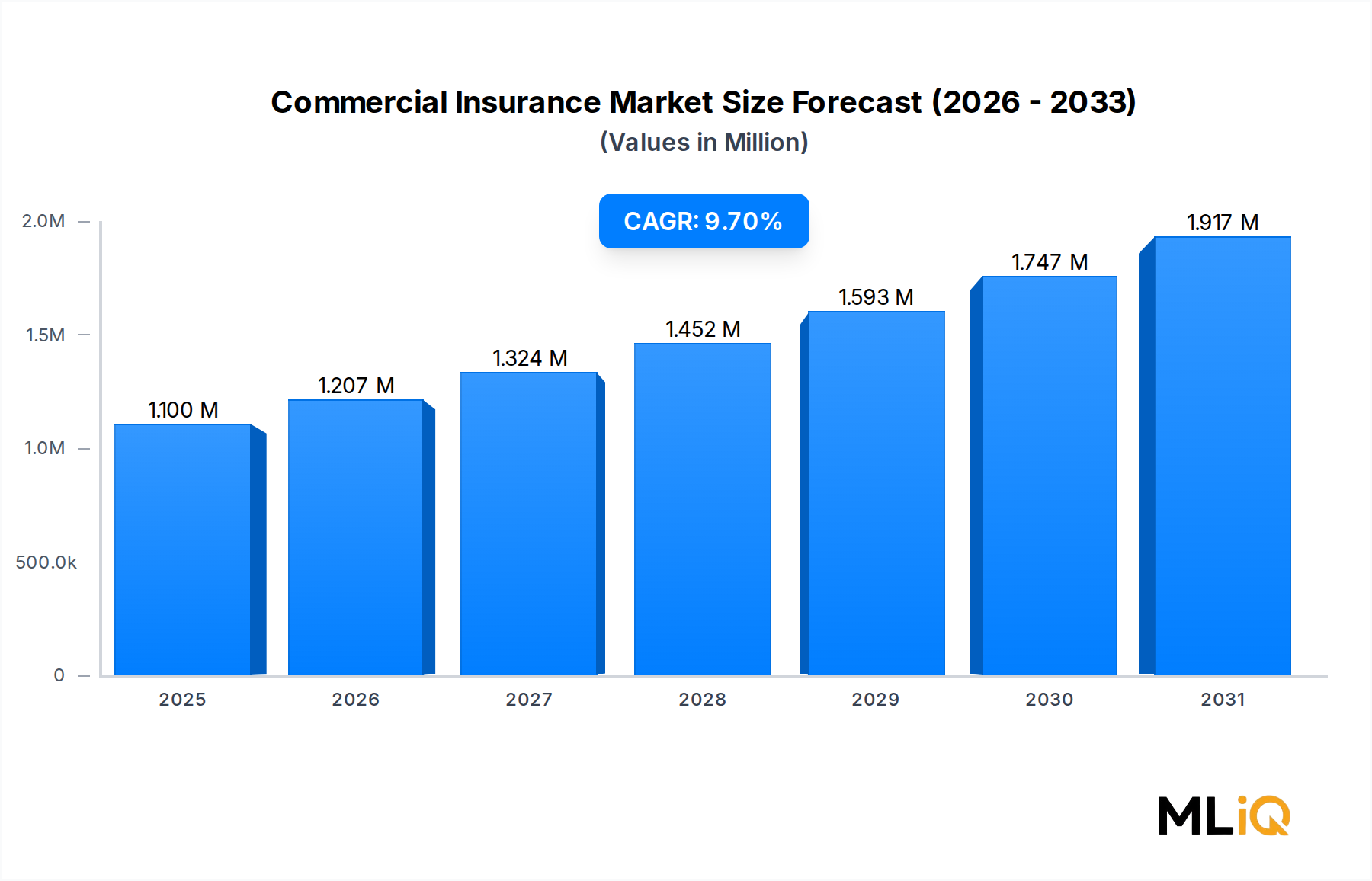

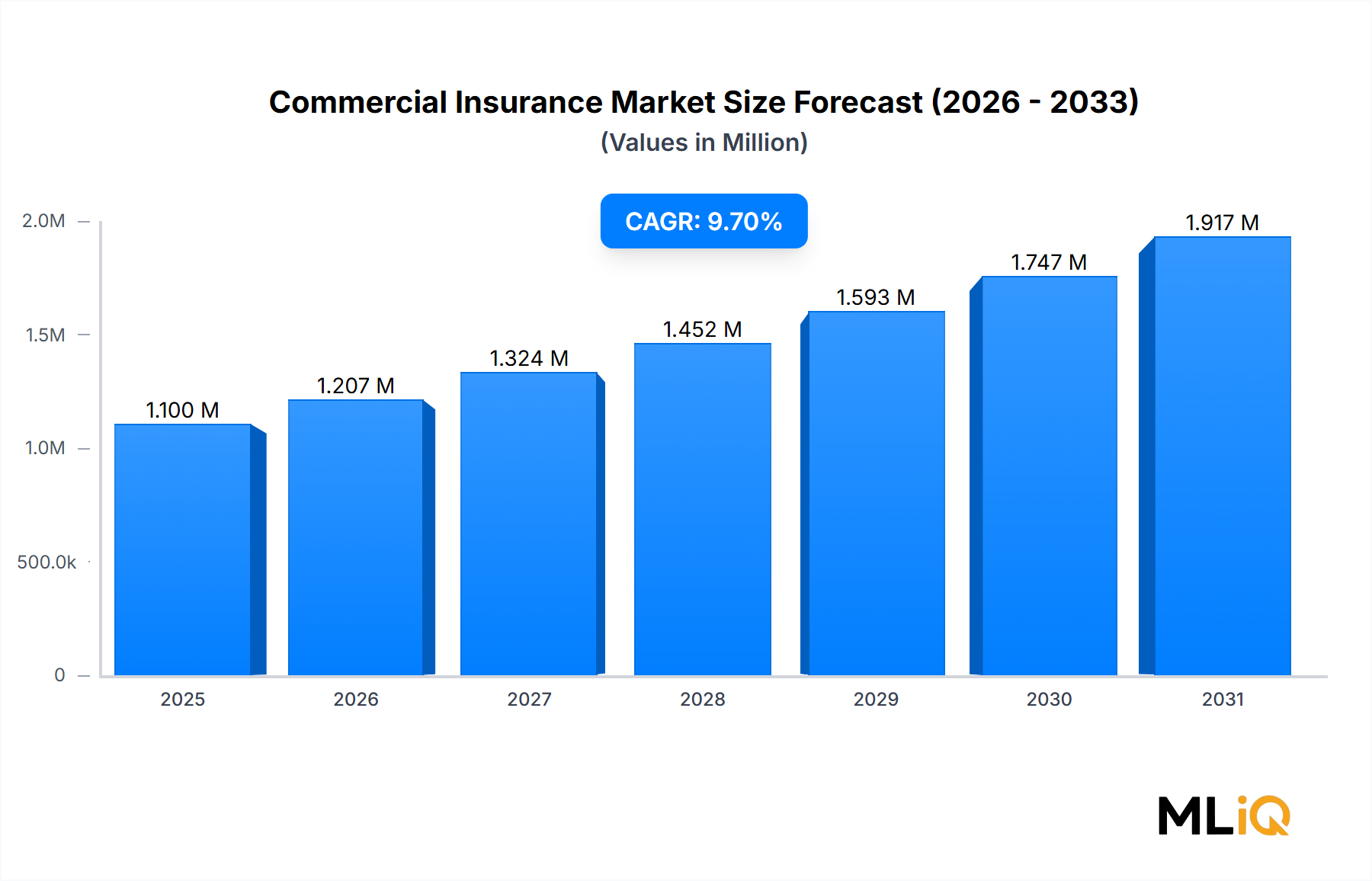

The global Commercial Insurance Market is projected to reach a valuation of $1,099.88 billion, expanding at a compound annual growth rate (CAGR) of 9.7% over the forecast period. This robust trajectory reflects deep structural demand from enterprises seeking financial protection against an increasingly complex and volatile risk environment. Rising operational risks, expanding regulatory obligations, and the digital transformation of core business processes have collectively reinforced the strategic imperative for comprehensive commercial insurance coverage worldwide.

At its foundation, the market benefits from converging macro tailwinds. Climate-related catastrophic losses have surged in frequency and magnitude, compelling businesses across sectors — from manufacturing to logistics — to reassess their coverage adequacy. Simultaneously, stricter regulatory frameworks in North America, Europe, and select Asia Pacific economies are mandating higher minimum coverage thresholds, particularly in liability and property insurance sub-segments. This regulatory pressure is translating directly into premium volume growth for carriers and brokers alike.

Digital penetration is another critical accelerant. The proliferation of connected devices, cloud infrastructure, and AI-driven underwriting platforms is enabling insurers to price risk more accurately, reduce loss ratios, and unlock previously underserved segments of the small and medium enterprise (SME) landscape. Insurers leveraging telematics, real-time IoT data, and predictive analytics are achieving materially lower combined ratios while extending their addressable markets.

The healthcare, IT and telecom, and energy verticals are emerging as particularly high-growth end markets. Healthcare organizations face mounting malpractice and cyber exposure; tech firms confront evolving data breach and intellectual property risks; and energy companies are navigating both physical asset risks and rapidly shifting ESG-linked liability profiles. These sector-specific dynamics are feeding strong demand across multiple commercial insurance product lines.

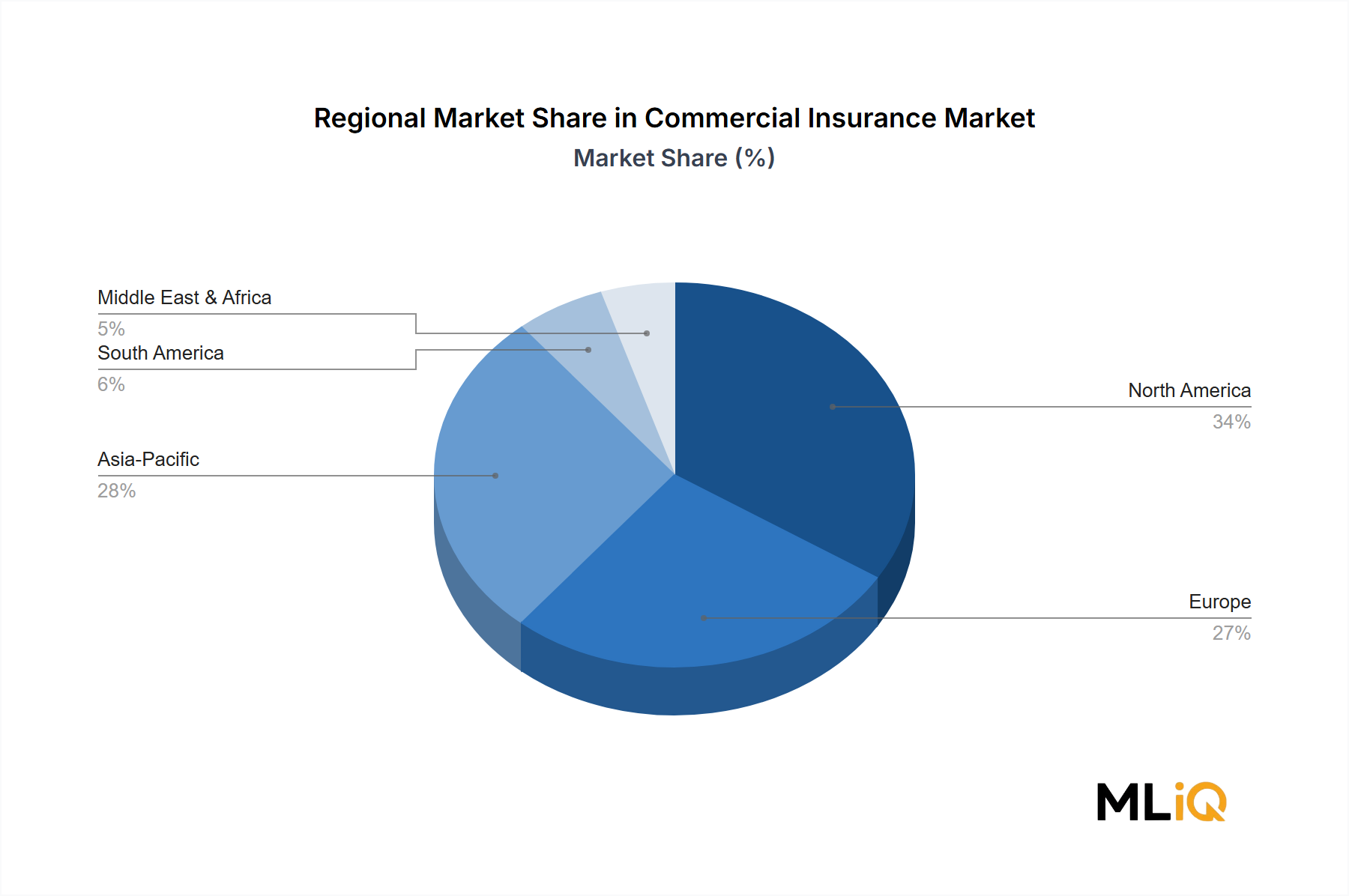

Geographically, North America continues to command the largest revenue share, supported by a mature insurance ecosystem and high penetration rates. However, the Asia Pacific region is the fastest-growing, driven by rapid industrialization, expanding SME ecosystems, and rising insurance awareness in China, India, and Southeast Asia. Europe remains a significant and stable contributor, with ongoing regulatory harmonization under Solvency II frameworks providing structural support.

Looking forward, the Commercial Insurance Market is poised for sustained expansion. The convergence of climate risk repricing, cyber threat escalation, and enterprise digitalization is broadening the insurance product spectrum, creating fertile ground for innovation in parametric insurance, usage-based models, and embedded insurance solutions. Market participants that invest in data infrastructure and distribution diversification will be best positioned to capture disproportionate share of this growth trajectory over the coming decade.