Multi Peril Crop Insurance Dominance in the Crop Insurance Market

Multi Peril Crop Insurance (MPCI) represents the dominant coverage segment within the global Crop Insurance Market, commanding the largest share of gross written premiums and policyholder adoption across nearly all major agricultural economies. MPCI policies are designed to protect farmers against a broad spectrum of yield-reducing risks including drought, flood, hail, frost, disease, and pest infestations under a single umbrella contract, distinguishing them sharply from named-peril or single-risk policies that only cover explicitly defined events.

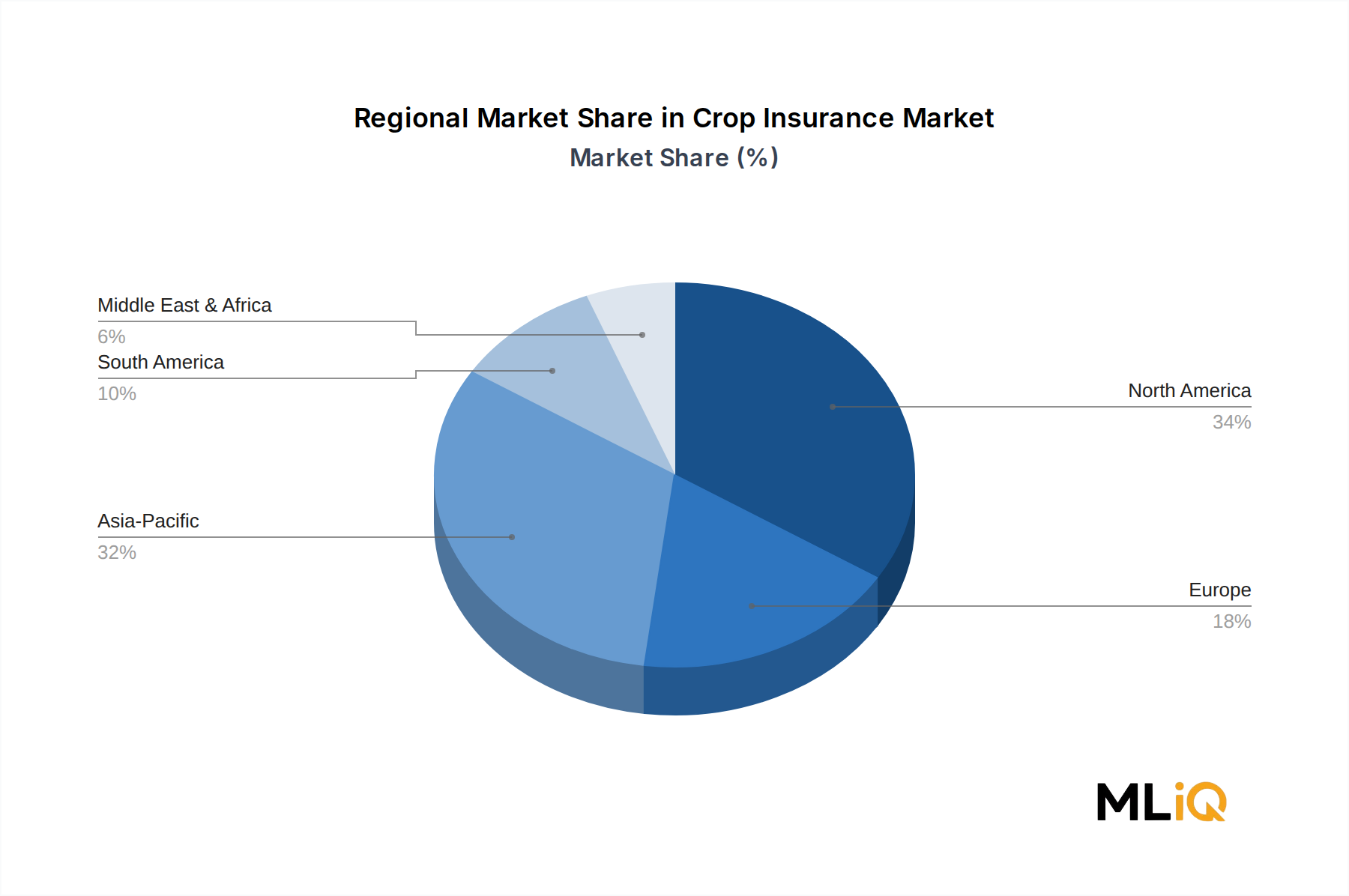

The structural dominance of MPCI stems primarily from the comprehensive risk coverage it affords, which aligns directly with the multi-dimensional exposure profile of modern commercial farming operations. As climate change has rendered weather patterns increasingly erratic and unpredictable, the demand for holistic protection instruments has intensified. Farmers operating at scale — particularly in the United States, India, China, Brazil, and Canada — are increasingly unable or unwilling to absorb the basis risk associated with narrower coverage products, reinforcing MPCI's lead position.

In the United States, the Federal Crop Insurance Program (FCIP), administered by the Risk Management Agency (RMA) under the USDA, provides heavily subsidized MPCI products to over 1.1 million policyholders annually, covering approximately 380 million acres of cropland. Premium subsidies averaging 60% of the actuarial cost ensure broad participation and make MPCI the default risk management tool for American farmers. Similar architectures exist in India through the Pradhan Mantri Fasal Bima Yojana (PMFBY) scheme, which mandates MPCI coverage for loanee farmers and has enrolled more than 55 million farmer applications in recent cycles.

Key players operating prominently within the MPCI sub-segment include PICC in China, which leverages its state-backed distribution network to dominate domestic multi-peril programs; Agriculture Insurance Company of India Limited (AIC), which functions as the primary implementing agency for government-backed MPCI schemes; and American Financial Group, which underwrites substantial MPCI volumes through its Great American Insurance subsidiary. Chubb and QBE Insurance Group Limited have also made targeted investments in MPCI product innovation across Asia Pacific markets, combining actuarial rigor with precision agriculture data inputs.

From a market share perspective, MPCI's dominance is consolidating rather than fragmenting. As remote sensing data, drone-based crop monitoring, and algorithmic loss assessment tools become more accessible, the unit economics of underwriting MPCI products are improving structurally. Insurers can now better differentiate risk at the individual field or micro-zone level rather than relying solely on county-level or regional loss ratios, reducing adverse selection and enabling more competitive premium structures.

The MPCI segment is further buttressed by growing private reinsurance capacity. Major reinsurers operating in the broader Reinsurance Market have increased their appetite for agricultural excess-of-loss treaties as portfolio diversification tools, given the low correlation of crop yield risk with traditional financial and catastrophe perils. This capital inflow is enabling primary insurers to expand MPCI capacity and enter previously underserved geographies without proportionally increasing their net retained risk exposure.

Looking ahead, MPCI is expected to maintain its dominance through 2033, with growth particularly pronounced in emerging markets where government-mandated coverage expansion programs are scaling rapidly. The integration of parametric triggers within hybrid MPCI structures — a convergence with the Parametric Insurance Market — is also emerging as a critical product innovation pathway, enabling faster claims settlements and reducing moral hazard concerns that have historically constrained MPCI adoption in lower-trust environments.