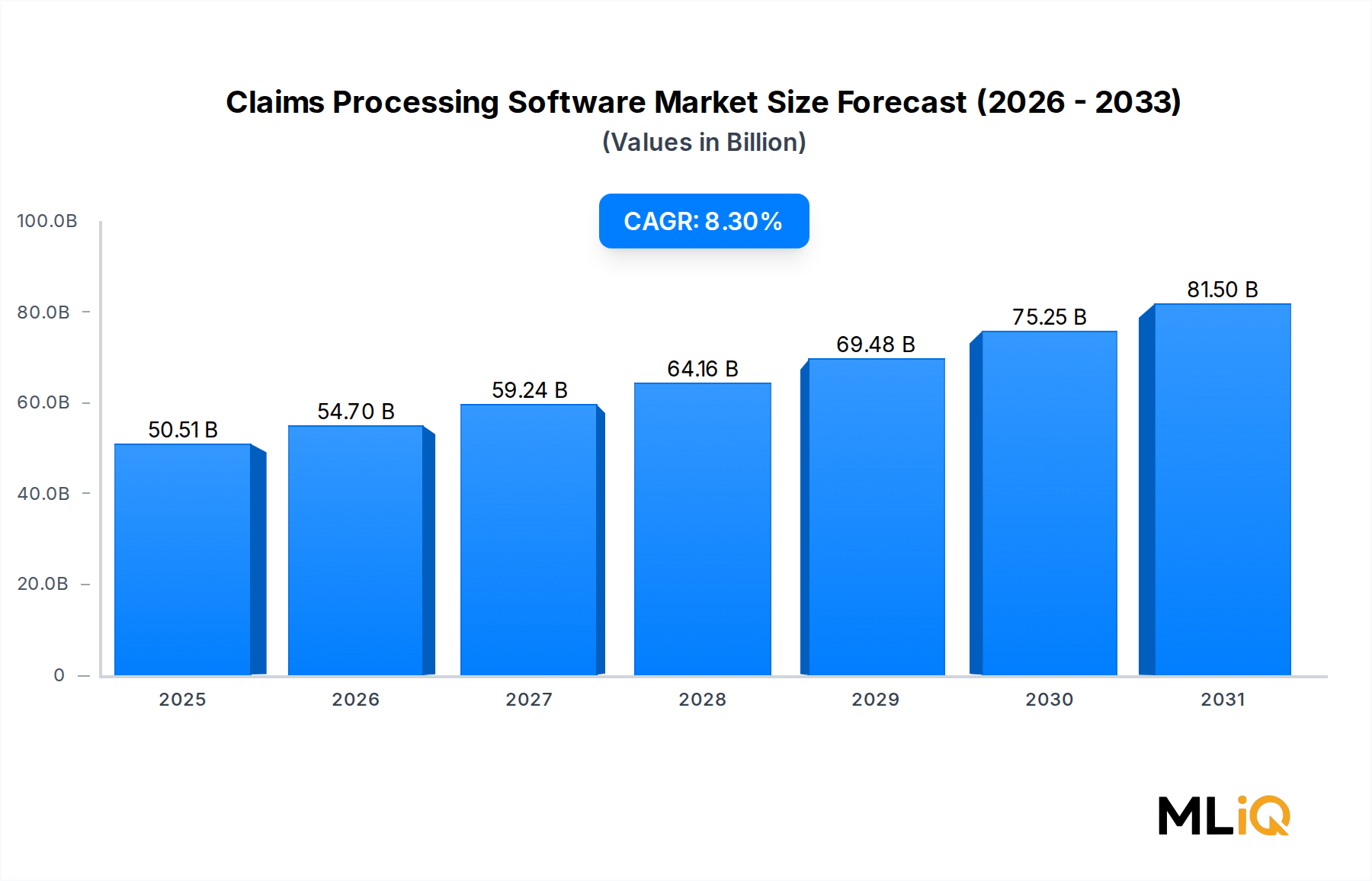

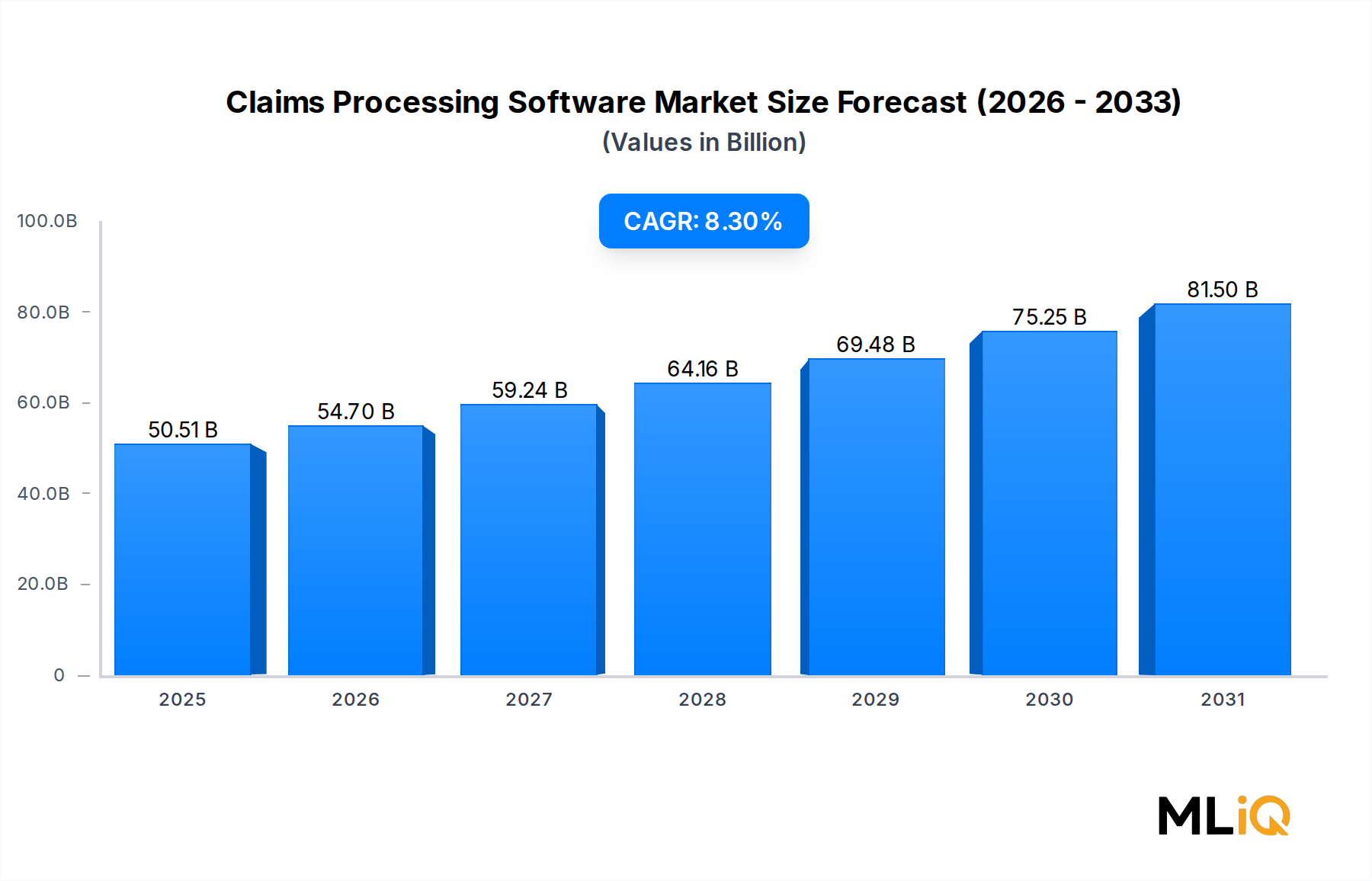

Software Component Dominance in the Claims Processing Software Market

Within the component segmentation of the Claims Processing Software Market, the software sub-segment commands the dominant revenue share, consistently accounting for an estimated 72–75% of total market value. This dominance reflects the capital-intensive nature of platform licensing, the multi-year subscription commitments that enterprise insurers enter with core system vendors, and the high switching costs that entrench established software relationships once integration with policy administration, billing, and actuarial systems is complete.

The software segment encompasses several functional layers: first notice of loss (FNOL) capture modules, automated adjudication engines, fraud detection and analytics dashboards, payment disbursement orchestration, and regulatory reporting suites. Each layer contributes recurring revenue through annual maintenance fees, cloud subscription tiers, and consumption-based pricing models increasingly adopted by mid-market insurers who prefer variable cost structures aligned to claim volume fluctuations.

Large enterprises represent the highest absolute revenue contributor within the software segment. Carriers with annual written premiums exceeding $1 billion typically deploy enterprise-grade platforms with multi-line, multi-jurisdiction capabilities, requiring deep customization, robust API ecosystems, and carrier-grade SLAs. These deployments generate average contract values (ACVs) in the range of $2 million to $15 million depending on claim volume thresholds and functional scope, making them among the most financially significant software procurement decisions in the BFSI sector.

Small and medium-sized enterprises (SMEs), while individually lower in contract value, collectively represent a fast-growing adoption cohort. The emergence of pre-configured SaaS platforms with standardized workflows, embedded compliance libraries, and low-code configuration interfaces has dramatically reduced the implementation barrier for regional carriers, managing general agents (MGAs), and specialty line insurers. Vendors such as Duck Creek Technologies and HawkSoft have specifically engineered SME-oriented product tiers that allow accelerated onboarding within 90 to 180 days, compared to the 12 to 24-month implementation cycles associated with large-enterprise deployments.

The services sub-segment — encompassing implementation, integration, training, and managed services — accounts for the remaining 25–28% of market revenue. While smaller in absolute terms, the services segment carries strategic importance as a retention mechanism; insurers that rely on vendor-delivered managed services for ongoing system operations exhibit significantly lower churn rates than self-managed deployments. The growing complexity of integrating claims platforms with telematics feeds, IoT sensor networks, and third-party data providers is sustaining demand for specialized integration services, particularly as carriers expand into usage-based insurance (UBI) and parametric product lines.

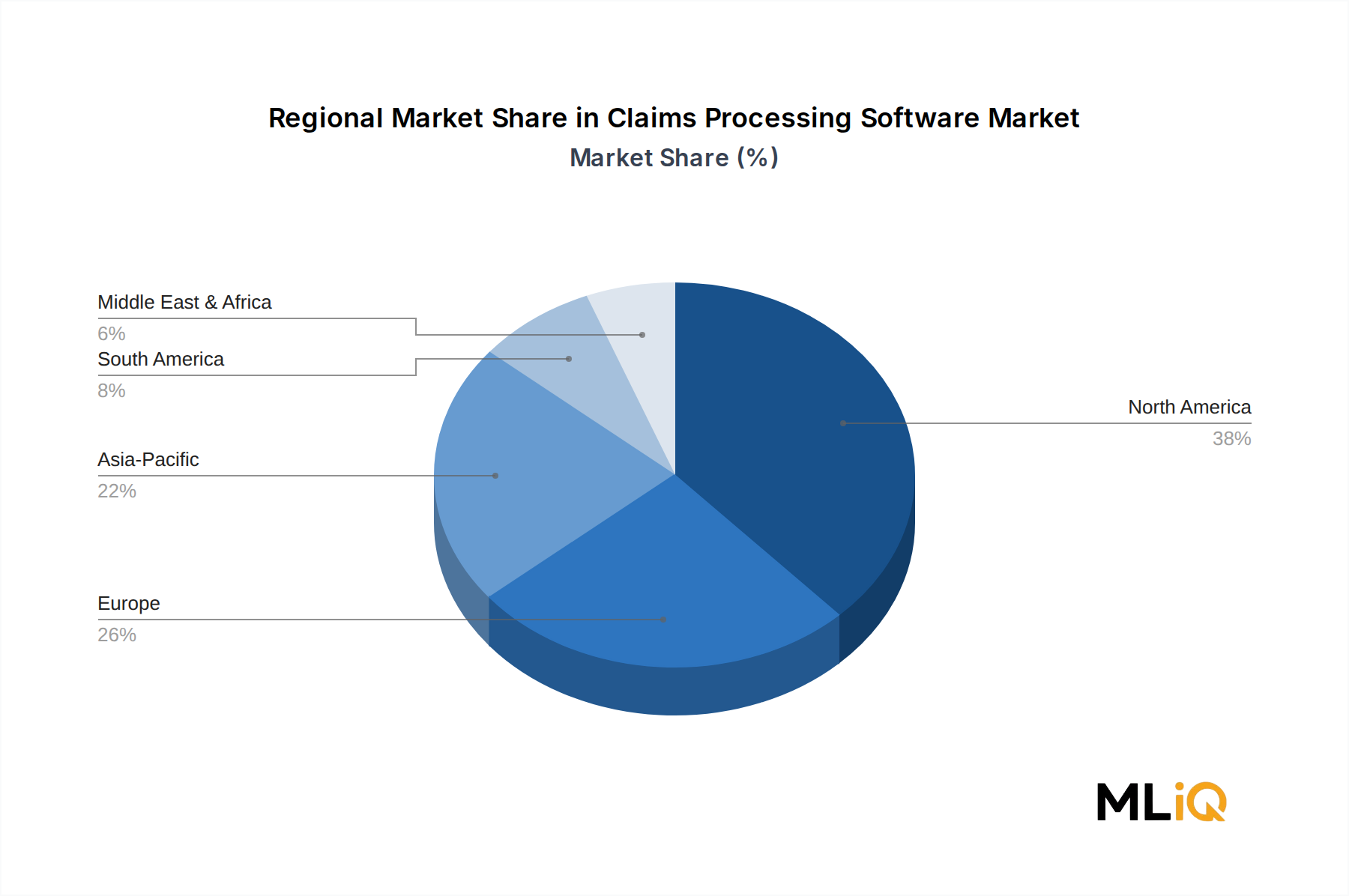

Key players anchoring the software segment include Pegasystems Inc., which leverages its AI-decisioning platform for automated claims routing and real-time fraud scoring; Duck Creek Technologies, whose cloud-native P&C suite is adopted by more than 30 of the top 100 global P&C carriers; FINEOS, which dominates the life, accident, and health claims administration segment particularly in North American and Australian markets; and Newgen Software Technologies Limited, which has expanded its low-code claims automation platform across Asian and Middle Eastern insurance markets with notable traction in government health insurance programs.

The software segment's share is not merely holding steady — it is consolidating. The rapid depreciation of on-premise infrastructure investments, combined with vendor-driven cloud migration incentive programs offering preferential pricing for multi-year SaaS commitments, is accelerating the conversion of legacy software licensees to subscription-based cloud tenants. This structural shift is expanding the addressable recurring revenue base while compressing one-time perpetual license revenues, fundamentally reshaping vendor income statement profiles toward higher-margin, more predictable annual recurring revenue (ARR) models.