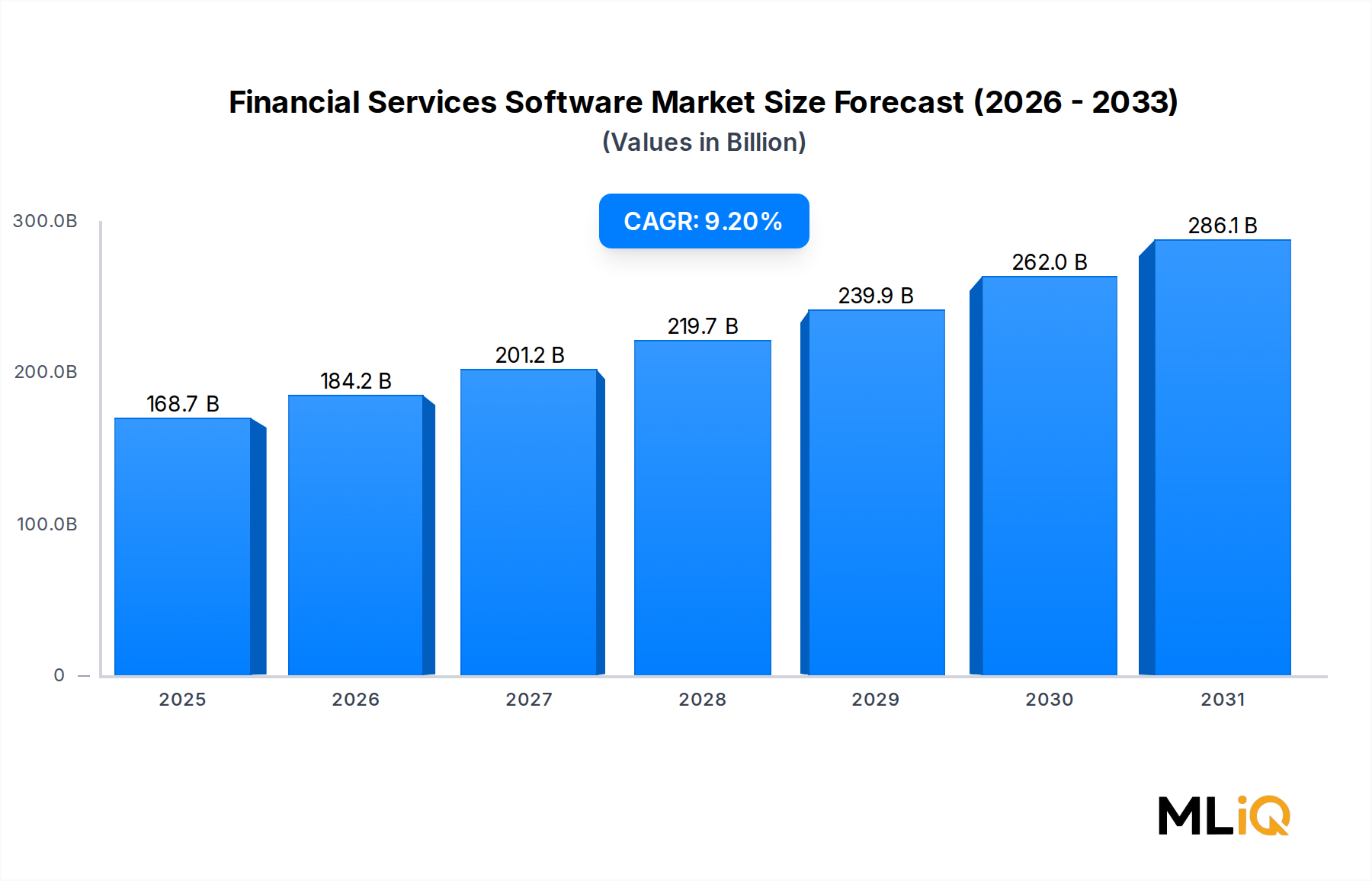

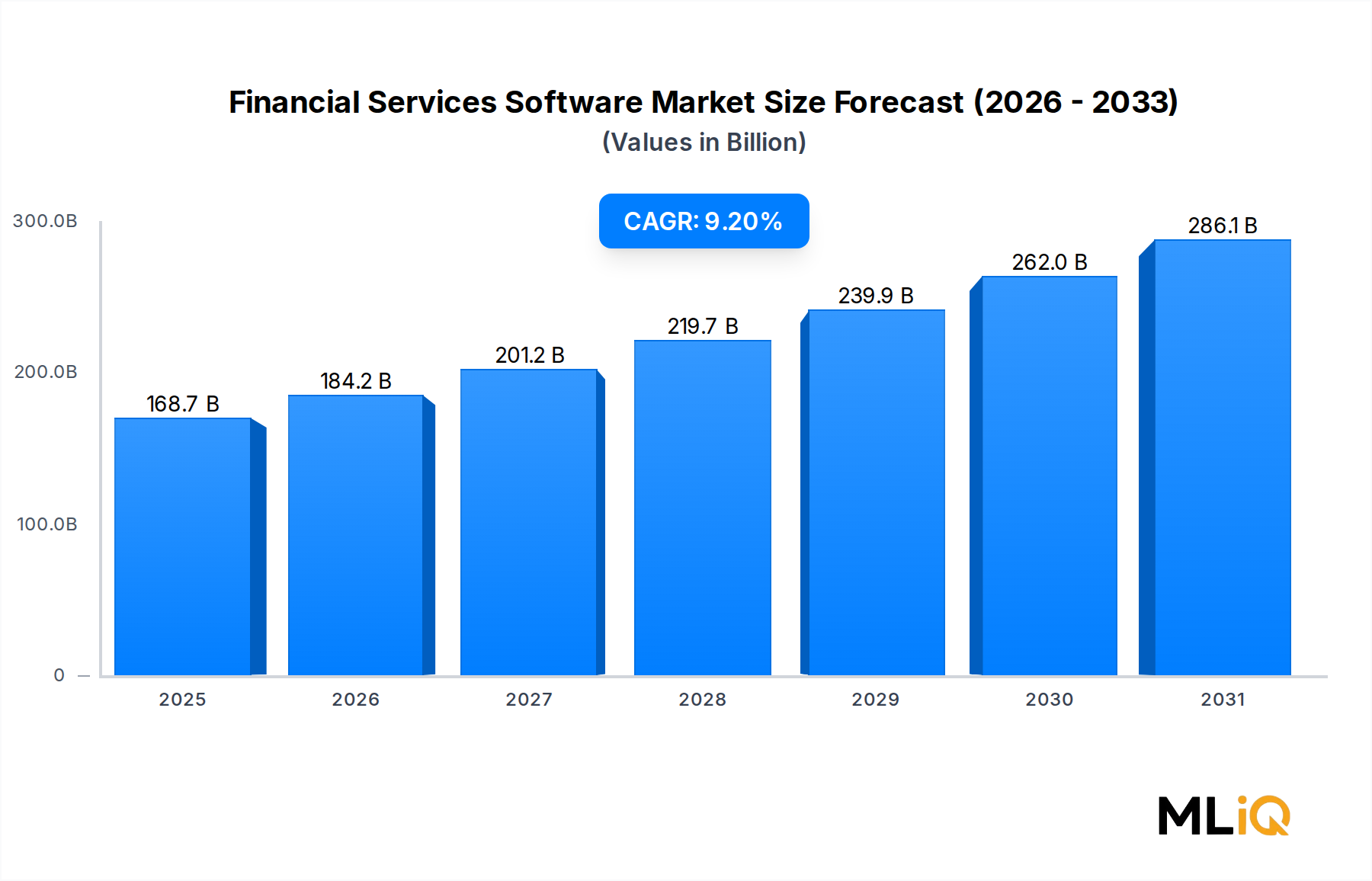

The Financial Services Software Market is positioned at a decisive inflection point, combining robust structural demand with accelerating digital transformation across banking, insurance, and capital markets. The market was valued at $168.72 billion in the base assessment year and is projected to expand at a compound annual growth rate (CAGR) of 9.2% through 2033, reflecting the deepening integration of software platforms into core financial operations globally.

Several macro-level tailwinds are catalyzing this expansion. First, the wholesale migration of legacy on-premise systems toward cloud-native architectures has compressed deployment cycles while delivering measurable cost savings, prompting institutions of all sizes to accelerate technology refresh cycles. Second, regulatory complexity — amplified by frameworks such as Basel IV, DORA in Europe, and evolving anti-money-laundering mandates — is driving sustained investment in compliance automation and audit management tools. Third, the proliferation of real-time payments, open banking APIs, and embedded finance has created structural demand for high-throughput transaction processing engines.

On the demand side, large enterprises continue to dominate spending, accounting for the majority of software procurement, yet small and medium-sized financial institutions are registering the fastest adoption rates as vendor pricing models evolve toward consumption-based and SaaS structures. The enterprise IT sub-segment and business transaction processing tools are capturing disproportionate investment as organizations seek unified platforms that reduce vendor sprawl.

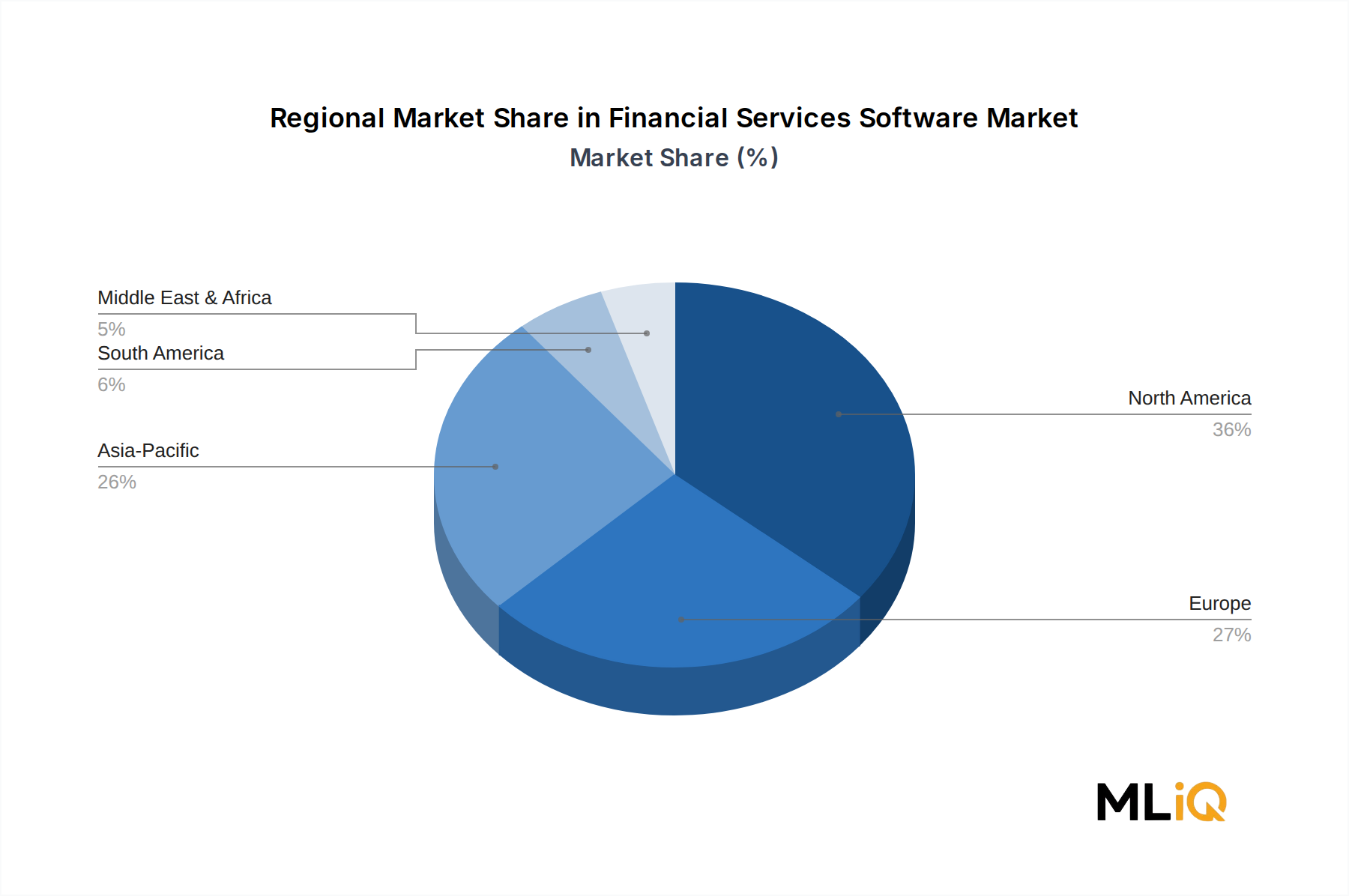

Geographically, North America retains its position as the single largest revenue contributor, underpinned by concentrated banking sector density and early cloud adoption. Asia Pacific, however, is emerging as the highest-growth region, driven by fintech ecosystem expansion in China, India, and Southeast Asian markets. Europe's regulatory modernization agenda is sustaining steady demand even against a backdrop of macroeconomic uncertainty.

Key demand drivers include the rise of artificial intelligence-powered analytics, the need for real-time risk surveillance capabilities, and the increasing consumerization of enterprise financial tools. Restraints center on data sovereignty concerns, integration complexity with decades-old core banking systems, and talent scarcity in specialized financial technology domains.

Looking ahead to 2033, the market is expected to reach a substantially elevated valuation as generative AI becomes embedded into risk, compliance, and customer experience workflows. Vendors that can deliver modular, interoperable platforms will capture outsized share as financial institutions increasingly favor composable architectures over monolithic solutions. The competitive landscape will reward those offering pre-built regulatory content libraries, API-first designs, and measurable return-on-investment metrics tied to operational efficiency.