Europe's Galileo, China's BeiDou, and India's NavIC — requires ground-based timing infrastructure built around cesium and hydrogen maser standards, sustaining institutional demand from national space agencies and time laboratories.

On the constraint side, the high unit cost of cesium beam and hydrogen maser clocks limits their adoption outside well-funded government and scientific procurement channels. Hydrogen masers, which deliver the highest short-term stability, remain priced at $50,000 to $300,000 per unit, confining their market to national metrology institutes and premium satellite ground station operators. Supply chain dependencies on specialized components — including rubidium vapor cells, cesium beam tubes, and low-noise microwave oscillators — represent additional vulnerability, particularly given geopolitical tensions affecting rare material access and semiconductor supply chains.

Leonardo: An Italian defense and aerospace conglomerate with a dedicated timing and frequency division, Leonardo supplies cesium and rubidium frequency standards for military navigation, satellite ground systems, and scientific metrology applications across European and export markets.

Oscilloquartz: A division of ADVA Optical Networking, Oscilloquartz specializes in synchronization solutions for telecom networks, offering cesium-referenced timing servers and software-defined synchronization platforms widely deployed in mobile backhaul and fronthaul architectures.

Excelitas Technologies Corp.: Excelitas develops photonic and optoelectronic subsystems critical to atomic clock resonance cell technology, including rubidium discharge lamps and photodetectors, positioning the company as both a component supplier and a timing module manufacturer.

Stanford Research Systems: A precision instrumentation manufacturer headquartered in California, Stanford Research Systems produces high-performance rubidium frequency standards and signal generators widely used in physics research, metrology laboratories, and calibration facilities.

AccuBeat ltd.: An Israeli manufacturer of rubidium atomic clocks and GPS-disciplined oscillators, AccuBeat serves defense, telecommunications, and scientific markets with compact, mil-spec-qualified frequency reference products.

Orolia: Now integrated into the Safran group, Orolia is a global leader in resilient positioning, navigation, and timing (PNT) solutions, offering a broad portfolio spanning chip-scale to rack-mount atomic clocks for defense, maritime, aviation, and critical infrastructure applications.

IQD Frequency Products Ltd.: A UK-based frequency control specialist, IQD manufactures rubidium oscillators and oven-controlled crystal oscillators (OCXOs) for telecommunications, industrial, and military OEM customers, with distribution networks spanning Europe and Asia.

Tekron: A New Zealand-based manufacturer of precision timing equipment, Tekron specializes in GPS-disciplined atomic clock systems and IEEE 1588 PTP grandmaster clocks for power utility, railway, and telecommunications infrastructure.

Microchip Technology Inc.: A leading semiconductor company that acquired Symmetricom's timing division, Microchip Technology offers the broadest commercial portfolio of atomic timing products including CSACs, rubidium oscillators, and precision time servers under the TimeCesium and Quantum brand lines.

VREMYA-CH JSC: A Russian scientific-industrial enterprise specializing in cesium beam frequency standards and hydrogen masers, VREMYA-CH supplies primary and secondary frequency standards to Russian national metrology institutions and space program infrastructure.

March 2024: Microchip Technology Inc. announced the commercial availability of its second-generation chip-scale atomic clock with improved phase noise performance of -110 dBc/Hz at 10 Hz offset, targeting GPS-denied UAV and autonomous vehicle navigation platforms.

January 2024: The European Space Agency (ESA) confirmed the successful in-orbit validation of passive hydrogen maser clocks aboard Galileo FOC satellites, demonstrating frequency stability of <1 ns/day, setting a benchmark for global navigation satellite system timing performance.

September 2023: Orolia (Safran) secured a multi-year contract with a North American Tier-1 mobile network operator to supply rubidium-based grandmaster clock systems for 5G synchronization infrastructure across more than 2,000 base station sites.

June 2023: The U.S. Defense Advanced Research Projects Agency (DARPA) launched the Robust Optical Clock Network (ROCkN) program with the objective of developing transportable optical atomic clocks with stability exceeding 10⁻¹⁸, intended for military PNT resilience applications.

November 2022: AccuBeat ltd. received Israeli Ministry of Defense approval for a new generation of mil-spec rubidium oscillators designed for integration into next-generation armored vehicle navigation systems, with deliveries scheduled commencing Q1 2024.

August 2022: IQD Frequency Products Ltd. expanded its rubidium oscillator production line at its Crewkerne, UK facility, increasing annual manufacturing capacity by 35% in response to growing demand from the European telecommunications synchronization market.

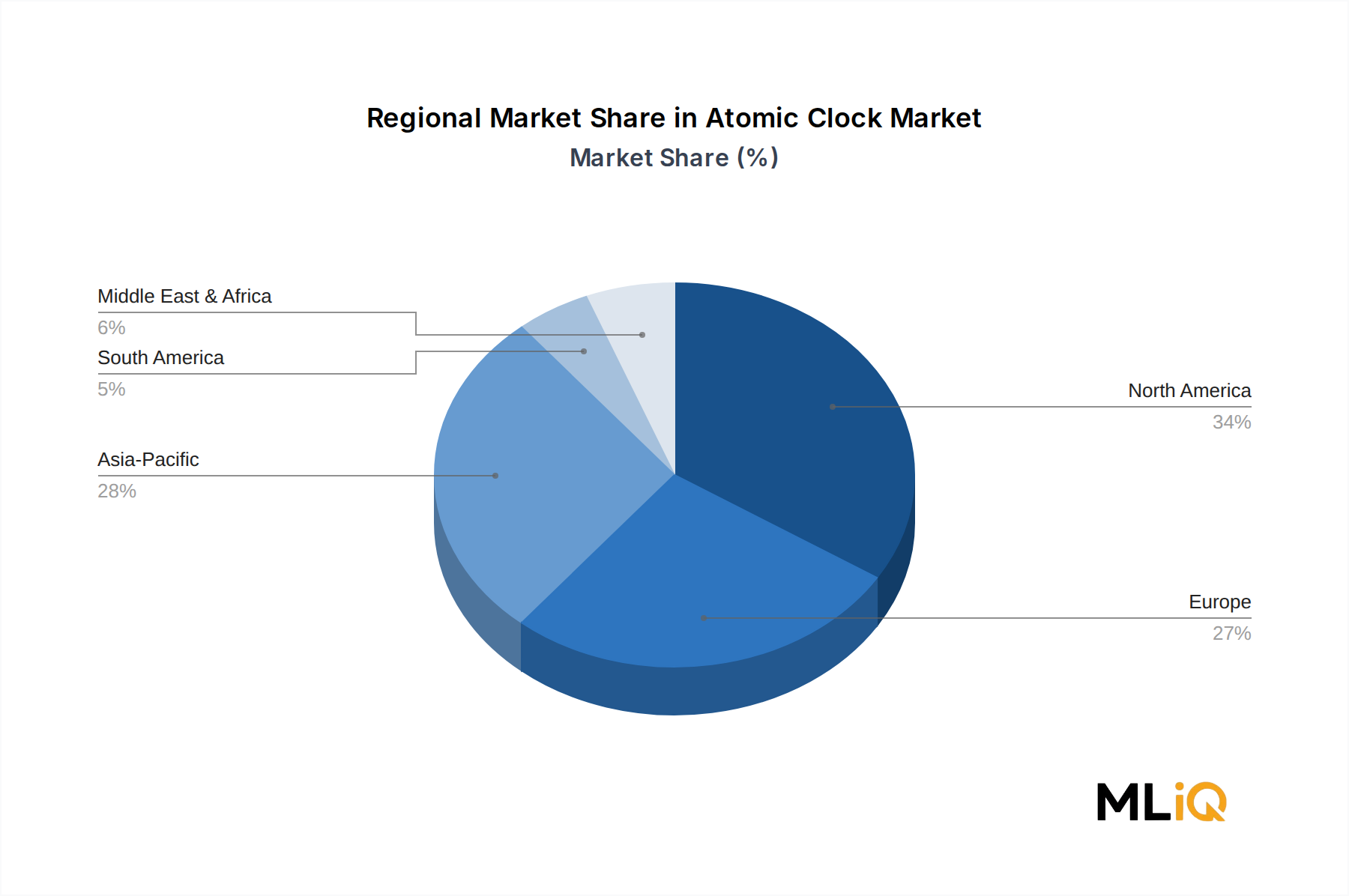

North America represents the largest regional market for atomic clocks, accounting for an estimated 34–37% of global revenue in 2025. The United States drives the overwhelming majority of regional demand through defense procurement programs, GNSS ground infrastructure operated by the U.S. Space Force, and the presence of major commercial timing technology developers. The U.S. Department of Defense's investment in PNT resilience, including the Assured PNT program, sustains consistent public sector demand. Canada and Mexico contribute incrementally through telecom infrastructure upgrades. North America is projected to maintain a regional CAGR of approximately 5.8% through the forecast horizon.

Europe is the second-largest market, with Germany, the United Kingdom, France, and Italy serving as primary demand centers. European demand is anchored by Galileo program support infrastructure, NATO defense modernization, and national metrology institutes including PTB (Germany) and NPL (UK) that procure hydrogen masers and cesium standards for primary frequency calibration. The region benefits from a strong indigenous manufacturing base including Leonardo, Oscilloquartz, IQD, and Orolia. European regional CAGR is estimated at 5.5–6.0%.

Asia Pacific is the fastest-growing regional market, projected at a CAGR of 7.5–8.2%, driven by China's BeiDou satellite navigation system expansion, India's NavIC deployment, and aggressive 5G network infrastructure build-outs across China, Japan, South Korea, and ASEAN nations. China's domestic atomic clock industry, supported by state investment, is scaling rapidly, while Japanese manufacturers maintain precision component competencies relevant to the global supply chain. The Defense Electronics Market is a key growth vector in the region as defense modernization programs intensify.

Middle East and Africa represent an emerging market, with Israel standing out as a technology innovator through AccuBeat and related defense-linked timing research. GCC nations are investing in telecom infrastructure upgrades and smart city timing infrastructure, driving incremental demand. Regional CAGR is estimated at 6.5%, though from a smaller base.

South America remains the least developed regional market, with Brazil accounting for the majority of regional atomic clock procurement, primarily for telecommunications synchronization and GNSS reference station applications. Regional CAGR is estimated at 4.5%.

The customer base for the Atomic Clock Market can be segmented into four primary end-user categories: defense and government agencies, telecommunications operators and infrastructure providers, scientific and metrological institutions, and industrial and commercial technology integrators.

Defense and government customers represent the highest-value segment by average transaction size, procuring customized, qualification-tested units through formal tender processes, often with extended lifecycle support requirements. These buyers prioritize reliability, environmental robustness (temperature range, shock, and vibration specifications), and supply chain security over unit cost. Procurement cycles are long — typically 18 to 36 months from requirement definition to contract award — and single-source or dual-source qualification is common, creating high switching costs and deep customer-supplier relationships. The Satellite Navigation Market and Defense Electronics Market are the primary institutional procurement contexts for this segment.

Telecom operators purchase atomic clocks primarily as capital expenditure items bundled within network synchronization infrastructure upgrades. These buyers are highly sensitive to total cost of ownership (TCO), including power consumption, maintenance intervals, and system integration complexity. The transition to IEEE 1588v2 (PTP) and SyncE architectures has standardized procurement specifications, enabling more competitive bidding and reducing vendor lock-in compared to legacy SONET/SDH timing infrastructures. Volume purchase agreements with 12- to 24-month delivery schedules are common for large-scale 5G rollout programs.

Scientific and metrological institutions procure premium-grade instruments — primarily cesium beam standards and hydrogen masers — through research budget cycles with relatively low price sensitivity. These buyers value absolute accuracy, traceability to SI units, and published performance specifications over commercial warranty terms. Institutional procurement through national laboratories influences downstream market perception of manufacturer technical credibility.

Industrial integrators and OEM customers source rubidium oscillators and CSACs through electronic component distribution channels, with purchasing driven by bill-of-materials cost optimization and form factor constraints. The Frequency Control Products Market and the Quartz Crystal Oscillator

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.22% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Atomic Clock Market market expansion.

Key companies in the market include Leonardo, Oscilloquartz, Excelitas Technologies Corp., Stanford Research Systems, AccuBeat ltd., Orolia, IQD Frequency Products Ltd., Tekron, Microchip Technology Inc., VREMYA-CH JSC.

The market segments include Type, Cesium, Hydrogen, Application.

The market size is estimated to be USD 0.62 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Atomic Clock Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Atomic Clock Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.