1. What are the major growth drivers for the South America Quinoa Seeds Industry market?

Factors such as are projected to boost the South America Quinoa Seeds Industry market expansion.

+1 2315155523

South America Quinoa Seeds Industry

South America Quinoa Seeds Industry

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

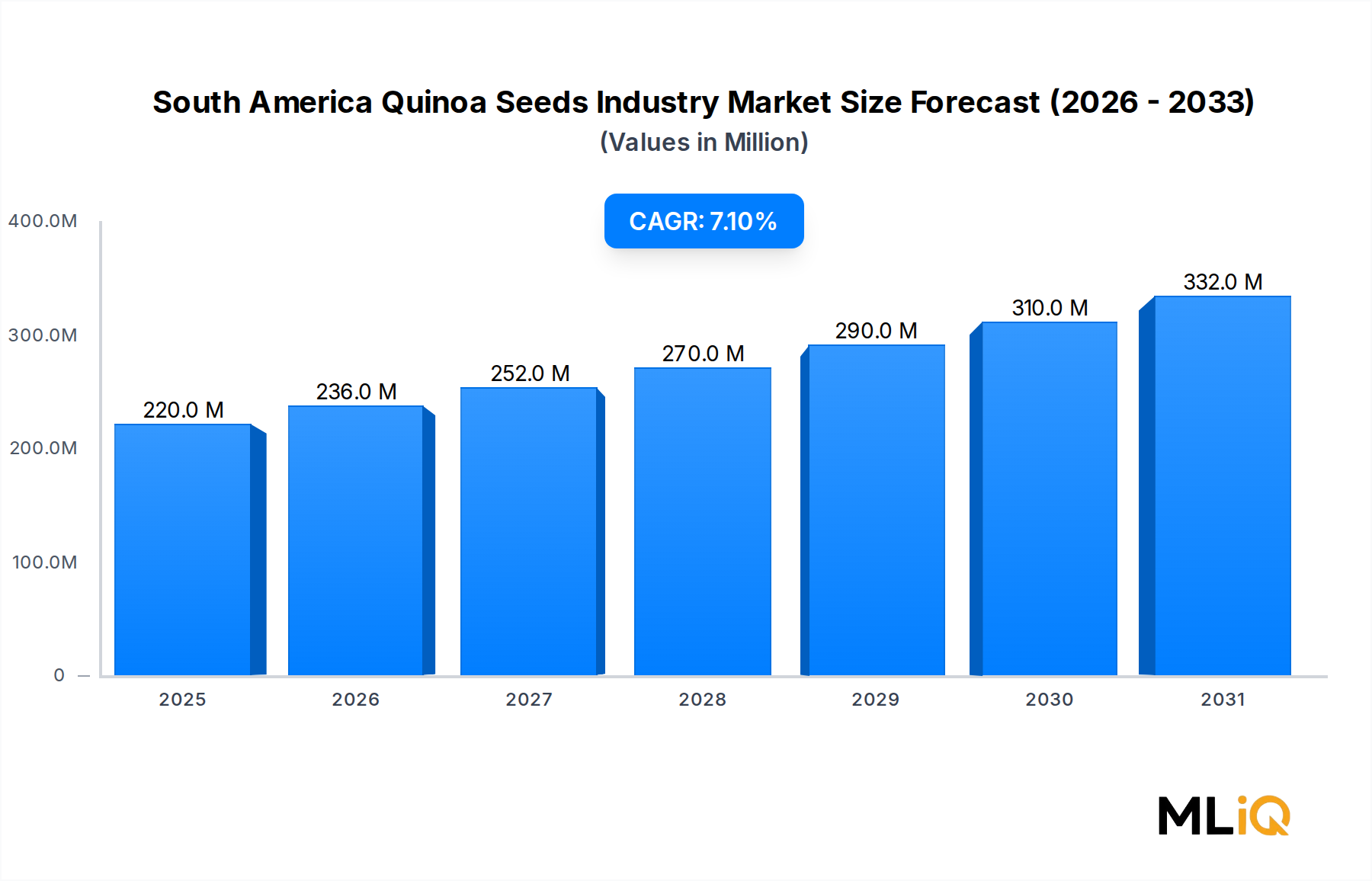

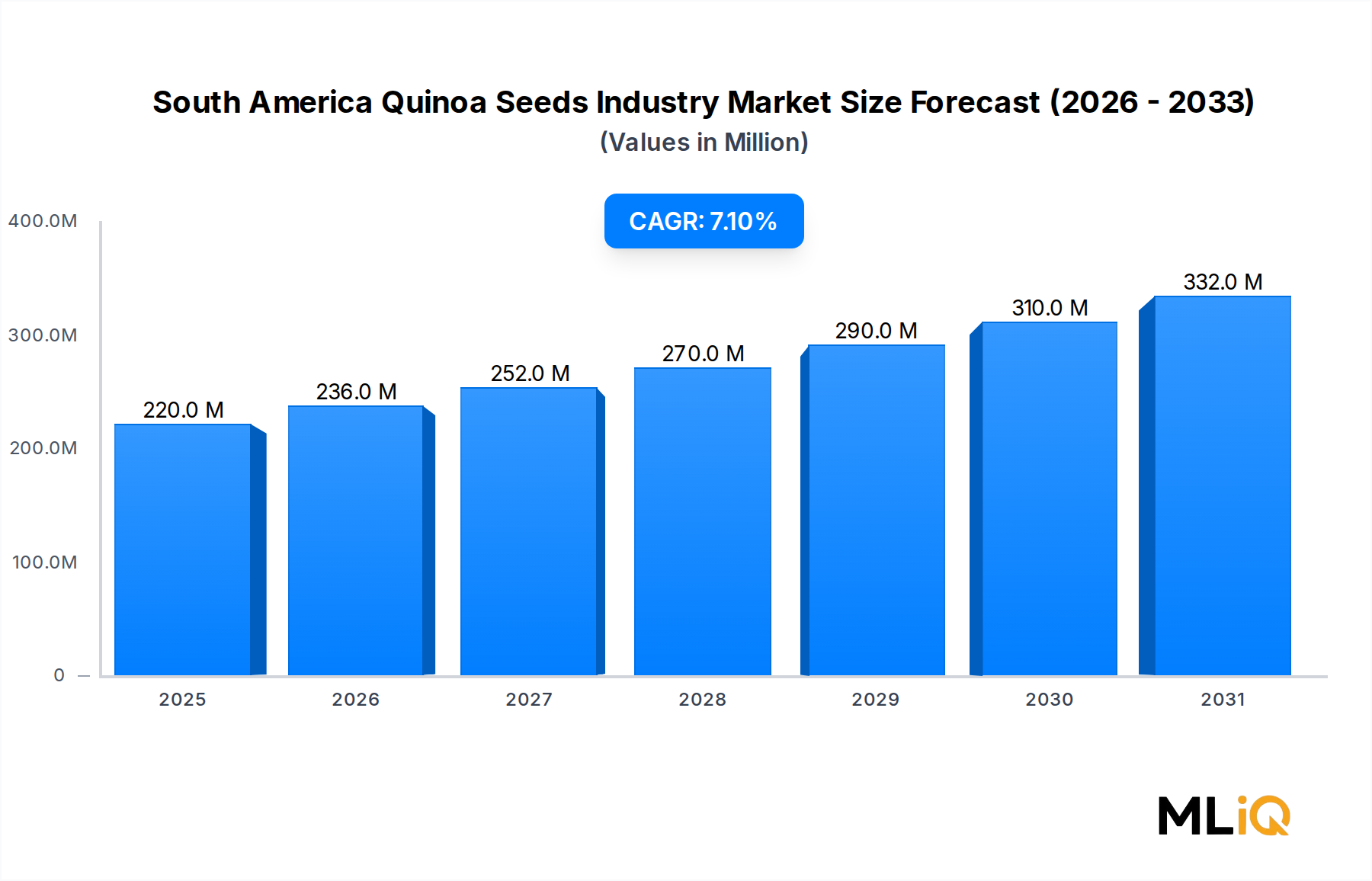

The South America Quinoa Seeds Industry Market is currently valued at $220 million and is projected to expand at a compound annual growth rate (CAGR) of 7.12% through the forecast period of 2025 to 2033. This trajectory reflects robust international demand, accelerating domestic consumption, and structural shifts in global dietary preferences that continue to favor high-protein, nutrient-dense crops.

Quinoa has historically been cultivated in the Andean highlands of Bolivia and Peru, nations that collectively account for the majority of global quinoa seed output. However, expanding agronomic research, government-backed cultivation incentives, and climate-adaptive seed varieties are broadening the geographic production footprint across Brazil and Argentina. This diversification is a critical macro tailwind, insulating the regional supply chain from altitude- and precipitation-specific yield risks.

From a demand-side perspective, rising consumer awareness around plant-based nutrition is one of the most powerful growth engines underpinning the South America Quinoa Seeds Industry Market. The global shift toward flexitarian and vegan diets has elevated quinoa's positioning as a complete protein source containing all nine essential amino acids — a distinction shared by very few plant crops. This nutritional profile has made quinoa a cornerstone ingredient in the Plant-Based Protein Market, driving consistent procurement volume from food manufacturers and ingredient processors across North America, Europe, and Asia Pacific.

Export dynamics are equally compelling. South American quinoa producers have benefited from preferential trade agreements between Andean Community nations and the European Union, facilitating tariff-reduced access to some of the most lucrative consumer markets globally. European demand, particularly from Germany, France, and the United Kingdom, for certified organic and fair-trade quinoa continues to outpace supply in certain crop cycles, reinforcing premium pricing power for certified producers.

On the technology front, precision agriculture platforms — including drone-based crop monitoring, soil microbiome analytics, and AI-assisted yield forecasting — are being deployed at scale by larger Bolivian and Peruvian agri-enterprises to optimize quinoa production. These disruptive technological integrations are expected to reduce per-unit cost of production by approximately 12–18% over the next five years, supporting margin expansion even as raw commodity pricing experiences cyclical pressure.

Looking forward through 2033, the South America Quinoa Seeds Industry Market is expected to surpass $390 million in total market value under base-case assumptions, driven by sustained export growth, premiumization of processed quinoa derivatives, and emerging demand from Southeast Asian markets where health-conscious middle-class populations are growing rapidly. Regulatory developments promoting organic certification and sustainability labeling will further differentiate South American quinoa in the global commodity landscape.

Within the South America Quinoa Seeds Industry Market, Bolivia and Peru collectively constitute the dominant production and export segment, commanding an estimated combined revenue share exceeding 68% of total regional market value. This dominance is rooted in centuries of agronomic heritage, unique high-altitude terroir, and deeply embedded institutional knowledge that cannot be rapidly replicated in emerging producing nations.

Bolivia, specifically the Altiplano plateau region, represents the world's single largest quinoa-producing zone. The country's Royal Quinoa (Quinua Real), cultivated at altitudes between 3,500 and 4,000 meters above sea level, commands a significant price premium in international markets due to its large grain size, superior protein content, and certified organic status. Bolivian quinoa exports have historically been directed toward the United States and European Union, with Germany and France being two of the most consistent high-volume buyers. The Bolivian government has progressively invested in quinoa research stations and farmer cooperatives, enabling smallholder producers — who account for approximately 75% of Bolivian quinoa cultivation — to access quality certification pipelines and export-oriented logistics infrastructure.

Peru, as the second dominant player, has diversified its quinoa cultivation across a broader range of agro-climatic zones, including coastal regions, which has enabled year-round production cycles not fully achievable in Bolivia. The Peruvian government's Quinoa Promotion Program has allocated substantial funding toward improving varietal development, post-harvest processing technology, and international marketing campaigns positioning Peruvian quinoa as a premium wellness ingredient. Peru has also developed a more advanced value-added processing industry relative to Bolivia, with a larger number of quinoa flour mills, puffed quinoa operations, and quinoa-flake production facilities operating within the country.

The dominance of these two nations is further reinforced by their leadership in organic certification. Certified organic quinoa from Bolivia and Peru commands price premiums of 25–40% over conventional varieties in European and North American retail channels, creating powerful economic incentives for continued investment in organic cultivation practices. This dynamic has stimulated significant activity in the Organic Quinoa Market, where South American producers hold a structural competitive advantage rooted in low synthetic input use historically driven by geography rather than certification compliance costs alone.

However, the dominance of Bolivia and Peru is not without competitive pressure. Argentina has emerged as a rapidly scaling quinoa producer, particularly in the provinces of Jujuy and Salta, where investments in irrigation infrastructure and varietal adaptation programs have improved yield reliability. Brazil's nascent quinoa cultivation sector, while still small in absolute terms, is attracting research investment from both public agricultural agencies and private agribusiness firms seeking to diversify quinoa supply chains domestically.

Key players operating within the Bolivian and Peruvian dominant segment include Quinoa Foods Company, Andean Valley Corporation, Cooperativa Agraria ANAPQUI, and IRUPANA Andean Organic Food. These entities range from vertically integrated export enterprises to farmer-owned cooperatives, and collectively they shape pricing dynamics, certification standards, and varietal innovation trajectories within the broader South America Quinoa Seeds Industry Market. The segment's revenue share is currently consolidating among a smaller number of larger, export-certified producers, as global buyers increasingly require supply chain traceability, sustainability documentation, and consistent quality metrics that favor organized commercial operations over fragmented smallholder supply.

The South America Quinoa Seeds Industry Market is propelled by a convergence of structural demand drivers, though several material constraints temper the pace of growth and margin expansion.

The most quantitatively significant driver is the accelerating global demand for high-protein plant foods. Global plant-based food market revenues grew at a CAGR of approximately 9.5% between 2019 and 2024, and quinoa — as a nutritionally superior grain crop — has captured a disproportionate share of ingredient procurement growth within this macro trend. Food manufacturers reformulating products to meet clean-label and allergen-free requirements have driven increased sourcing of quinoa as a functional ingredient, intersecting directly with growth in the Functional Food Ingredients Market and the Nutraceutical Ingredients Market.

Export demand from Europe remains a cornerstone driver. European imports of quinoa from South America exceeded 50,000 metric tons annually in recent crop cycles, with Germany, France, and the Netherlands functioning as primary import hubs for subsequent redistribution across the EU. The European Commission's Farm-to-Fork Strategy, which mandates reduced pesticide use and increased organic land proportion by 2030, is creating tailwinds for South American certified organic quinoa producers who already operate at low synthetic input levels.

On the constraint side, climate variability represents the most systemic risk. El Niño-related precipitation disruptions have caused yield fluctuations of up to 30% in Bolivian Altiplano regions in affected crop years, generating supply shortfalls that temporarily compress processor margins and create price spikes that destabilize long-term procurement contracts. Additionally, soil degradation from intensifying cultivation pressure on historically low-input quinoa lands presents a medium-term agronomic constraint that regional governments are only beginning to address through rotational farming incentive programs.

Currency risk and logistics infrastructure deficits further constrain market efficiency, particularly for smallholder producers in Bolivia's land-locked geography, where export freight costs represent 15–22% of FOB value — a significantly higher logistics cost burden than grain exporters in coastal South American nations face.

The competitive landscape of the South America Quinoa Seeds Industry Market is characterized by a mix of vertically integrated agri-enterprises, export-oriented cooperatives, and internationally backed ingredient processors. The following profiles represent the key participants shaping market structure and competitive dynamics:

Andean Valley Corporation: One of Bolivia's largest quinoa exporters, Andean Valley maintains vertically integrated operations spanning seed sourcing, cleaning, processing, and international logistics, supplying certified organic quinoa to retail and food service buyers across over 40 countries.

Cooperativa Agraria ANAPQUI: A Bolivian farmer-owned cooperative representing thousands of smallholder quinoa producers in the Altiplano region, ANAPQUI holds multiple fair-trade and organic certifications and has been a foundational supplier to European specialty food importers for over two decades.

IRUPANA Andean Organic Food: A Bolivian company focused on value-added quinoa processing, IRUPANA produces a range of quinoa-based consumer food products and bulk ingredients, and has expanded distribution into Latin American retail markets alongside its traditional export business.

Quinoa Foods Company: A Peru-based enterprise specializing in processed quinoa derivatives including quinoa flour and quinoa flakes, the company supplies both private-label food manufacturers and branded consumer goods companies across North American and European markets.

Grupo Orgánico Nacional (Peru): Focused on certified organic quinoa cultivation and export, this company has developed strong supply chain traceability systems and works closely with international buyers requiring documented sustainability metrics.

AgroAndina (Argentina): An emerging Argentinian producer leveraging government-supported agri-technology programs in the northwestern provinces, AgroAndina is positioning Argentine quinoa as a cost-competitive alternative to Bolivian and Peruvian origin product for bulk ingredient buyers.

Empresa Brasileira de Pesquisa Agropecuária (EMBRAPA): Brazil's federal agricultural research agency is playing a catalytic role in developing quinoa varieties adapted to lower-altitude Brazilian growing conditions, with commercial cultivation partnerships beginning to generate commercially meaningful output volumes.

March 2023: The Bolivian Ministry of Rural Development and Land launched a national quinoa genetic diversity preservation program, committing $4.2 million to catalog and protect over 3,000 quinoa ecotypes held in the national gene bank, with implications for long-term varietal innovation pipelines.

July 2023: The European Union and the Andean Community concluded a revised phytosanitary protocol reducing certification processing times for organic quinoa imports, an administrative improvement expected to reduce compliance costs for Bolivian and Peruvian exporters by approximately 8% annually.

November 2023: EMBRAPA published results from a multi-year quinoa adaptation trial in Brazil's Cerrado region, reporting yields of 1.8 metric tons per hectare under drip irrigation conditions — a figure approaching commercial viability thresholds for Brazilian agribusinesses.

February 2024: Andean Valley Corporation announced a strategic supply agreement with a major European private-label retailer for a five-year certified organic quinoa supply contract, representing one of the largest single long-term procurement commitments in the sector's recent history.

June 2024: Peru's Ministry of Agrarian Development unveiled a $12 million public-private investment program targeting quinoa value chain modernization, including post-harvest processing facility upgrades and export marketing support through 2027.

October 2024: A consortium of South American quinoa producers formally submitted a proposal to the United Nations Food and Agriculture Organization for quinoa's inclusion in the FAO Strategic Framework for Sustainable Agriculture, seeking multilateral recognition that could unlock additional development financing.

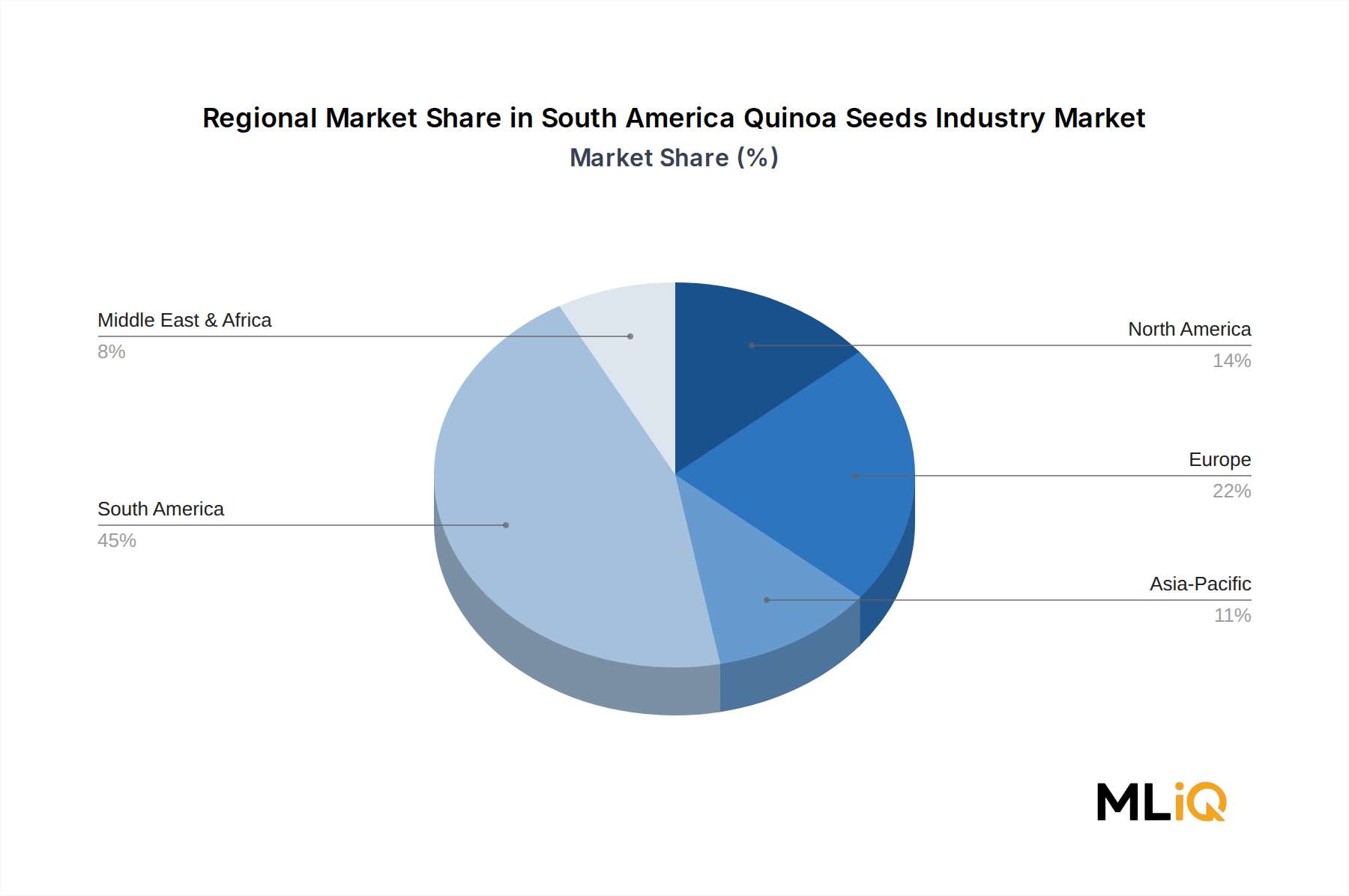

The South America Quinoa Seeds Industry Market exhibits pronounced regional heterogeneity in terms of production volume, export orientation, value-addition capability, and growth trajectory.

Bolivia remains the production epicenter of the South America Quinoa Seeds Industry Market, accounting for an estimated 38–42% of total regional revenue. The Bolivian market segment grows at an estimated CAGR of 6.4%, slightly below the regional average, reflecting the maturity of its quinoa export infrastructure and the slower pace of domestic value-added processing development. The primary demand driver in Bolivia is sustained European premium import demand for Royal Quinoa origin-certified product.

Peru represents the second-largest segment, contributing approximately 28–32% of regional revenue and growing at a CAGR of approximately 7.8% — marginally above the regional average. Peru's faster growth rate reflects its more advanced domestic processing industry, diversified export market portfolio including rapidly expanding Asian buyer relationships, and government-backed quinoa promotion programs. The country's coastal quinoa production zones additionally provide supply resilience advantages that Bolivia lacks.

Argentina is the fastest-growing national segment within the South America Quinoa Seeds Industry Market, with an estimated CAGR of 11.2% driven from a comparatively low production base. Investment in irrigation infrastructure, seed adaptation research, and proximity to existing agricultural export logistics corridors are enabling rapid capacity scale-up. Argentina's quinoa output is primarily targeting bulk ingredient buyers seeking cost-competitive sourcing alternatives.

Brazil, while currently a minor contributor with less than 5% of regional market revenue, is exhibiting the most dynamic institutional investment trajectory. EMBRAPA's research programs and growing interest from large domestic food manufacturers in locally sourced quinoa — consistent with Brazil's broader food security diversification policy objectives — position Brazil as a watch-market for disproportionate growth post-2027.

The Rest of South America segment, including Chile and Ecuador, accounts for a modest share of regional revenue but plays a role in specialty organic production niches and in supplying domestic health food retail channels that are growing at double-digit rates in urbanizing consumer markets.

Investment activity in the South America Quinoa Seeds Industry Market has intensified meaningfully over the 2022–2024 period, with capital flows concentrating across three primary sub-segments: certified organic production infrastructure, post-harvest processing technology, and supply chain traceability platforms.

On the M&A front, several mid-sized Bolivian and Peruvian quinoa exporters have been targeted for strategic acquisition by European and North American health food conglomerates seeking to secure vertically integrated quinoa supply chains. These transactions have been motivated by persistent supply chain disruptions experienced during the 2020–2022 period, which exposed the vulnerability of spot-market procurement strategies for quinoa-dependent product lines. Acquirers have prioritized targets with existing organic certifications, established farmer cooperative networks, and documented traceability systems — characteristics that command significant valuation premiums in transaction negotiations.

Venture funding has flowed predominantly into agri-technology startups applying precision agriculture tools to quinoa cultivation optimization. Bolivian and Peruvian agri-tech firms offering drone-based crop health monitoring, satellite soil analysis services, and AI-assisted irrigation scheduling have collectively attracted an estimated $35–45 million in venture and development finance capital between 2022 and 2024. Development finance institutions including the Inter-American Development Bank and the International Finance Corporation have been active co-investors alongside private venture capital in several of these technology deployments.

Strategic partnerships between South American quinoa producers and global food ingredient companies have also proliferated, with multi-year offtake agreements increasingly incorporating sustainability performance metrics — including soil carbon sequestration benchmarks and water use efficiency targets — as contractual terms rather than aspirational commitments. This evolution reflects growing buyer pressure from corporate sustainability reporting requirements under frameworks such as the Science Based Targets initiative.

The Gluten-Free Products Market and the Ancient Grains Market have been identified by investment analysts as the sub-segments generating the highest quinoa ingredient demand growth, and capital allocation within the quinoa value chain is disproportionately concentrated in processing facilities capable of producing gluten-free certified quinoa derivatives to pharmaceutical-grade purity standards.

The customer base of the South America Quinoa Seeds Industry Market is segmented across four primary buyer categories, each exhibiting distinct purchasing criteria, price sensitivity profiles, and procurement channel preferences.

Food manufacturers and ingredient processors represent the largest buyer

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.12% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the South America Quinoa Seeds Industry market expansion.

Key companies in the market include .

The market segments include Country, Price Trend Analysis.

The market size is estimated to be USD 220 million as of 2022.

N/A

High Regional Exports to European Countries.

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "South America Quinoa Seeds Industry," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the South America Quinoa Seeds Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.