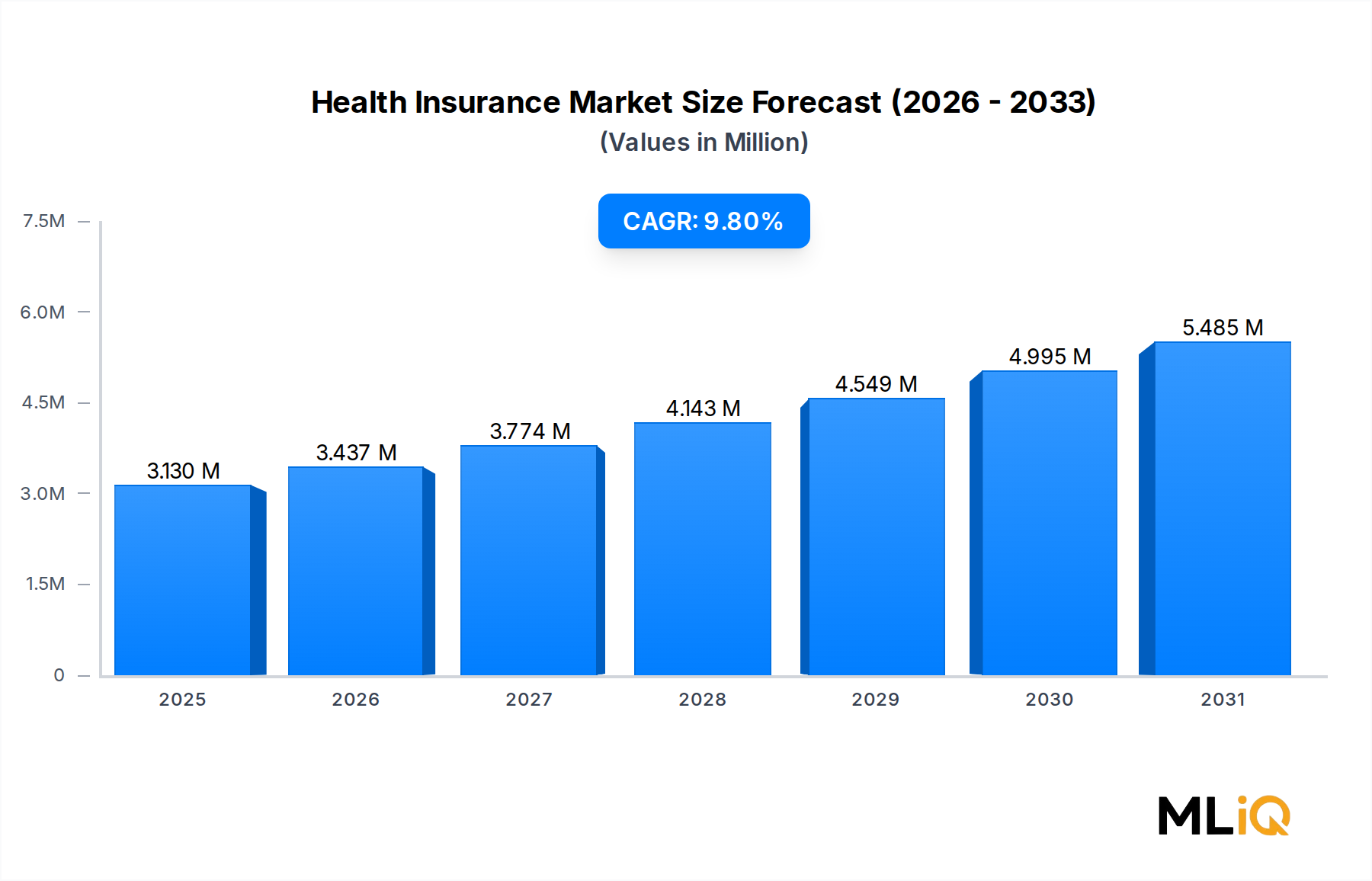

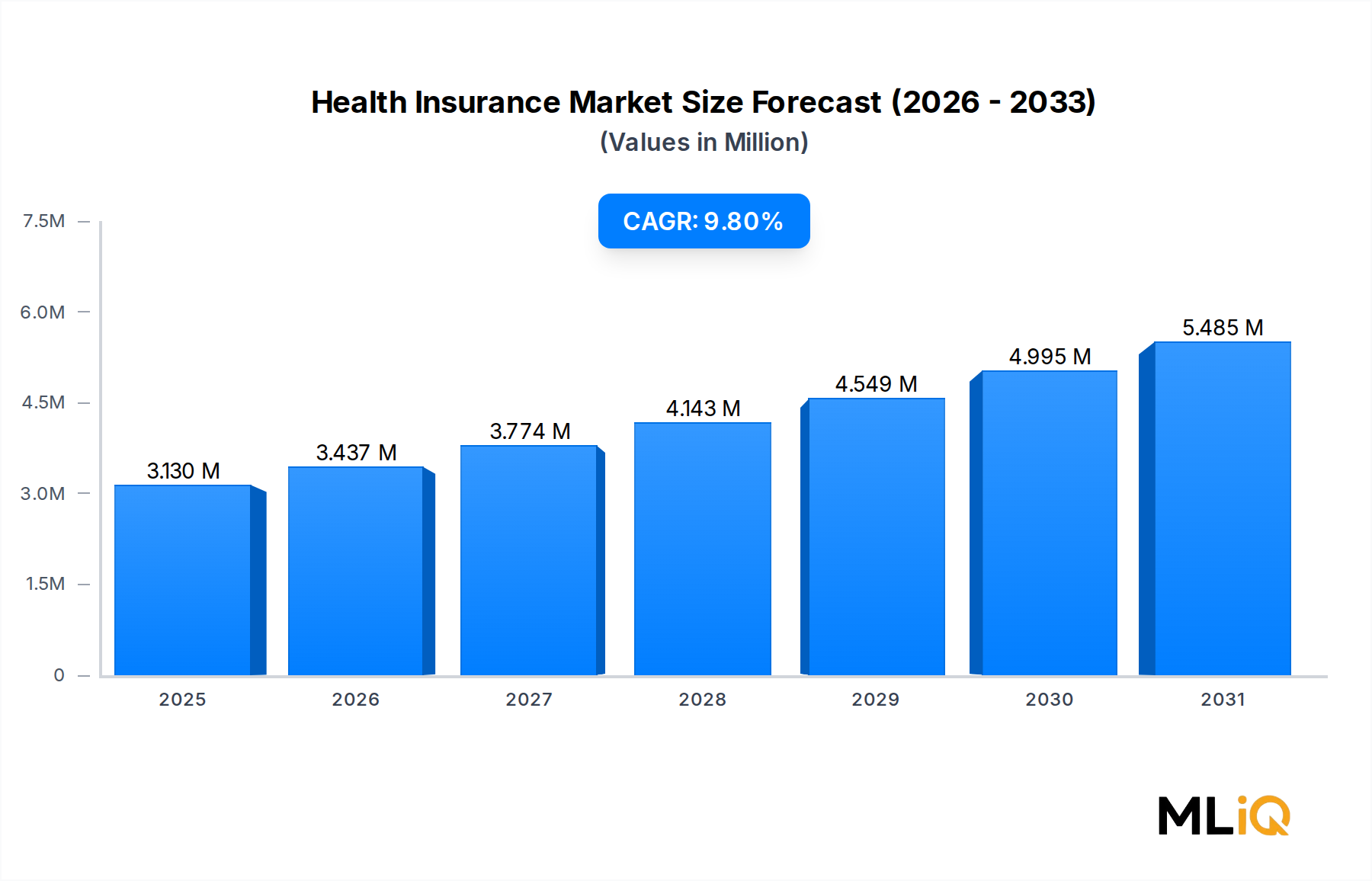

The Health Insurance Market is shaped by a well-defined set of quantifiable drivers and structural constraints that collectively determine the pace and quality of its 9.8% CAGR trajectory through 2033.

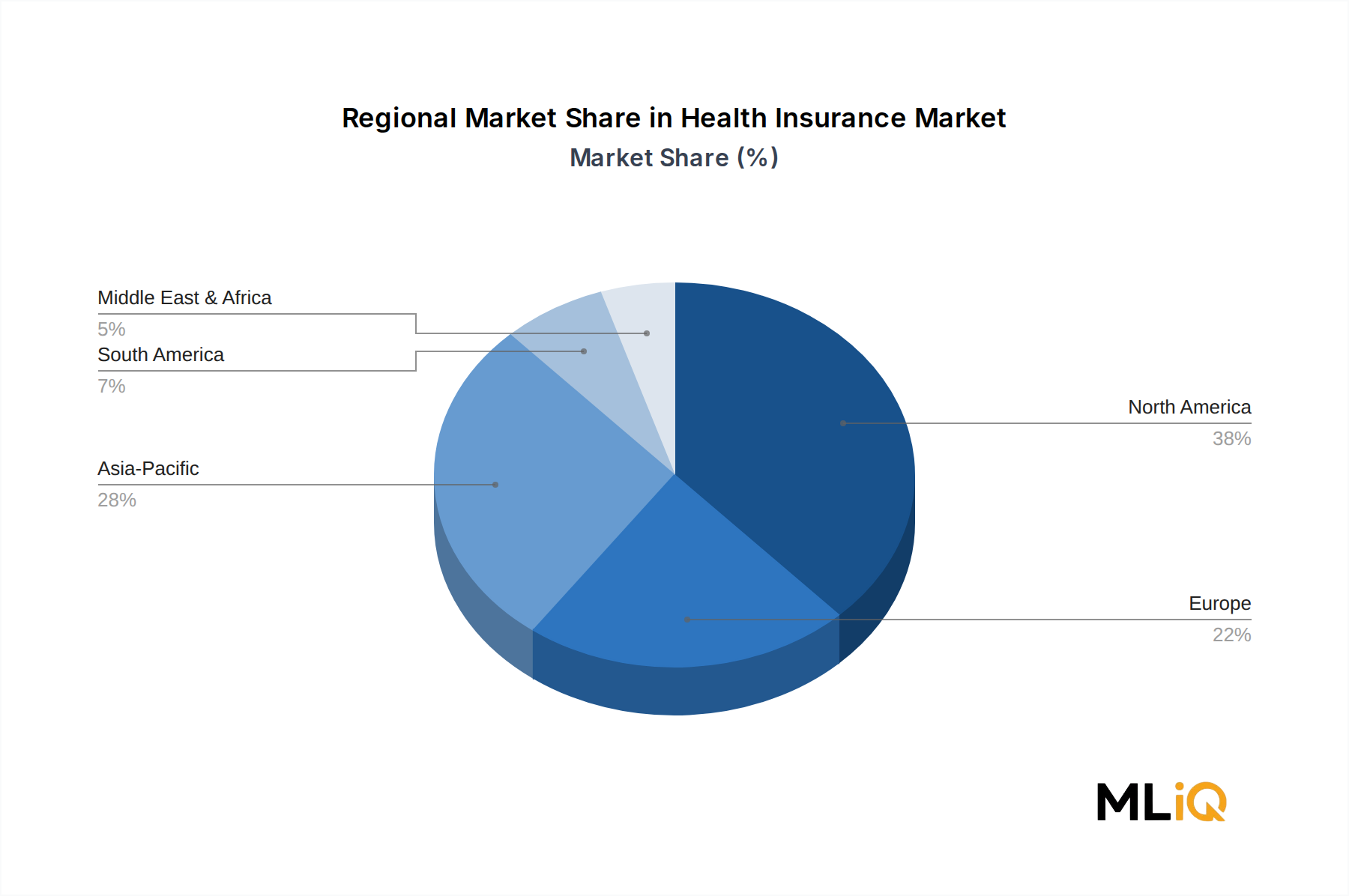

Driver 1 — Demographic Expansion of High-Risk Cohorts: The global population aged 65 and above is projected to reach 1.6 billion by 2050, according to United Nations demographic data, with near-term inflections already visible in premium volume trends. Senior citizens represent the highest per-capita healthcare utilization cohort, driving systematic increases in actuarial risk pools and compelling insurers to develop age-banded product tiers. This demographic tailwind is particularly acute in Japan, South Korea, Germany, Italy, and the United States.

Driver 2 — Regulatory Mandate Expansion: Government-enforced insurance coverage requirements are a primary volume catalyst. The U.S. Affordable Care Act's individual mandate legacy, India's Ayushman Bharat program targeting 500 million beneficiaries, and Saudi Arabia's compulsory employer health coverage regime collectively represent billions of mandated enrollment events that are expanding the premium base and reducing adverse selection risk in national risk pools.

Driver 3 — Rising Healthcare Cost Inflation: Global healthcare cost inflation averaged 8–10% annually in recent years, materially increasing both the necessity of insurance coverage and the premium rates carriers can justify to maintain adequate reserves. Medical cost trend rates in the United States have consistently outpaced general CPI by a factor of 1.5–2x, creating sustained premium pricing power for established carriers.

Constraint 1 — Affordability Gap in Emerging Markets: Despite structural demand growth, a significant affordability constraint limits penetration in lower-income demographics. In markets such as Sub-Saharan Africa and South and Southeast Asia, out-of-pocket health expenditure remains the dominant payment mechanism because formal insurance premiums exceed disposable income thresholds for the informal workforce segment.

Constraint 2 — Regulatory Complexity and Compliance Cost: Operating across multiple jurisdictions exposes global insurers to fragmented regulatory regimes, creating compliance cost burdens that compress operating margins. The heterogeneity of benefit mandates, reserve requirements, and data privacy standards across markets such as the European Union, China, and the United States increases the cost of product development and distribution, slowing market entry and innovation cycles.

Constraint 3 — Elevated Medical Loss Ratios Post-Pandemic: Deferred care patterns during the COVID-19 pandemic resulted in a surge of high-acuity claims utilization in 2022–2023, pressuring medical loss ratios at major carriers and reducing underwriting profitability, which in some markets triggered premium increases that accelerated coverage lapses among price-sensitive policyholders.