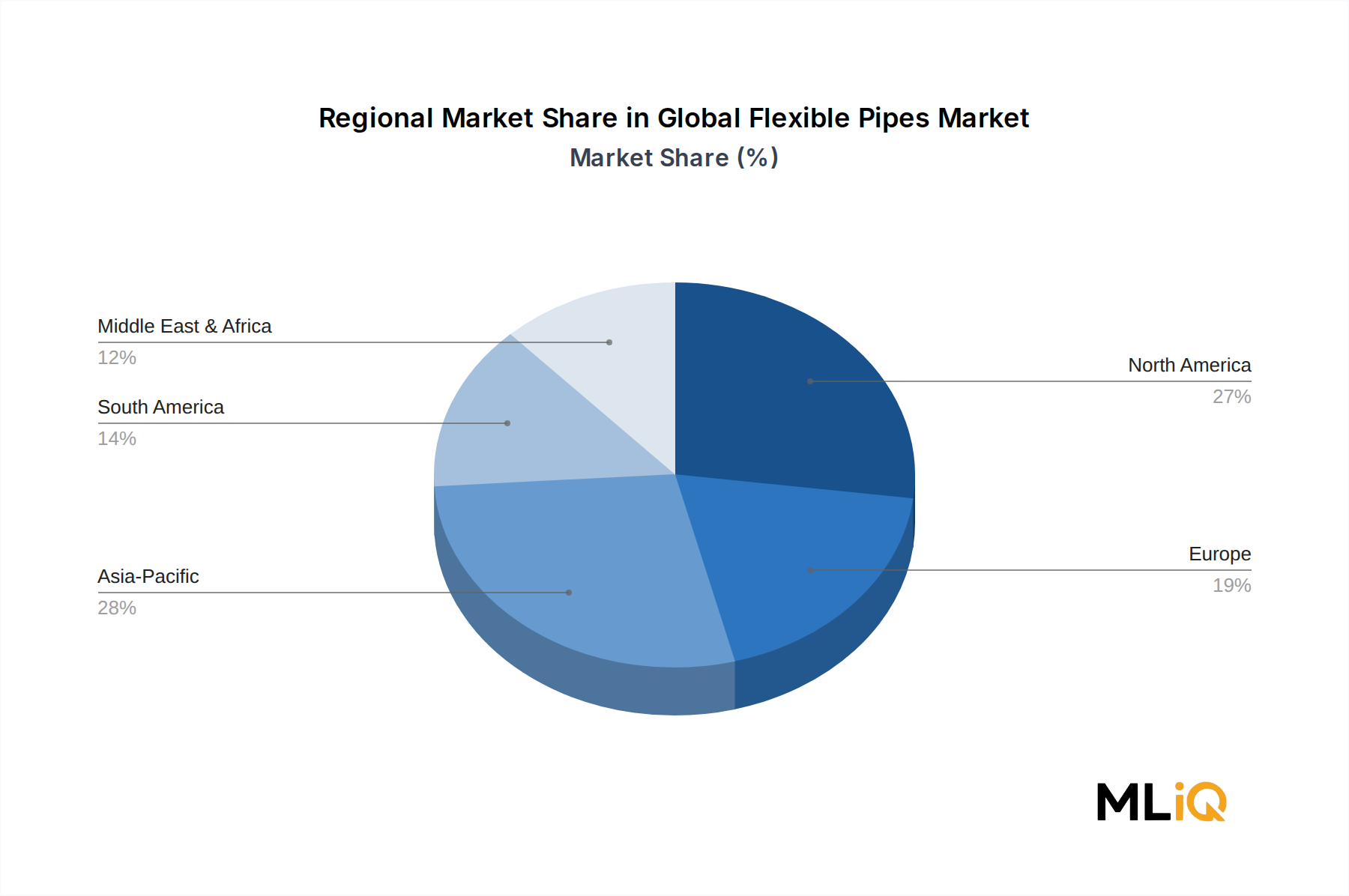

The Global Flexible Pipes Market exhibits pronounced regional differentiation in growth rates, demand drivers, and competitive dynamics, reflecting the geographic distribution of offshore hydrocarbon reserves, infrastructure investment cycles, and industrial development trajectories.

North America accounted for an estimated 28–30% of global flexible pipe revenue in 2024, driven primarily by onshore shale and tight oil gathering infrastructure demand in the United States and a growing deepwater Gulf of Mexico development pipeline. The region's onshore flexible pipe segment has benefited from operator preference for corrosion-resistant polymer alternatives to carbon steel gathering lines, particularly in the Permian Basin where produced water volumes and corrosive fluid compositions impose high maintenance costs on conventional steel systems. Canada's oil sands sector provides additional demand for flexible pipe in thermal recovery and steam injection applications. North America is projected to grow at approximately 4.2% CAGR through 2033, slightly below the global average, as market maturity moderates the growth ceiling in the onshore segment.

South America, led overwhelmingly by Brazil, represents the most significant single-country market for offshore flexible pipe globally. Petrobras's sustained capital program in the pre-salt Santos and Campos basins, which involves the continuous sanctioning of new FPSO units, generates structural baseline demand for flexible risers and flowlines that is expected to persist through the entire forecast period. Brazil is estimated to represent approximately 20–22% of global offshore flexible pipe demand and is projected to grow at a CAGR of 5.5–6.0% through 2033, making South America the second-fastest growing region overall.

Europe, centered on the North Sea ecosystem spanning the United Kingdom, Norway, and the Netherlands, represents a mature but reinvestment-active market. Late-life field extension programs and tieback development strategies are generating flexible pipe demand for shorter, lower-cost subsea tiebacks connecting satellite fields to existing infrastructure. The region's growth rate is estimated at 3.5–4.0% CAGR through 2033, reflecting market maturity offset by energy security investment following 2022 supply disruptions. The Oil and Gas Pipeline Market in Europe has seen increased investment in infrastructure resilience, indirectly supporting flexible pipe demand.

Asia Pacific is identified as the fastest-growing regional market, with a projected CAGR of 6.0–6.5% through 2033. Offshore field development activity in the South China Sea, India's deepwater blocks, and Australia's LNG infrastructure expansion are the primary drivers. The Industrial Hose Market in Asia Pacific is also growing rapidly, with chemical processing and mining sector demand for flexible polymer piping adding a significant industrial demand layer to the region's offshore-led growth story. China and India collectively account for the majority of regional volume growth.

Middle East and Africa is an emerging growth market, with GCC national oil companies increasingly deploying flexible pipe in offshore gas field developments and subsea processing trials. Africa's deepwater frontier basins in Mozambique, Senegal, and Namibia are at early stages of production infrastructure development, positioning the region for above-average growth in the latter half of the forecast period.