1. What are the major growth drivers for the Caps and Closures Market market?

Factors such as are projected to boost the Caps and Closures Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

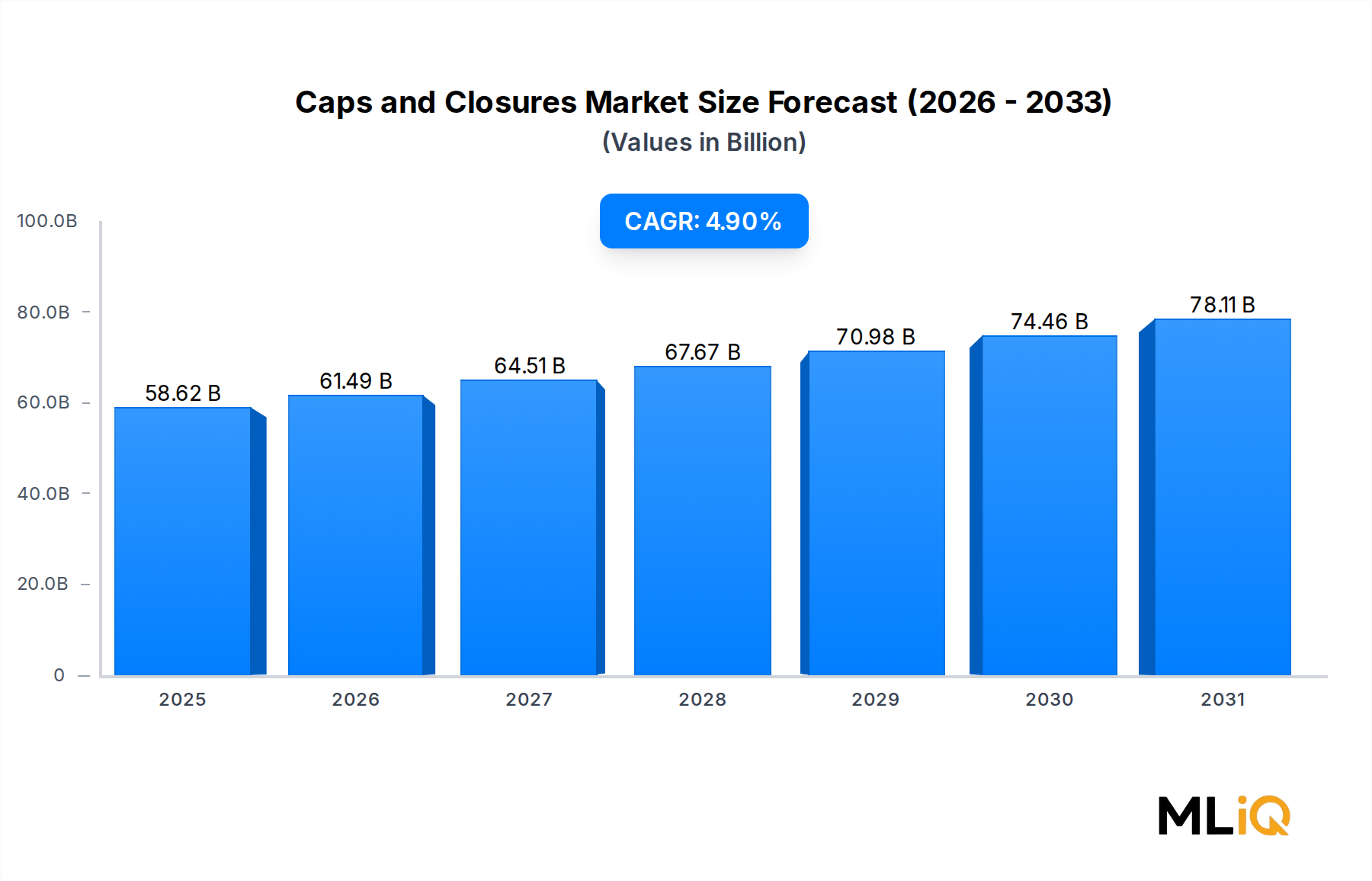

The global Caps and Closures Market was valued at approximately $58,622.61 million and is projected to expand at a compound annual growth rate (CAGR) of 4.9% through 2033, reflecting sustained demand across food, beverage, pharmaceutical, and personal care sectors. This trajectory positions the market as a structurally resilient packaging sub-segment, anchored by the inexorable growth in packaged beverage consumption, rising urbanization, and accelerating e-commerce logistics that demand robust, tamper-evident sealing solutions.

Key demand drivers include the proliferation of single-serve and on-the-go beverage formats, which have intensified the need for lightweight, resealable, and child-resistant closures. The bottled water segment alone accounted for a substantial share of closure volumes globally in 2024, driven by heightened health consciousness and a migration away from sugary carbonated beverages in developed markets. Simultaneously, premium wine and craft beer categories are fueling demand for specialty closures such as natural corks, screw caps, and synthetic alternatives, reinforcing product differentiation strategies among beverage brands.

Macro tailwinds include rising consumer incomes in Asia Pacific and Latin America, expanding modern retail infrastructure, and regulatory mandates around tamper-evidence and child-resistant packaging in North America and Europe. These regulatory frameworks are compelling manufacturers to invest in advanced closure engineering, particularly for pharmaceutical and nutraceutical applications.

From a materials standpoint, plastic remains the dominant raw material, commanding the largest volume share due to cost efficiency, design versatility, and compatibility with high-speed filling lines. However, the industry is undergoing a material transition as brand owners respond to Extended Producer Responsibility (EPR) legislation and circular economy mandates by shifting toward recycled content, mono-material constructions, and bio-based polymers.

The competitive landscape is moderately consolidated, with global players such as Berry Global, Amcor, AptarGroup, and Crown Holdings controlling significant revenue shares through vertical integration, geographic diversification, and continuous innovation pipelines. Smaller regional players compete on price and customization, particularly in emerging markets.

Looking ahead to 2033, the market is expected to benefit from smart closure technologies incorporating QR codes, NFC chips, and freshness indicators that transform the humble cap into an interactive consumer touchpoint. The convergence of sustainability imperatives, technological innovation, and premiumization trends will define competitive differentiation through the forecast horizon, creating both disruption and opportunity for incumbents and new entrants alike.

Among all product and material segments within the Caps and Closures Market, plastic screw closures represent the single largest revenue-generating category, commanding a dominant share of both volume and value metrics globally. This dominance is not incidental; it is the product of decades of materials engineering advancement, manufacturing scalability, and alignment with the structural demands of the modern beverage and food packaging supply chain.

Plastic screw closures are ubiquitous across bottled water, carbonated soft drinks, dairy products, condiments, and household chemical applications. Their adoption is underpinned by the Plastic Packaging Market, which provides the raw material and manufacturing infrastructure necessary for high-throughput closure production. High-density polyethylene (HDPE) and polypropylene (PP) remain the dominant resin types, offering an optimal balance of chemical resistance, barrier properties, torque performance, and recyclability.

The segment's dominance is reinforced by several structural factors. First, global PET bottle production — a cornerstone of the Polyethylene Terephthalate Market — is intrinsically linked to plastic closure demand, as every PET bottle requires a compatible closure system. The global PET bottle market produces hundreds of billions of units annually, each necessitating a closure, creating an enormous and highly predictable demand floor.

Second, high-speed continuous thread (CT) closures are standard equipment on virtually all beverage filling lines, giving plastic screw closures a significant installed-base advantage over alternative formats. Switching costs for filling line retooling create high barriers to displacement by competing closure types such as metal crowns or corks, particularly in the carbonated soft drinks segment.

Third, plastic closures are highly amenable to functional innovation. Tamper-evidence bands, child-resistant mechanisms, dispensing spouts, flip-top actuation, and freshness indicators can all be integrated into plastic closure architectures at relatively modest incremental cost. This versatility allows the segment to serve both mass-market commodity applications and premium, high-functionality niches simultaneously.

Key players dominating this sub-segment include Berry Global, Inc, which maintains an extensive portfolio of injection-molded closures across multiple industries and geographies. BERICAP GmbH And Co. KG is a specialist closure manufacturer with a strong European and global footprint, particularly in beverage, industrial, and food closures. Amcor Plc integrates closure manufacturing within its broader flexible and rigid packaging platform, offering converged solutions to multinational brand owners.

In terms of market share trajectory, the plastic screw closure segment is consolidating rather than dramatically expanding its share, as sustainability pressures are beginning to slow growth at the margins. The introduction of tethered cap regulations under the European Union's Single-Use Plastics Directive — mandating that closures remain attached to beverage containers from July 2024 — has triggered a significant product re-engineering cycle, requiring capital investment but also reinforcing the segment's technological moat. Manufacturers capable of delivering compliant tethered closure solutions at scale are effectively gaining competitive ground, as the regulatory transition barriers favor well-capitalized, technically sophisticated players.

The convergence of regulatory compliance, material innovation toward recycled and bio-based resins, and functional premiumization ensures that plastic screw closures will remain the revenue backbone of the Caps and Closures Market through 2033, even as alternative materials gain incremental share in specific end-use niches.

The Caps and Closures Market is propelled by a set of quantifiable structural drivers while simultaneously navigating material and regulatory headwinds that constrain margin expansion and require continuous capital investment.

Primary driver: Bottled beverage volume growth. Global bottled water consumption surpassed 400 billion liters in 2023, with per-capita consumption growing at above-average rates across Southeast Asia, India, and Sub-Saharan Africa. Each liter of bottled water requires at least one closure unit, creating a direct, measurable linkage between beverage consumption growth and closure demand. The carbonated soft drinks segment — representing one of the largest application categories — generates comparable closure demand volumes, further reinforcing this driver's structural importance.

Second driver: Regulatory mandates for tamper-evidence and child-resistance. In the United States, the Poison Prevention Packaging Act (PPCA) mandates child-resistant closures for pharmaceuticals and household chemicals, creating a regulatory floor of demand that is immune to cyclical economic downturns. Similarly, the EU Single-Use Plastics Directive's tethered cap requirement is driving a product transition cycle worth hundreds of millions of dollars in re-tooling investment across European filling operations through 2025.

Third driver: Premiumization in wine and spirits. The global wine market's shift toward premium and super-premium tiers is directly stimulating demand for natural cork, synthetic cork, and screw cap closures that convey quality signals. The Cork and closures segment benefits from the intersection of premiumization and sustainability narratives.

Primary constraint: Volatile raw material costs. Polyethylene and polypropylene resin prices are highly correlated with crude oil and natural gas feedstock pricing. The 2022 energy crisis caused resin prices to spike by over 40% in some European markets, compressing closure manufacturer margins and triggering pricing disputes with brand-owner customers. Sustained raw material volatility remains a key risk.

Second constraint: Sustainability and recyclability pressure. Brand owners under EPR obligations are demanding increased recycled content, lightweighting, and mono-material designs. Transitioning manufacturing lines to process recycled resins and engineering closures for compatibility with recycling streams requires significant R&D and capital expenditure, creating a near-term financial burden, particularly for mid-size producers.

The competitive landscape of the Caps and Closures Market is characterized by a tiered structure of global integrated packaging conglomerates, specialized closure manufacturers, and regional players. The following profiles illustrate the strategic positioning of the market's principal participants.

Allstates Rubber And Tool Corp: A diversified manufacturer offering rubber and plastic closure solutions primarily for industrial and specialty applications, leveraging custom fabrication capabilities to serve niche segments with technical sealing requirements.

Amcor Plc: A global packaging leader integrating closure solutions within its broader rigid and flexible packaging portfolio, with sustainability commitments targeting 100% recyclable or reusable packaging by 2025 driving material innovation across its closure product lines.

AptarGroup, Inc: A specialist in dispensing, sealing, and active packaging solutions, AptarGroup differentiates through high-value dispensing closure systems for beauty, personal care, pharmaceutical, and food applications, commanding premium pricing through functional innovation.

Ball Corporation: Primarily a metal packaging leader, Ball Corporation's closure-related capabilities are concentrated in aluminum can ends and easy-open end technologies, benefiting from the structural growth of the Aluminum Cans Market and sustainable packaging mandates.

BERICAP GmbH And Co. KG: One of the world's largest dedicated closure manufacturers, BERICAP operates globally with deep expertise in screw closures, sports caps, and dispensing closures for the food, beverage, and industrial segments, with particular strength in European markets.

Berry Global, Inc: A scale-driven packaging conglomerate with one of the broadest closure portfolios globally, Berry Global competes across commodity and specialty closure segments through a combination of geographic reach, material science capabilities, and manufacturing efficiency.

Crown Holdings, Inc: A global leader in metal packaging and closures, Crown Holdings specializes in metal crowns, lug closures, and can ends for beverage and food applications, benefiting from the structural dynamics of the Metal Packaging Market.

GCL Holdings S.C.A: A holding entity with interests in packaging and closures, GCL Holdings operates strategically in European and global markets with a focus on value-added closure systems for premium food and beverage applications.

JELINEK CORK GROUP: A heritage natural cork producer supplying premium wine and spirits closures, JELINEK competes on quality, sustainability credentials of natural cork, and supply chain traceability for high-end beverage brands.

M.A. SILVA USA, LLC: A natural and technical cork specialist serving the North American wine market, M.A. SILVA focuses on product quality, customization, and brand storytelling as key differentiators in the premium wine closure segment.

July 2024: The European Union's tethered cap mandate under the Single-Use Plastics Directive came into full effect, requiring all plastic beverage bottles under three liters sold in EU member states to feature closures physically attached to the container, triggering a major product redesign wave across the industry.

March 2024: Berry Global announced the commercial launch of a new lightweight, fully recyclable polypropylene screw closure designed to meet EU recyclability standards, reducing material usage by approximately 15% per unit compared to legacy designs.

November 2023: AptarGroup completed the acquisition of a specialty dispensing technology company to strengthen its active and intelligent closure portfolio, expanding capabilities in precision dosing and contamination-prevention closure systems for pharmaceutical and nutraceutical applications.

September 2023: Crown Holdings announced a strategic investment in next-generation easy-open can end manufacturing technology at its European operations, targeting a 20% reduction in aluminum material usage per end unit through advanced forming technologies.

June 2023: BERICAP introduced a new bio-based polypropylene closure grade manufactured using renewable feedstock, achieving a carbon footprint reduction of over 30% versus conventional fossil-based equivalents, aligned with key beverage brand sustainability sourcing requirements.

February 2023: Amcor Plc and a major global beverage brand announced a multi-year supply agreement covering recyclable closure systems incorporating post-consumer recycled (PCR) resin content of at least 25%, reflecting accelerating brand-owner commitments to circular economy packaging targets.

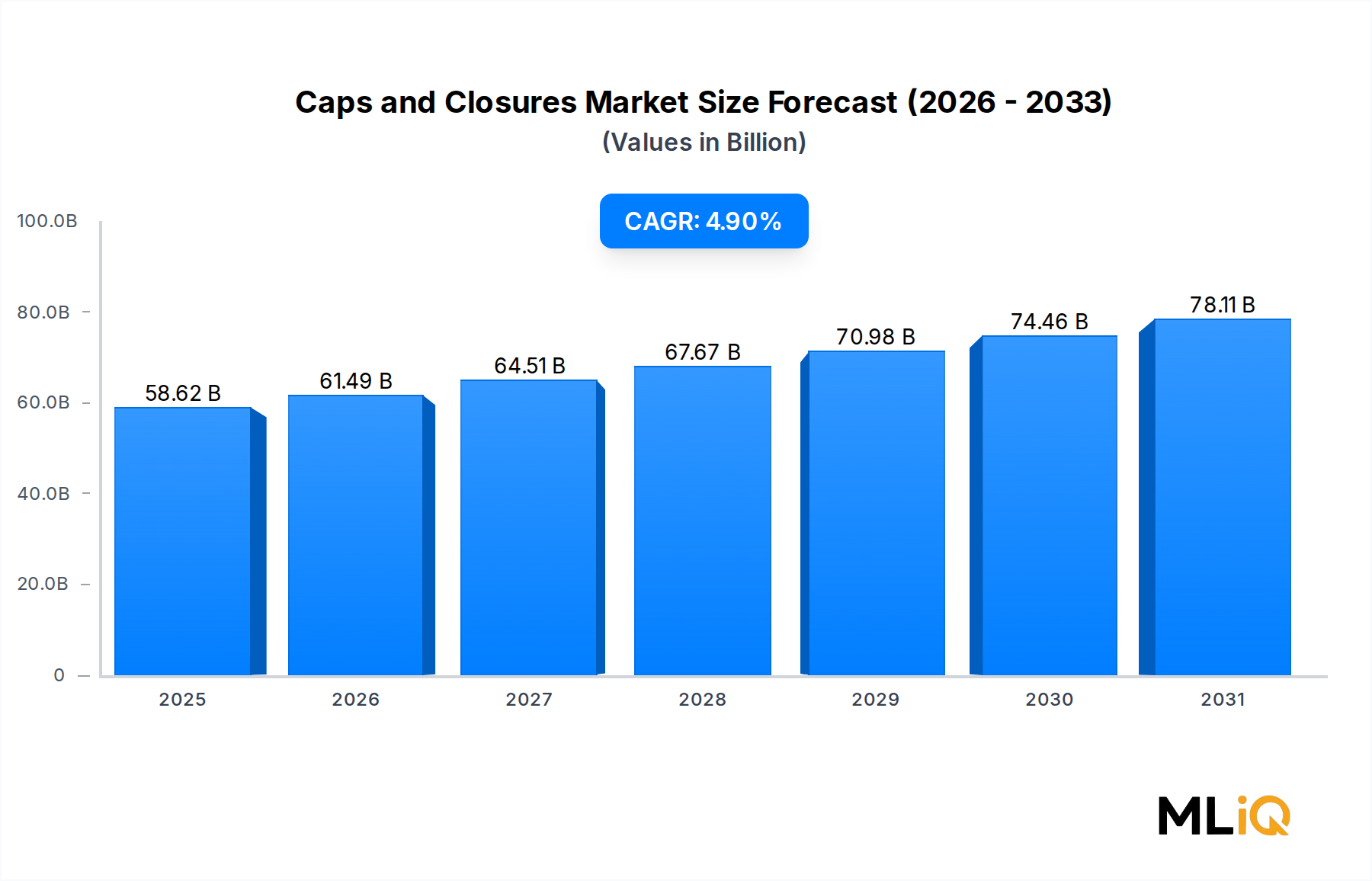

The Caps and Closures Market exhibits meaningful regional differentiation in terms of growth velocity, end-use mix, and regulatory environment, with Asia Pacific and North America representing the two most consequential geographic poles.

Asia Pacific is the fastest-growing region in the Caps and Closures Market, projected to expand at a CAGR of approximately 6.2% through 2033, driven by explosive bottled water consumption growth in India and Southeast Asia, rapidly modernizing beverage manufacturing infrastructure in China, and a growing middle class increasing per-capita packaged food and beverage consumption. China alone accounts for a disproportionate share of global PET bottle and plastic closure production volumes, supported by the scale economics of its domestic packaging manufacturing base.

North America represents the most mature regional market, with the United States contributing the largest single-country revenue share globally. Growth is more moderate at an estimated CAGR of approximately 3.8%, driven primarily by regulatory-driven product upgrades — including tethered closure preparation, child-resistant closure compliance, and recyclability mandates — rather than volume expansion. Premiumization in craft beer, spirits, and premium water categories also supports value growth above volume growth.

Europe is experiencing a structurally significant transition period driven by the EU Single-Use Plastics Directive and EPR frameworks that are compelling the entire regional supply chain to re-engineer closure designs. The region's CAGR is estimated at approximately 3.5% through 2033, constrained in the near term by compliance-related capital costs but supported by premium wine and spirits closure demand in France, Italy, and Spain.

Latin America, particularly Brazil and Argentina, is a mid-growth region with an estimated CAGR of approximately 5.1%, supported by expanding modern retail penetration, growing bottled water markets, and increasing demand for condiment and sauce packaging closures aligned with evolving food consumption patterns.

Middle East and Africa represents an emerging opportunity, with a projected CAGR of approximately 5.8%, driven by population growth, urbanization, and improving cold-chain infrastructure that supports packaged beverage market development. The GCC countries exhibit above-average demand for premium closure formats linked to bottled water and juice categories.

The Caps and Closures Market is undergoing a technology-driven transformation across three primary innovation vectors: smart and connected closures, sustainable material engineering, and precision dispensing systems.

Smart and connected closures represent the most disruptive near-term technology trajectory. These closures incorporate QR codes, NFC (Near Field Communication) chips, or RFID tags directly into the closure structure, enabling consumer engagement, supply chain authentication, product traceability, and freshness monitoring. Several major beverage brands piloted connected closure programs in 2023 and 2024, with adoption timelines pointing toward mainstream commercial deployment in premium beverage segments by 2026–2027. R&D investment in this area is accelerating, with packaging technology firms and electronics component suppliers forming cross-industry consortia to drive cost reduction from current per-unit smart closure premiums of approximately $0.05–$0.20 toward mass-market thresholds. This technology reinforces incumbent business models for large, well-capitalized closure manufacturers who can absorb the integration engineering costs while offering differentiated value propositions to brand-owner customers.

Sustainable material engineering, encompassing bio-based resins, chemically recycled polymers, and mono-material architecture design, is the second major innovation vector. The Sustainable Packaging Market imperative is compelling closure manufacturers to reformulate standard PP and HDPE closures using certified renewable or recycled feedstocks. The Injection Molding Market is evolving in parallel to process higher proportions of recycled resins without compromising dimensional tolerances and mechanical performance critical to high-speed filling line compatibility. Commercial availability of food-grade recycled PP for closures is expanding, with adoption projected to accelerate through 2025–2028 as supply chains for recycled feedstocks mature. \

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.9% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Caps and Closures Market market expansion.

Key companies in the market include Allstates Rubber And Tool Corp, Amcor Plc, AptarGroup, Inc, Ball Corporation, BERICAP GmbH And Co. KG, Berry Global, Inc, Crown Holdings, Inc, GCL Holdings S.C.A, JELINEK CORK GROUP, M.A. SILVA USA, LLC.

The market segments include Product Type, Raw Material, Application.

The market size is estimated to be USD 58622.61 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3799, USD 5899, and USD 11500 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Caps and Closures Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Caps and Closures Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.