Pure Robo Advisors as the Dominant Segment in the Robo Advisory Market

Within the Robo Advisory Market's segmentation by business model, Pure Robo Advisors represent the single largest revenue-generating category and continue to define the technological and commercial frontier of the sector. Unlike their hybrid counterparts — which blend algorithmic tools with human financial advisor touchpoints — Pure Robo Advisors rely entirely on automated, algorithm-driven processes for portfolio construction, rebalancing, risk profiling, and client communication. This full-stack automation model translates directly into superior operating leverage and the ability to serve mass-market retail investors at cost structures that were previously economically unviable.

The dominance of Pure Robo Advisors is rooted in several structural advantages. First, the elimination of human advisory overhead allows platforms to offer AUM-based fees averaging 0.25–0.35% annually, compared to 0.65–0.90% typical of hybrid models. This fee differential is a decisive acquisition lever in price-sensitive retail investor segments where even modest fee reductions compound into materially superior long-term net returns.

Second, Pure Robo Advisors benefit from scalability that is architecturally unconstrained. A traditional wealth advisor can service approximately 150–200 client relationships simultaneously; an automated platform can manage millions of accounts on a single infrastructure stack. This scalability advantage compounds over time as platforms accumulate behavioral and financial data to continuously refine their algorithmic models.

Betterment stands as the archetype of the Pure Robo Advisor model, having pioneered the category in the United States and maintaining one of the largest independent AUM bases in the segment. Wealthfront Corporation has similarly carved out a leadership position through an aggressive product expansion strategy that now encompasses high-yield cash accounts, direct indexing, and self-driving money automation — all delivered without human advisor intermediation.

The fintech robo advisor sub-category, which predominantly houses Pure Robo Advisors, is attracting disproportionate venture and strategic capital relative to bank-owned hybrid platforms. This investment asymmetry reflects institutional recognition that the full-automation model is the more scalable and defensible long-term architecture, particularly as AI capabilities continue to advance.

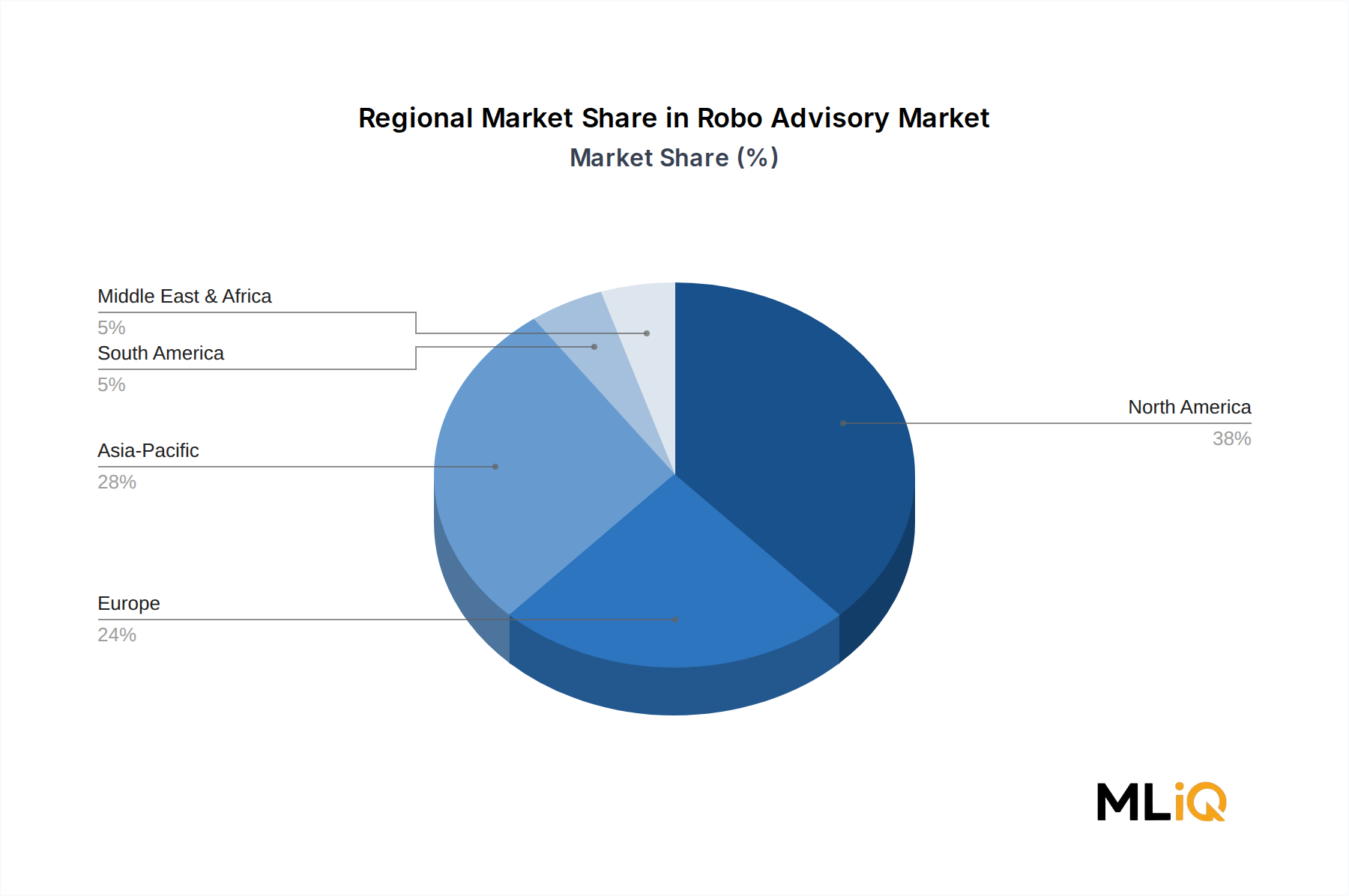

Geographically, Pure Robo Advisors command the highest market penetration in North America, where early regulatory clarity, high smartphone penetration, and a culturally embedded DIY investing ethos have created ideal adoption conditions. However, European platforms such as Ginmon Vermögensverwaltung GmbH and Wealthify Limited are rapidly closing the penetration gap, supported by MiFID II's transparency requirements that structurally favor low-fee automated models over opaque traditional advisory products.

The High Net Worth Individuals (HNIs) segment is also beginning to show meaningful traction with Pure Robo Advisors, historically a surprising development given this cohort's traditional preference for bespoke human advisory relationships. The catalyst is the emergence of sophisticated direct indexing tools — previously accessible only to ultra-HNW clients — being democratized through automated platforms at significantly reduced minimum investment thresholds.

Looking at market share trajectory, the Pure Robo Advisor segment is consolidating around a small number of well-capitalized platforms, suggesting that network effects and data moats are beginning to create durable competitive barriers. Smaller pure-play entrants without differentiated technology or distribution partnerships face increasing pressure to pivot toward niche vertical markets or accept acquisition as a primary exit pathway.

Overall, the Pure Robo Advisor segment's combination of fee competitiveness, unlimited scalability, and technological sophistication positions it to maintain its dominant share across the forecast period, even as hybrid models gain traction in segments where investor confidence in full automation remains nascent.