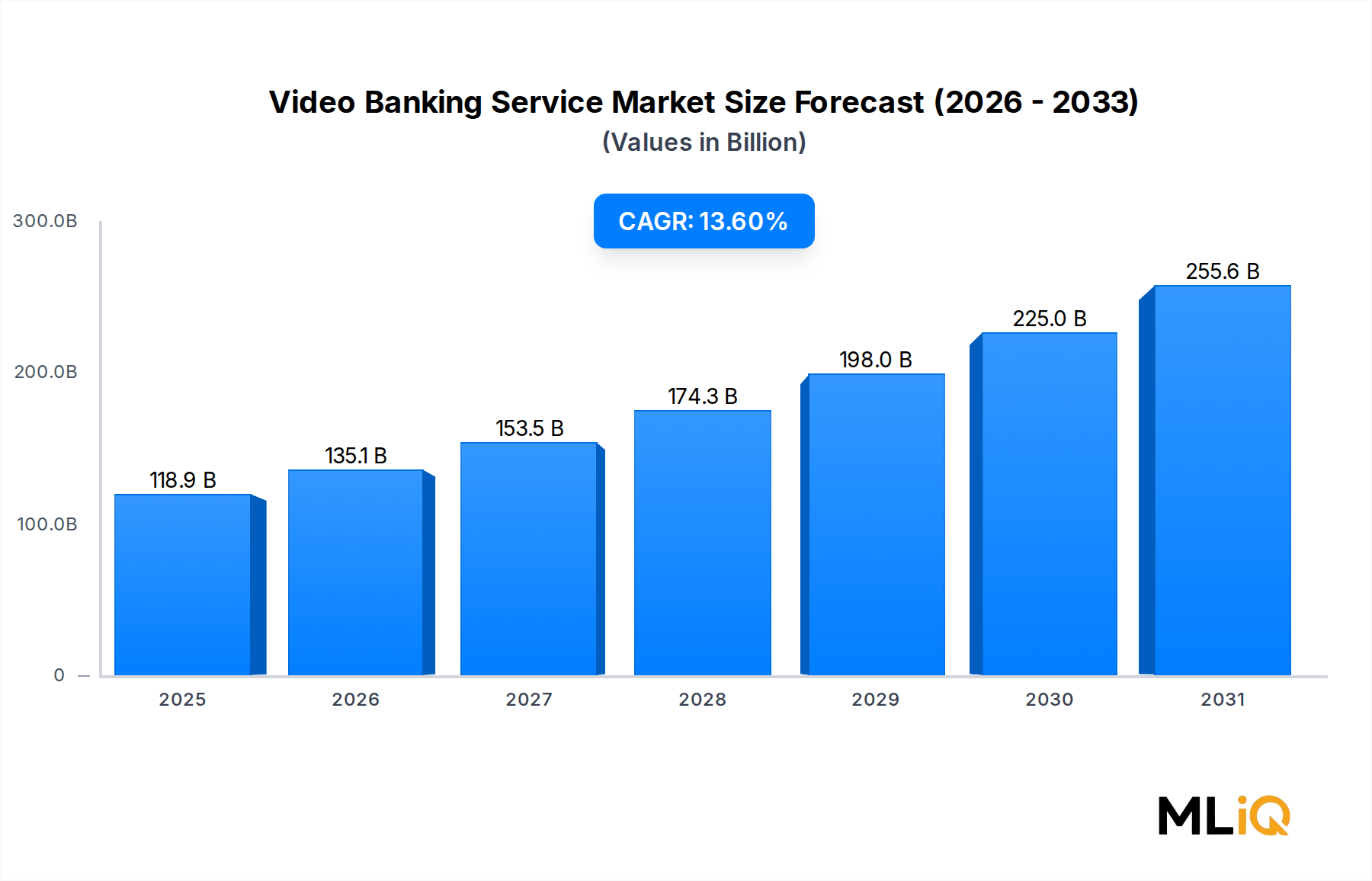

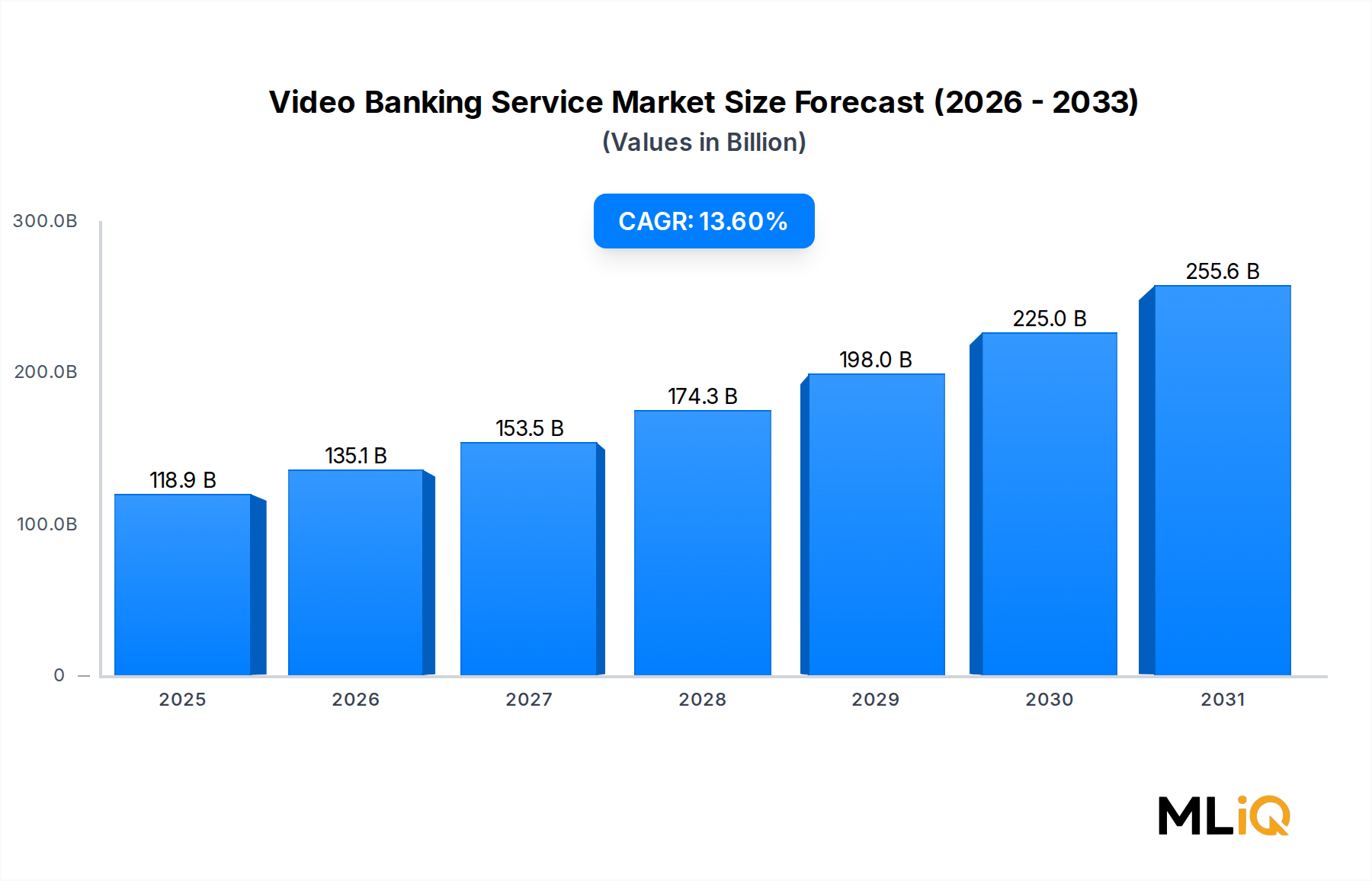

Solution Segment Dominance in the Video Banking Service Market

Within the Video Banking Service Market, the Solution segment commands the largest revenue share, accounting for the majority of total market value throughout the forecast horizon. This dominance is rooted in the comprehensive, platform-level capabilities that solution providers deliver — encompassing video communication engines, identity verification modules, session recording and compliance tools, digital signature integration, screen sharing functionality, and CRM connectivity.

Financial institutions consistently prioritize investment in end-to-end solution platforms over standalone service engagements because a holistic solution reduces integration complexity, vendor fragmentation, and long-term operational costs. Enterprise procurement committees within banks and credit unions evaluate video banking solutions against stringent criteria including uptime SLAs (typically above 99.9%), end-to-end encryption compliance with standards such as TLS 1.3 and AES-256, and compatibility with core banking systems from vendors like Temenos, FIS, and Finastra.

Glia Technologies, Inc. stands as a pivotal player in the solution segment, offering a Digital Customer Service platform that integrates video, voice, messaging, and AI-assisted cobrowsing within a single unified interface. Their architecture is designed specifically for regulated financial environments, with built-in compliance and audit trail capabilities that satisfy both consumer protection regulations and internal risk management requirements.

Barclays and U.S. Bank have both deployed proprietary or white-labeled video banking solutions that serve as the backbone of their digital advisory offerings, particularly for wealth management, mortgage consultations, and small business lending. The ability to conduct high-value, complex financial discussions through a secure, authenticated video channel has measurably improved customer satisfaction scores and reduced time-to-close for loan origination workflows.

The solution segment's share is not merely holding steady — it is consolidating further as financial institutions deepen their digital transformation commitments. Annual IT spending by global banks on digital channels and customer-facing technology continues to grow, with video banking solutions increasingly classified as core infrastructure rather than optional enhancement. This reclassification drives multi-year licensing agreements and enterprise-wide rollouts rather than pilot-scale deployments.

Cloud-native solution architectures are particularly dominant within this segment, enabling institutions to deploy updates, scale capacity during high-demand periods (such as tax season or market volatility events), and integrate new AI capabilities without disruptive re-platforming. Vendors offering microservices-based, API-first video banking solutions are capturing disproportionate market share relative to legacy on-premise competitors.

The shift in the Credit Union Technology Market also reinforces solution segment growth, as smaller cooperative institutions seek turnkey platforms that eliminate the need for large internal engineering teams. Vendors such as Glia Technologies, Inc. have specifically tailored their go-to-market strategies for credit unions, offering preconfigured compliance templates and rapid deployment packages that reduce time-to-value from months to weeks. This democratization of enterprise-grade video banking solutions across institutions of all sizes is a key structural driver of the segment's sustained dominance.