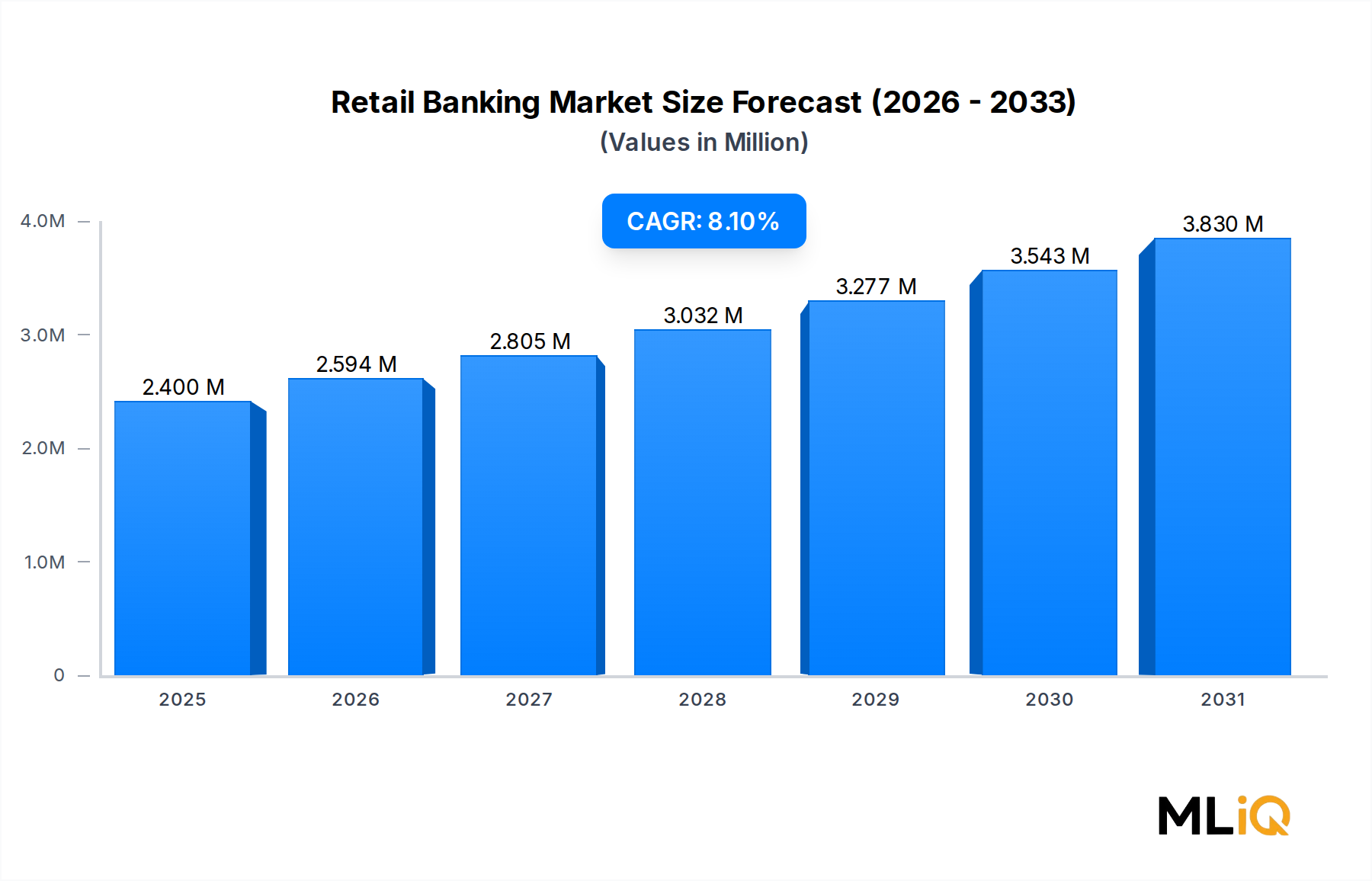

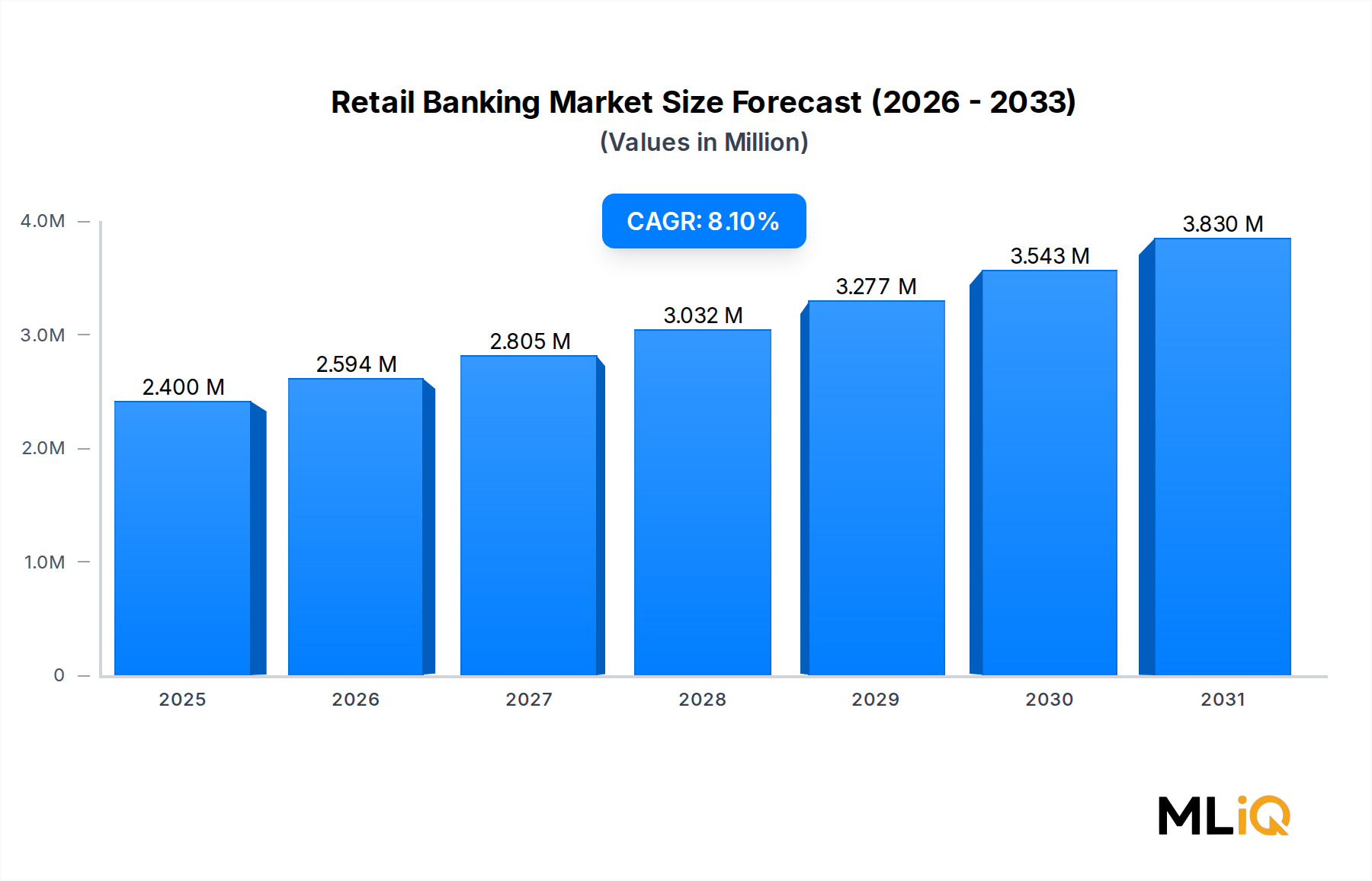

The global Retail Banking Market is valued at $2.40 trillion as of the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 8.1% through 2033, reflecting robust structural demand across consumer financial services worldwide. This trajectory positions the market to surpass $5.0 trillion by the end of the forecast horizon, underpinned by accelerating digital adoption, population-driven financial inclusion, and evolving consumer expectations across both mature and emerging economies.

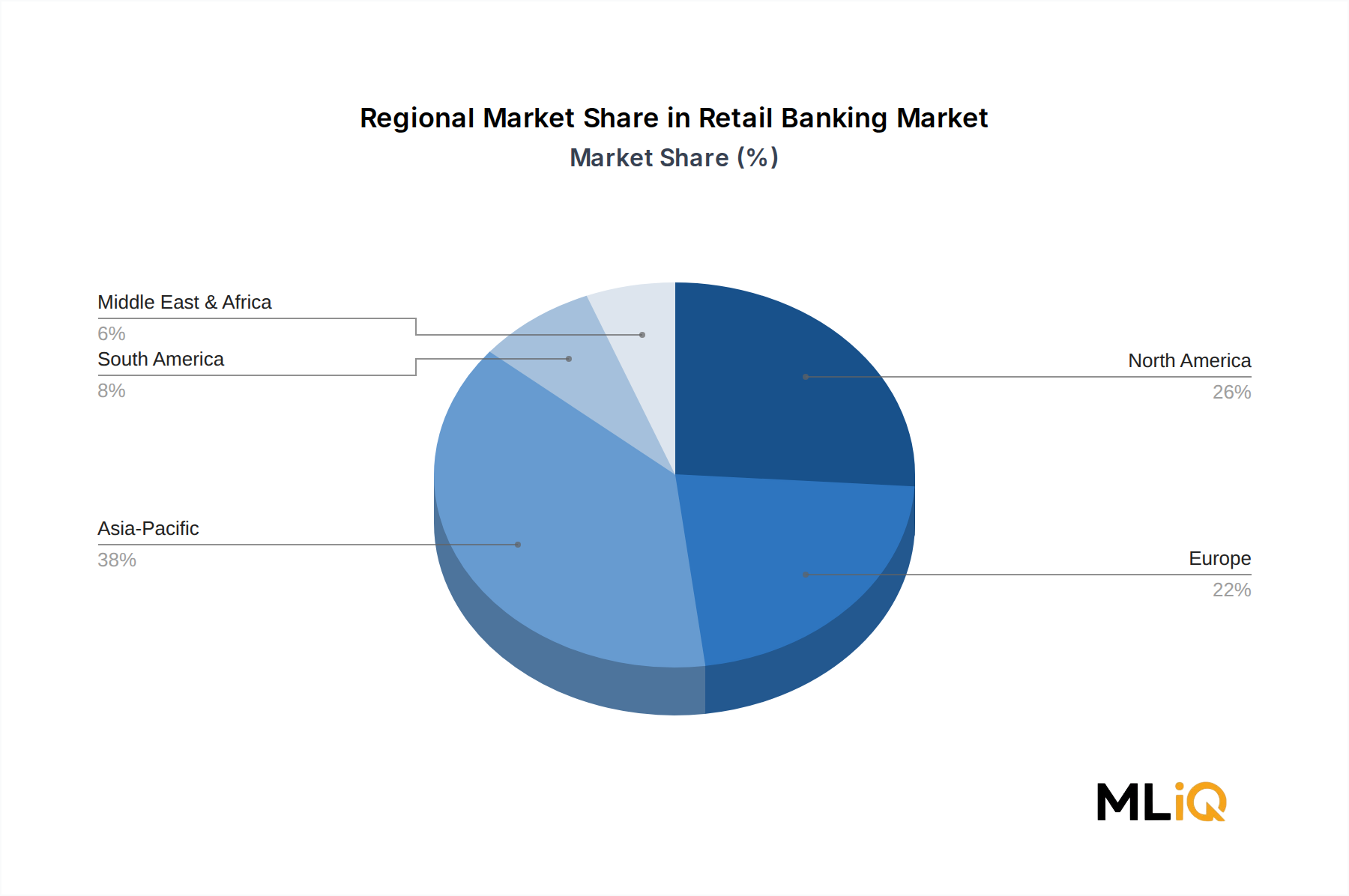

Several macro tailwinds are converging to sustain this momentum. First, the global unbanked and underbanked population—estimated at over 1.4 billion adults—presents a significant addressable opportunity, particularly across Asia Pacific, Sub-Saharan Africa, and Latin America. Second, rising disposable incomes and expanding middle-class demographics in India, China, Southeast Asia, and Brazil are translating directly into increased demand for core retail banking products including savings accounts, personal credit, and insurance-linked deposits. Third, the maturation of smartphone ecosystems and high-speed broadband penetration is enabling institutions to deliver cost-effective, scalable services at the branch-free level.

From a product perspective, demand for digitally delivered checking and savings accounts, consumer credit, and investment-linked banking packages is growing at a pace that outstrips traditional branch-based service delivery. Regulatory modernization—including open banking mandates across the European Union, the United Kingdom, and Australia—is further disrupting legacy service models by enabling third-party financial providers to compete directly within core retail banking workflows.

The Digital Banking Market, the Mobile Payments Market, and the Consumer Lending Market each serve as critical adjacent growth engines for retail banking institutions seeking to diversify revenue streams beyond net interest income. Simultaneously, incumbents are integrating capabilities from the Financial Technology Market to modernize core infrastructure and reduce operational cost ratios.

Forward-looking indicators suggest that the 2025–2028 window will be marked by heightened merger and acquisition activity, particularly in markets where digital-native challenger banks are gaining meaningful deposit share from traditional brick-and-mortar players. Tier-1 global banks are expected to accelerate investment in cloud-native core banking platforms, AI-driven credit decisioning, and real-time payment rails to defend margin and improve customer lifetime value metrics. The market's 8.1% CAGR therefore reflects not just volume expansion, but a fundamental repricing of how retail banking services are delivered, monetized, and regulated across the global financial system.