Fully Insured Plans: The Dominant Segment in the Group Health Insurance Market

Within the Group Health Insurance Market, plan type is the primary segmentation axis, and among the available structures — fully insured plans, self-insured plans, and mixed-insured plans — the fully insured plan segment commands the largest revenue share globally. This dominance is especially pronounced in small and medium enterprise (SME) cohorts and in emerging markets where employers lack the capital reserves and actuarial sophistication necessary to bear direct claims risk.

Under a fully insured arrangement, the employer pays a fixed periodic premium to an insurance carrier, which in turn assumes full financial responsibility for employee health claims. The carrier manages all administrative, actuarial, and claims functions, effectively transferring risk away from the employer's balance sheet. This structural simplicity is the primary reason for its widespread adoption: HR and finance teams in SMEs prefer predictable, budget-able premium outflows over the volatile claims exposure inherent in self-funded models.

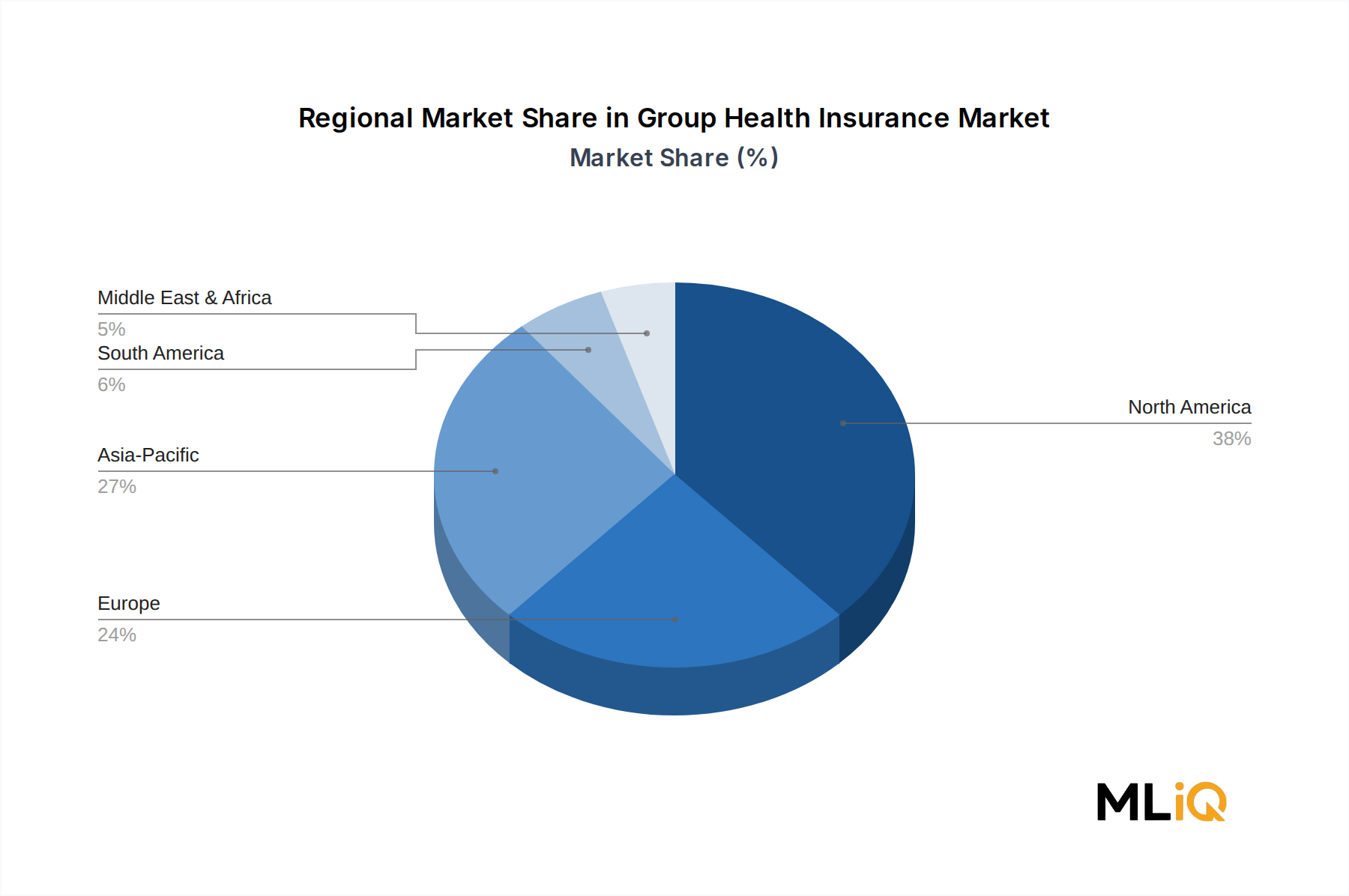

In North America, fully insured plans remain dominant among companies with fewer than 200 employees. According to industry aggregates, approximately 60–65% of businesses with under 50 employees rely on fully insured group health products, compared to roughly 20% for companies with more than 5,000 employees, where self-insured structures become economically advantageous. This size-dependent preference creates a natural segmentation dynamic that insurers are increasingly exploiting through tiered product portfolios.

In emerging markets — including India, Southeast Asia, and Sub-Saharan Africa — fully insured plans dominate due to regulatory frameworks that require licensed insurers to bear underwriting risk. In India, for instance, the Insurance Regulatory and Development Authority (IRDAI) mandates that group health policies be issued by registered general insurers, effectively precluding employer self-funding at scale. This regulatory architecture ensures that the fully insured model remains the structurally enforced default for the high-growth Asia Pacific and Middle East & Africa regions.

Key players anchoring this segment include United HealthCare Services, Inc., Cigna, Aetna Inc., Anthem Insurance Companies, Inc., and AXA. These carriers leverage vast provider networks, sophisticated actuarial models, and increasingly, AI-powered wellness programs to differentiate their fully insured group offerings. Allianz Care has carved a distinct niche in the multinational employer segment, offering globally portable fully insured group plans that serve corporations with geographically distributed workforces.

The fully insured segment's share, while dominant, faces mild structural compression in North America and Western Europe as mid-market employers migrate toward level-funded hybrid structures that combine elements of self-insurance with stop-loss reinsurance. This shift is catalyzed by greater employer awareness, the democratization of actuarial analytics tools, and the cost savings achievable when claims experience is favorable. The Health Reinsurance Market is expanding in response, with stop-loss carriers offering increasingly granular attachment-point customization to support this migration.

Nevertheless, in absolute revenue terms, the fully insured segment continues to grow robustly — driven by new-to-market SMEs in developing economies, regulatory mandates in high-growth geographies, and the inherent risk aversion of smaller employer groups. Insurers are responding by developing digital-first, modular fully insured products that allow SME employers to select benefit tiers, customize deductibles, and add ancillary riders such as dental and mental health coverage, thereby increasing average premium per policy and improving carrier revenue density.