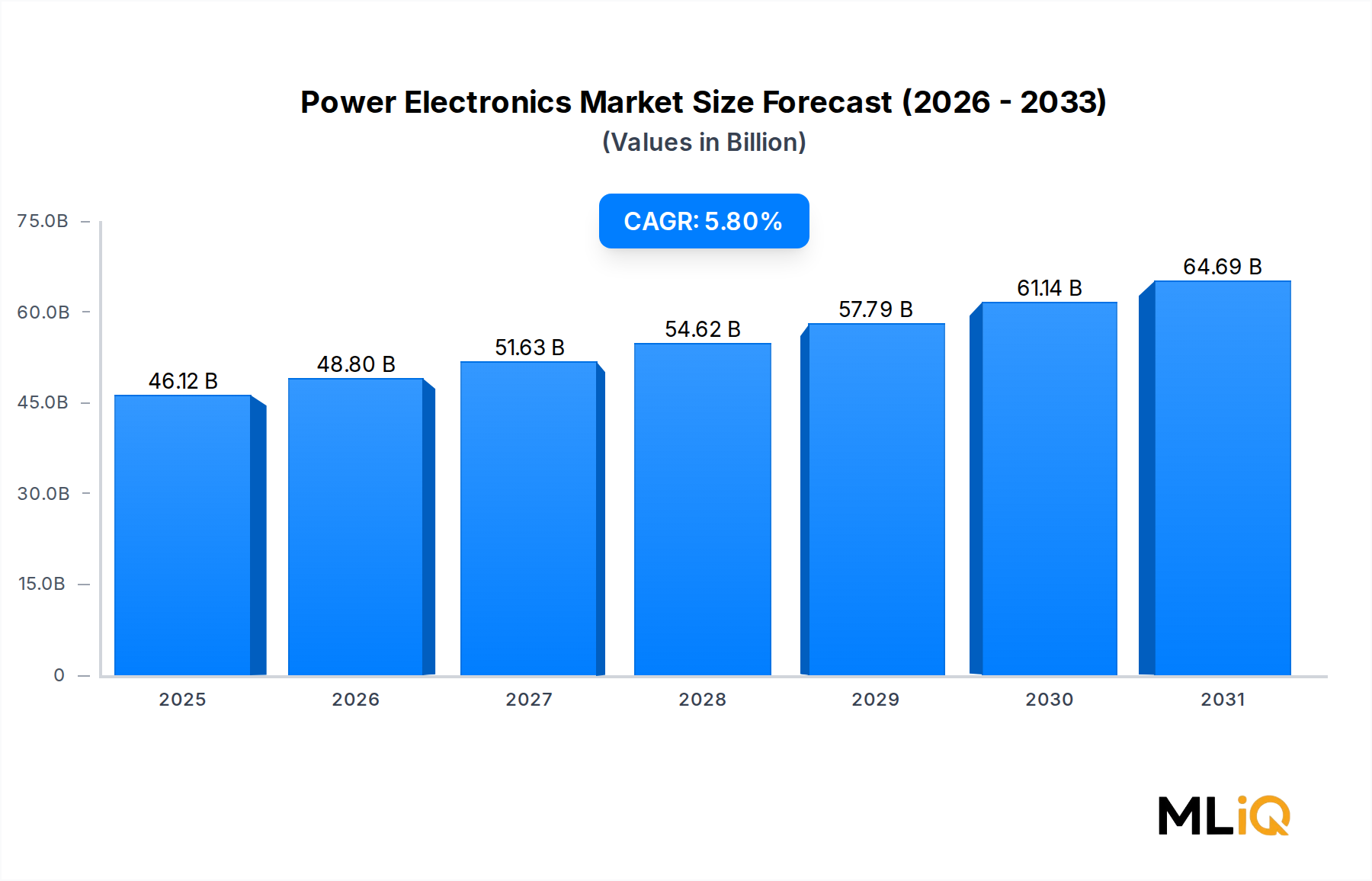

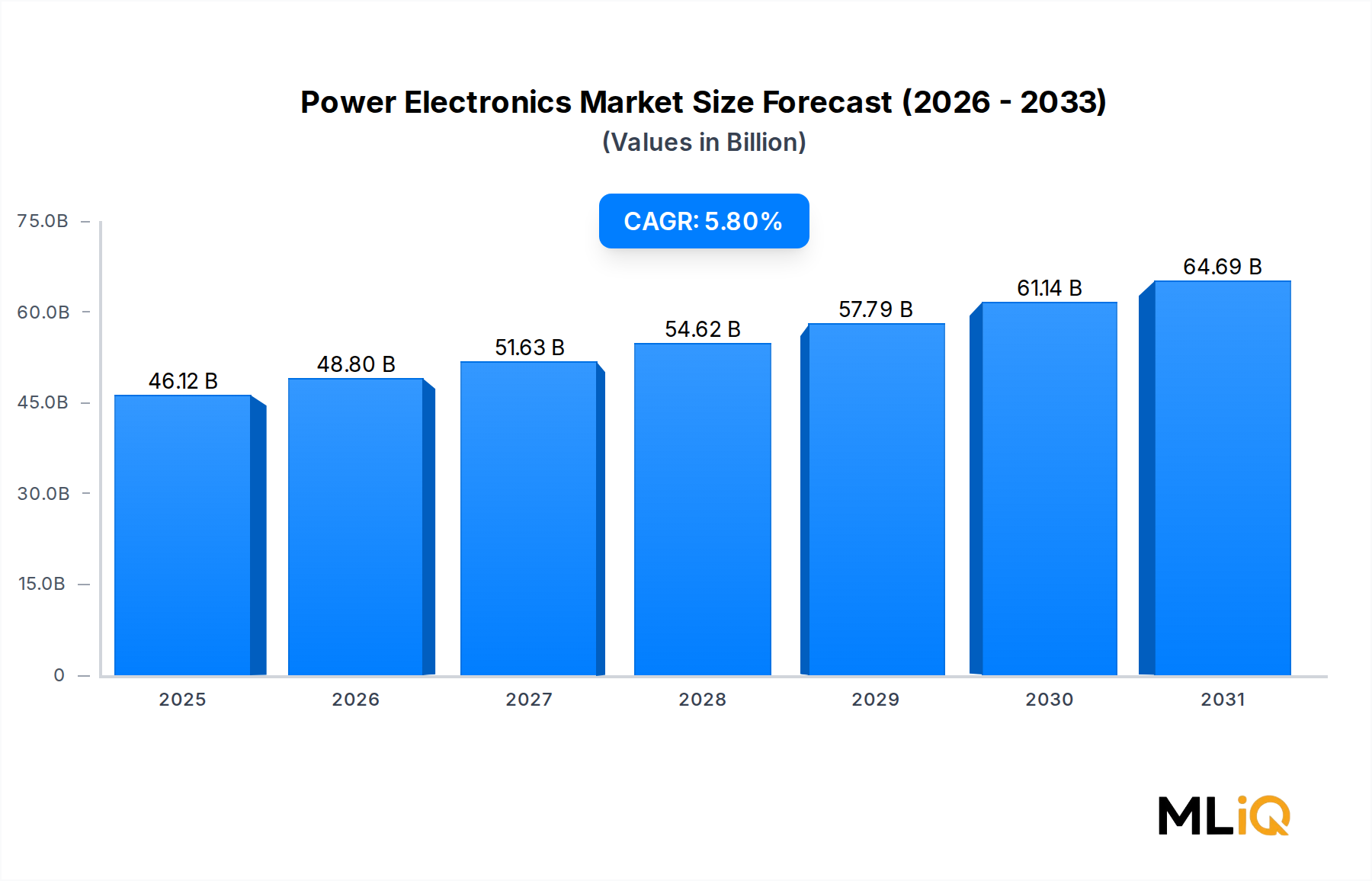

Power Discrete Device Dominance in the Power Electronics Market

Among the three primary device type segments — Power Discrete, Power Module, and Power IC — the Power Discrete segment commands the largest revenue share and continues to consolidate its leadership position across the forecast horizon. Power discrete devices, which include individual transistors, diodes, thyristors, and rectifiers, are indispensable in applications requiring high-voltage and high-current handling where monolithic integration is either technically impractical or cost-prohibitive.

The dominance of power discrete devices is rooted in several structural factors. First, the automotive sector's rapid electrification has generated surging demand for insulated gate bipolar transistors (IGBTs) and metal-oxide-semiconductor field-effect transistors (MOSFETs), which are widely deployed in EV traction inverters, onboard chargers, and DC-DC converters. A single battery electric vehicle (BEV) can incorporate upwards of 400 discrete power semiconductors, making automotive applications one of the fastest-growing sub-segments within the discrete device category.

Second, the renewable energy sector — particularly solar photovoltaic (PV) inverters and wind turbine converters — relies heavily on high-power discrete components capable of withstanding harsh operational environments and thermal cycling. As global solar PV capacity additions are projected to exceed 350 GW annually by 2026, demand for robust discrete power devices is expected to scale proportionally. The Renewable Energy Inverter Market is directly dependent on this segment's innovation pipeline.

Third, industrial motor drives and power supplies for factory automation applications consume large volumes of discrete IGBTs and SiC MOSFETs, particularly as manufacturers upgrade legacy systems to meet energy efficiency mandates. The Industrial Motor Drive Market represents a significant anchor demand base, insulating the power discrete segment from cyclical volatility in consumer-oriented applications.

Key players driving revenue within the power discrete segment include Infineon Technologies AG, which holds a leading global market position in IGBTs and SiC MOSFETs with dedicated manufacturing facilities in Germany, Austria, and Malaysia. STMicroelectronics N.V. has aggressively expanded its SiC MOSFET portfolio, leveraging long-term supply agreements with major EV manufacturers. Mitsubishi Electric Corporation and Toshiba Corporation retain strong positions in high-voltage IGBT modules serving industrial and railway traction applications, while Renesas Electronics Corporation focuses on automotive-grade discrete devices with stringent reliability certifications.

The segment's share is not only growing in absolute terms but also qualitatively transforming as wide bandgap materials displace conventional silicon. SiC-based discrete devices, in particular, are commanding significant price premiums — typically 2x to 3x the cost of equivalent silicon IGBTs — yet are being readily adopted due to system-level efficiency gains and reduced cooling requirements. This premiumization trend is expanding revenue pools even in markets where unit volume growth is moderate.

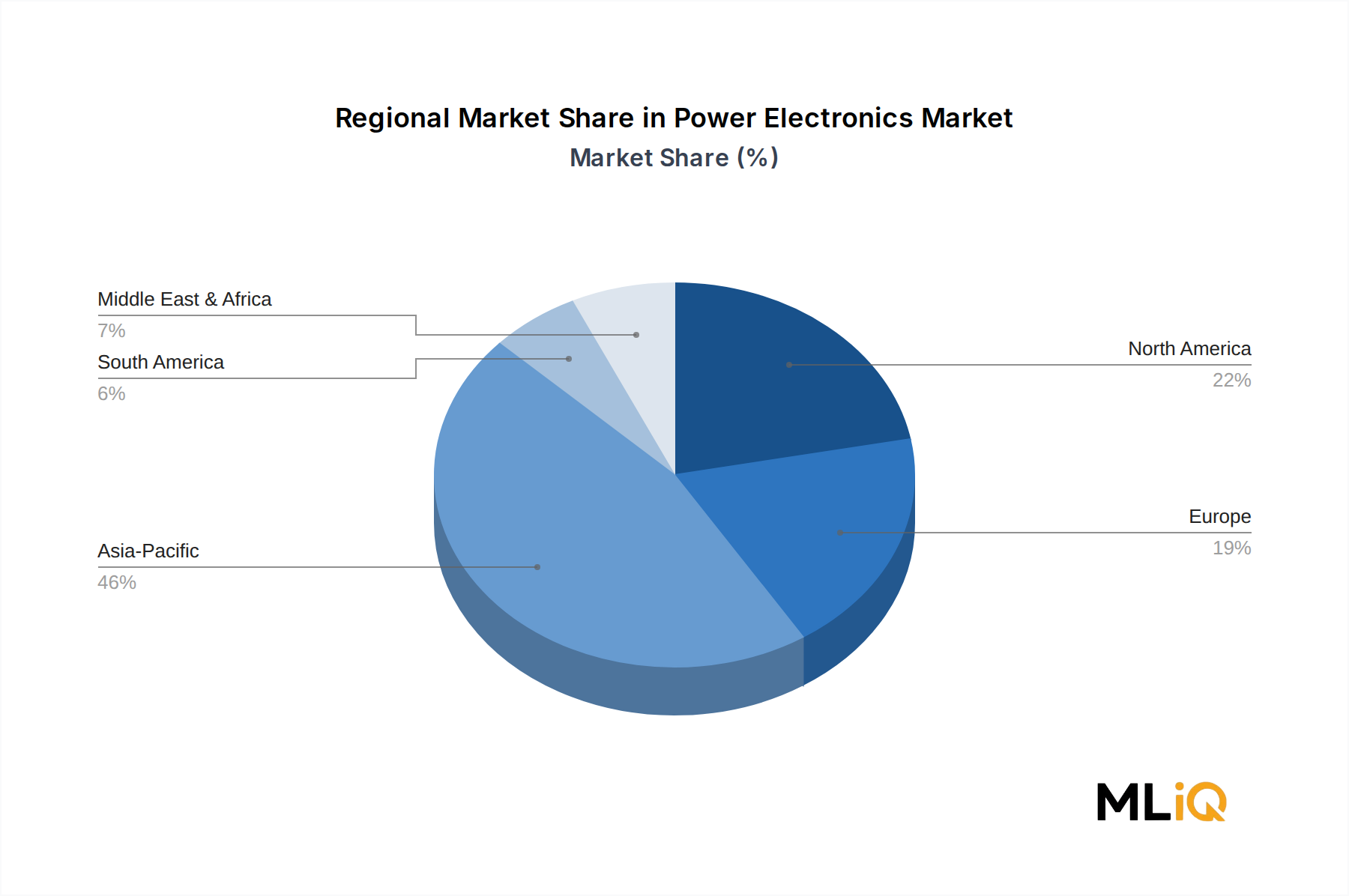

Geographically, the Asia Pacific region dominates power discrete device production and consumption, accounting for an estimated 42% of global revenue, led by China, Japan, and South Korea. However, the United States and Europe are investing heavily in reshoring discrete device manufacturing to reduce geopolitical supply chain exposure, with major capacity announcements from Infineon, Wolfspeed, and onsemi totaling over $10 billion in committed capital expenditure through 2027.

Consolidation within the power discrete segment is expected to continue as tier-1 manufacturers acquire niche SiC and GaN specialists to accelerate technology roadmaps. The segment's commanding position within the broader Power Electronics Market is anticipated to remain intact through 2033, supported by electrification megatrends and the irreplaceable role of discrete components in high-power conversion systems.