Excavator Bucket Dominance in the Construction Machinery Attachment Market

Among all attachment type segments, excavator buckets hold the largest revenue share within the Construction Machinery Attachment Market, accounting for an estimated 28%–32% of total market value across the forecast period. This dominance is deeply structural: excavators represent the highest-volume base machine category globally, and every excavator deployment — whether in earthmoving, trenching, mining, or landscaping — requires at least one bucket configuration, with most fleets maintaining multiple bucket variants (general-purpose, rock, grading, tilt, and ditch-cleaning) per machine.

The primacy of excavator buckets is reinforced by the sheer scale of global excavator sales. The global excavator fleet surpassed 1.2 million active units as of 2024, with China, Japan, South Korea, and the United States accounting for the majority of both production and deployment. Each new excavator sale generates immediate bucket demand, and fleet operators typically rotate buckets every 18 to 36 months depending on application severity, creating a high-frequency replacement market on top of new-unit-linked demand.

Product segmentation within excavator buckets is itself complex. Heavy-duty rock buckets with reinforced side cutters and abrasion-resistant steel liners command premium pricing, particularly in mining and quarrying applications. General-purpose digging buckets dominate the construction and earthmoving segments by volume. Tilting and rotating buckets — increasingly popular in European markets — represent the fastest-growing sub-segment within this category, as they enhance operator precision and reduce repositioning cycles.

On the materials and manufacturing side, the shift toward high-strength, wear-resistant steel alloys such as Hardox 500 and equivalent grades has allowed bucket manufacturers to reduce unit weight while extending service life, supporting a favorable total-cost-of-ownership narrative that accelerates upgrade cycles. Weld-on cutting edges and replaceable side protectors are standard aftermarket consumables that generate recurring revenue independent of new bucket sales.

Key players dominating the excavator bucket sub-segment include Caterpillar Inc., Komatsu Ltd., Volvo Construction Equipment AB, JCB, and a range of specialist aftermarket manufacturers such as Esco Group (a Weir Company), Hensley Industries, and MTG. OEM-branded buckets benefit from warranty integration and machine compatibility assurance, while aftermarket suppliers compete aggressively on price, availability, and customization flexibility.

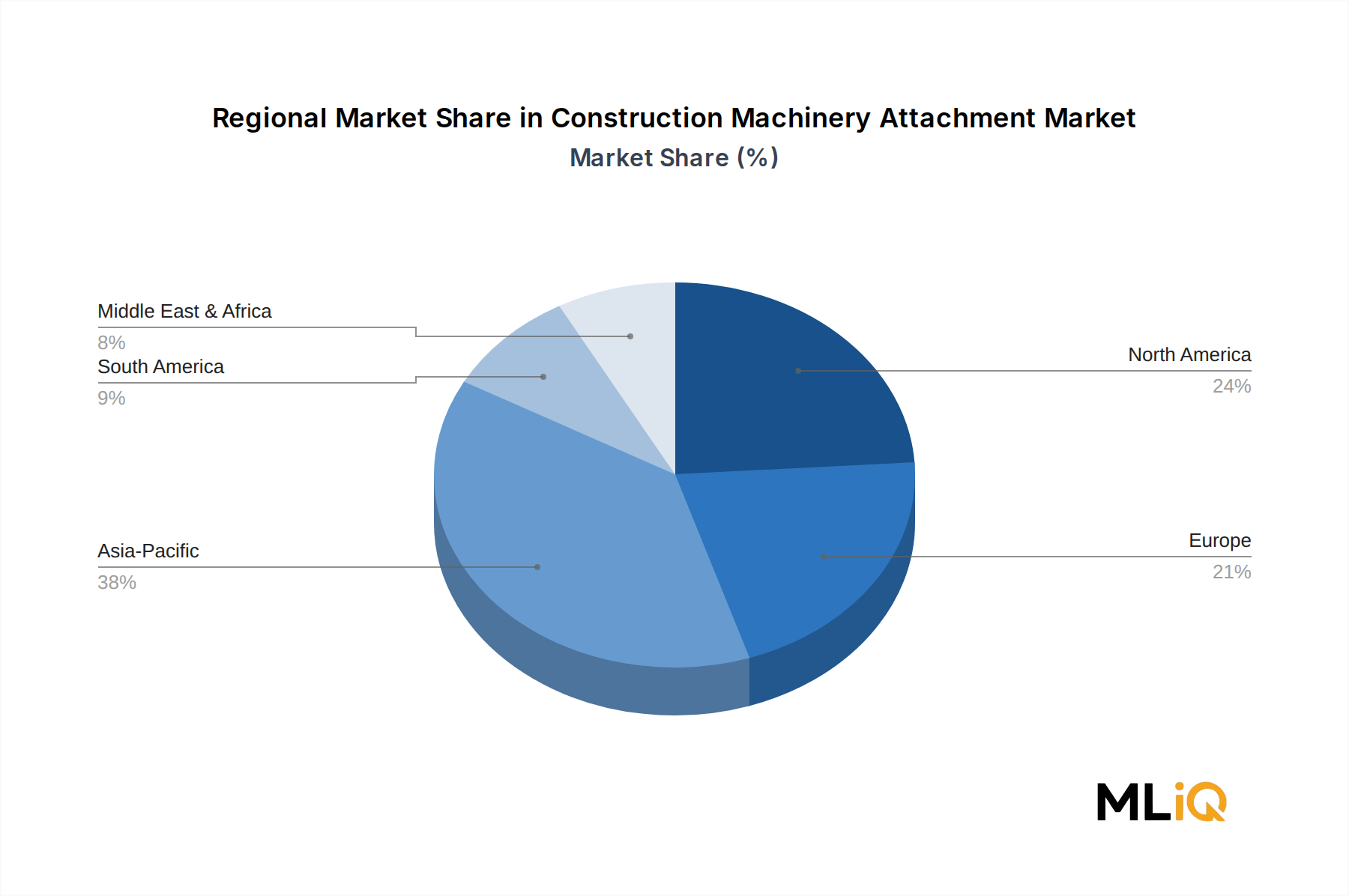

Regionally, Asia Pacific — led by China and India — commands the highest volume share of excavator bucket consumption, driven by the sheer size of regional construction activity and excavator fleet density. North America and Europe exhibit higher per-unit revenue due to the prevalence of specialty bucket configurations, premium wear materials, and hydraulic tilt-bucket upgrades.

The excavator bucket segment's share within the broader Construction Machinery Attachment Market is consolidating rather than eroding, as the global excavator fleet continues to grow and bucket replacement intervals remain relatively short. Attachment manufacturers are investing in digital wear monitoring — embedding sensors within cutting edges to alert operators of replacement thresholds — as a value-added differentiator that supports premium pricing and service contract attachment.