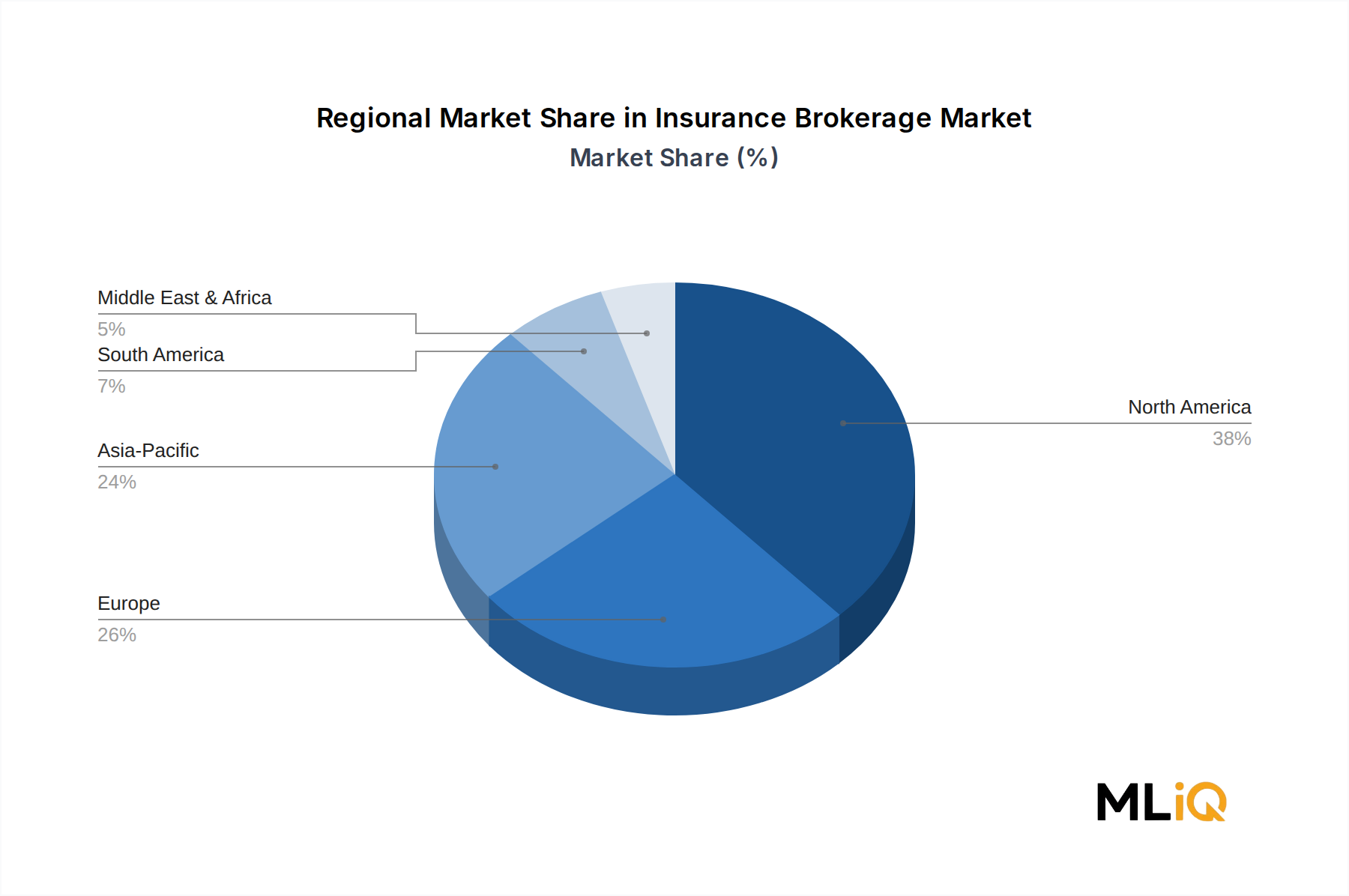

The Insurance Brokerage Market exhibits pronounced regional variation in growth rates, competitive dynamics, and primary demand drivers, reflecting underlying differences in insurance penetration, regulatory maturity, and economic development trajectories.

North America represents the largest regional market, accounting for an estimated 40–42% of total global brokerage revenue. The United States market is the primary driver, underpinned by deep commercial insurance penetration, a sophisticated specialty lines ecosystem, and a highly active M&A environment among mid-market brokers. Canada and Mexico contribute incrementally, with Canada's market characterized by strong employee benefits brokerage activity and Mexico exhibiting accelerating growth as formal commercial insurance adoption expands among SME clients. The North American market is the most mature globally, with projected growth tracking near the global average CAGR of 9.3%.

Europe constitutes the second-largest regional block, with the United Kingdom serving as the global hub for specialty and wholesale brokerage through the Lloyd's of London marketplace. Germany, France, and the Nordics are significant commercial lines markets, while regulatory harmonization under the EU's Insurance Distribution Directive has standardized conduct requirements across member states. European market growth is expected to be modestly below the global average, constrained by relatively high existing insurance penetration and fee compression from regulatory disclosure mandates.

Asia Pacific is the fastest-growing regional market, projected to deliver a CAGR materially above the global average through 2033. China and India represent the primary growth engines, driven by expanding middle-class populations, rising corporate risk awareness, and government-mandated insurance requirements in sectors including agriculture, construction, and financial services. ASEAN markets—particularly Indonesia, Vietnam, and Thailand—are experiencing accelerating growth in retail and SME commercial lines brokerage. Japan and South Korea represent more mature sub-markets with stable but lower-growth trajectories.

The Middle East and Africa region is experiencing robust growth, particularly within the GCC states where large-scale infrastructure investment programs and expanding financial services ecosystems are generating substantial commercial insurance demand. South Africa remains the most sophisticated African brokerage market by penetration and broker infrastructure.

South America's growth is concentrated in Brazil and, to a lesser extent, Argentina, where macroeconomic stabilization and expanding agricultural insurance programs are supporting brokerage activity. Political and currency risk volatility tempers the pace of foreign broker investment in this region.