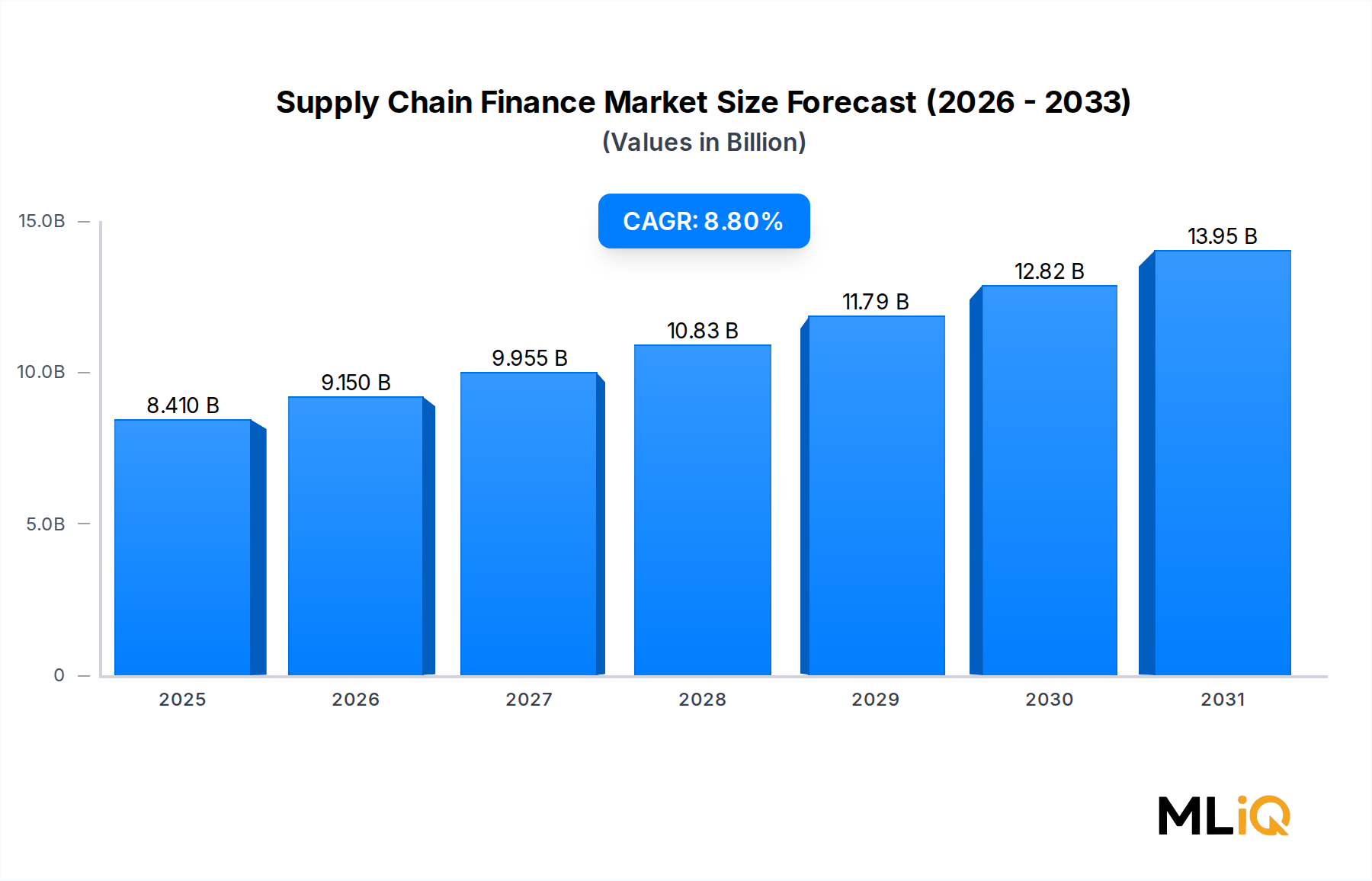

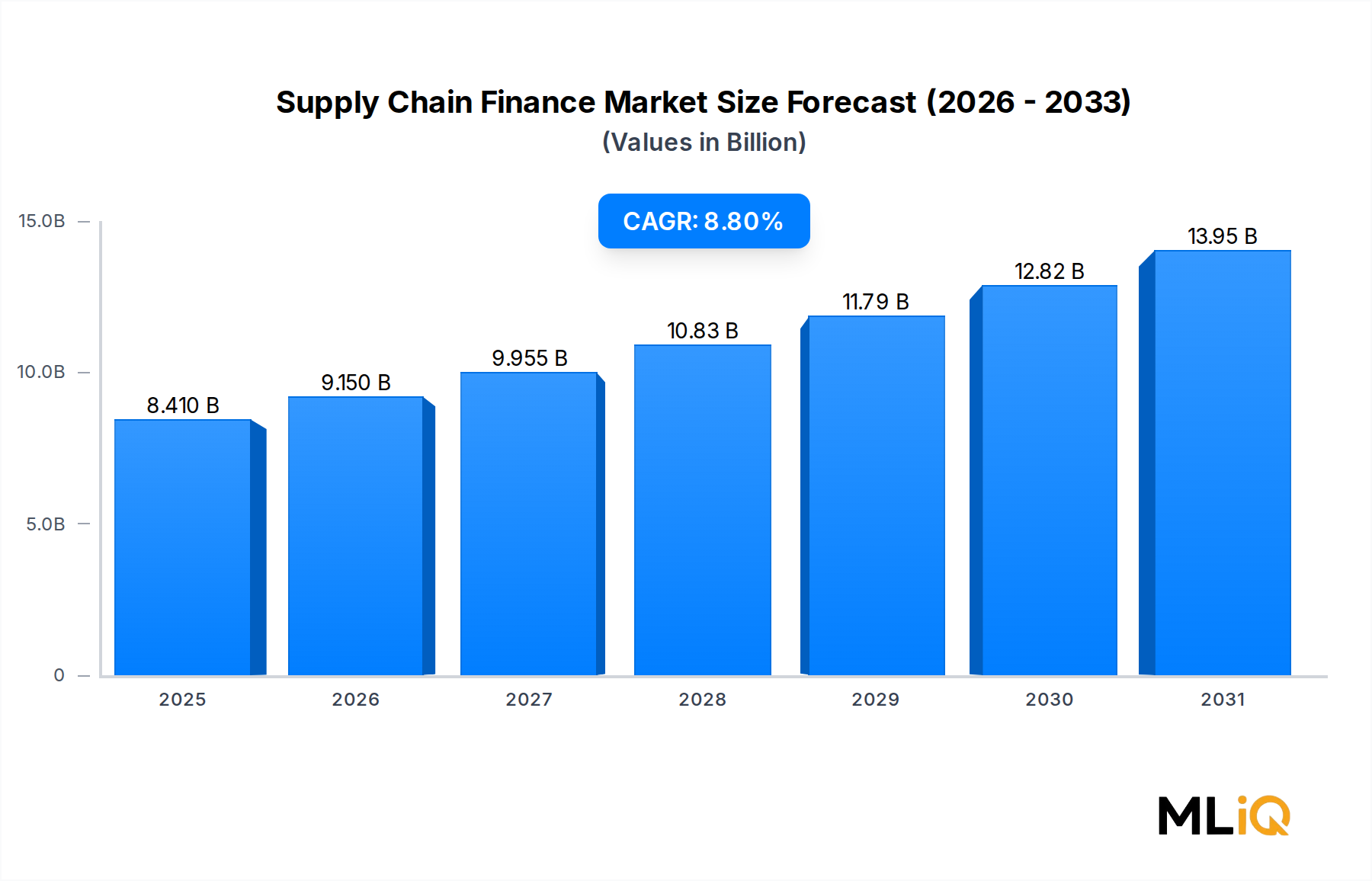

The global Supply Chain Finance Market was valued at $8.41 billion in the base year and is projected to expand at a compound annual growth rate (CAGR) of 8.8% through 2033, reflecting a robust structural shift in how enterprises manage liquidity across multi-tier supplier networks. This market sits at the intersection of financial services innovation, digital transformation, and evolving global trade dynamics, creating a fertile environment for sustained investment and product diversification.

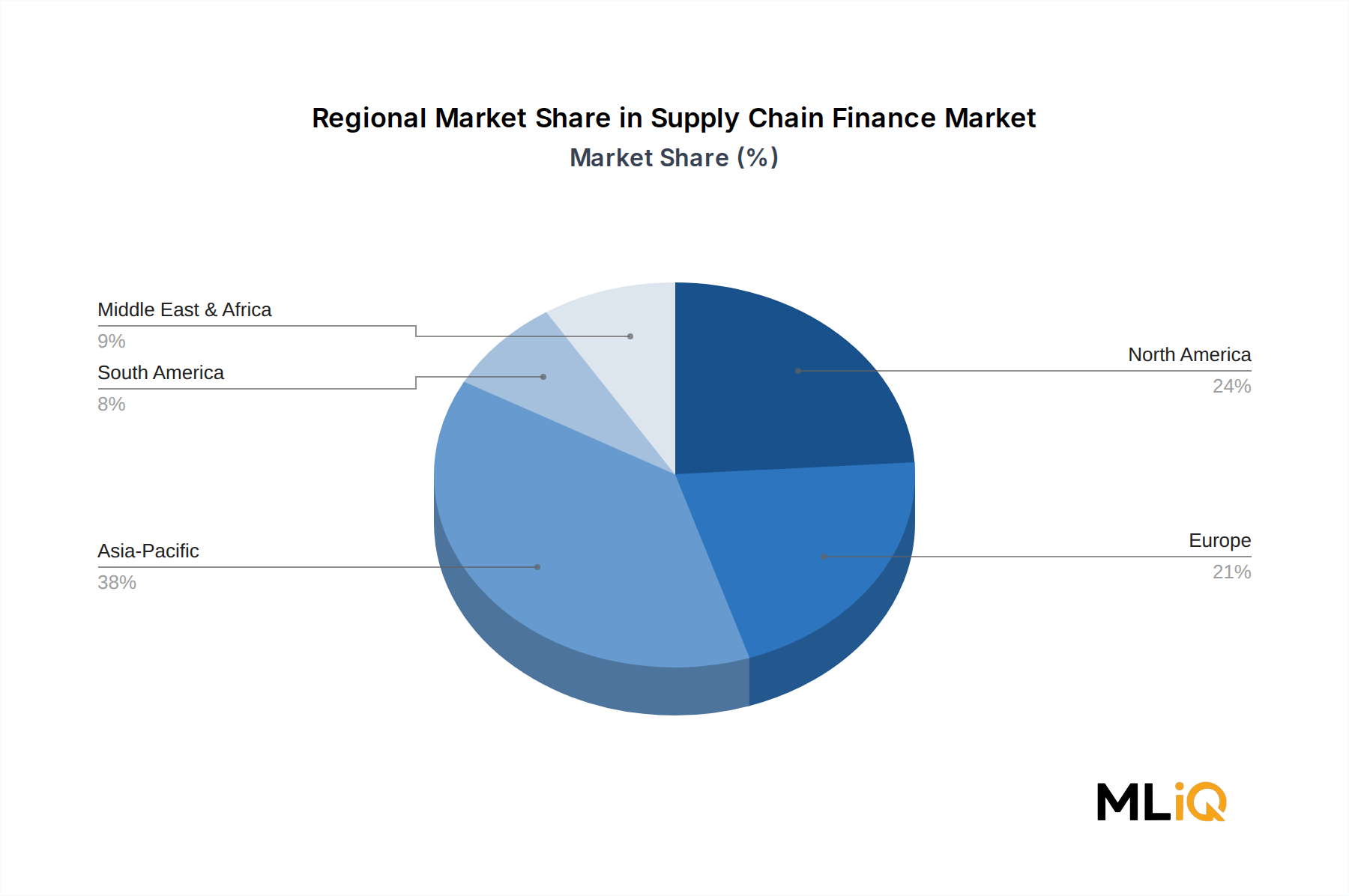

Demand for supply chain finance solutions is being propelled by several converging macro tailwinds. First, increasing global trade volumes — particularly in Asia Pacific and North America — are stretching the working capital cycles of both large buyers and small-to-medium suppliers, creating urgent demand for instruments such as reverse factoring, dynamic discounting, and receivables purchase programs. Second, the post-pandemic recalibration of global supply chains has heightened corporate awareness of supplier financial health as a systemic risk, prompting procurement and treasury functions to collaborate more closely than ever before. Third, the accelerating digitization of trade documentation — including electronic invoicing, e-bills of lading, and digital letters of credit — is substantially reducing the friction costs historically associated with trade finance instruments, enabling faster onboarding and higher transaction volumes.

Key demand drivers also include regulatory developments such as Basel III liquidity requirements, which incentivize banks to originate supply chain finance assets that carry favorable risk-weighting profiles. Furthermore, the proliferation of embedded finance platforms, application programming interfaces (APIs), and cloud-native treasury management systems has lowered the technological barrier for mid-market enterprises to access solutions previously available only to large multinationals.

From a sectoral perspective, the market is witnessing significant traction in industries with long payment cycles, including automotive, retail, consumer packaged goods, and healthcare. The rise of environmental, social, and governance (ESG) — linked supply chain finance programs, where financing costs are tied to suppliers' sustainability performance metrics, is emerging as a notable growth catalyst, blending capital efficiency with responsible sourcing objectives.

Looking ahead to 2033, the Supply Chain Finance Market is expected to be characterized by deeper platform consolidation, the normalization of artificial intelligence-driven risk scoring for supplier creditworthiness, and the integration of central bank digital currencies (CBDCs) into cross-border settlement mechanisms. Collectively, these developments position the market for compounding value creation well beyond its current trajectory.