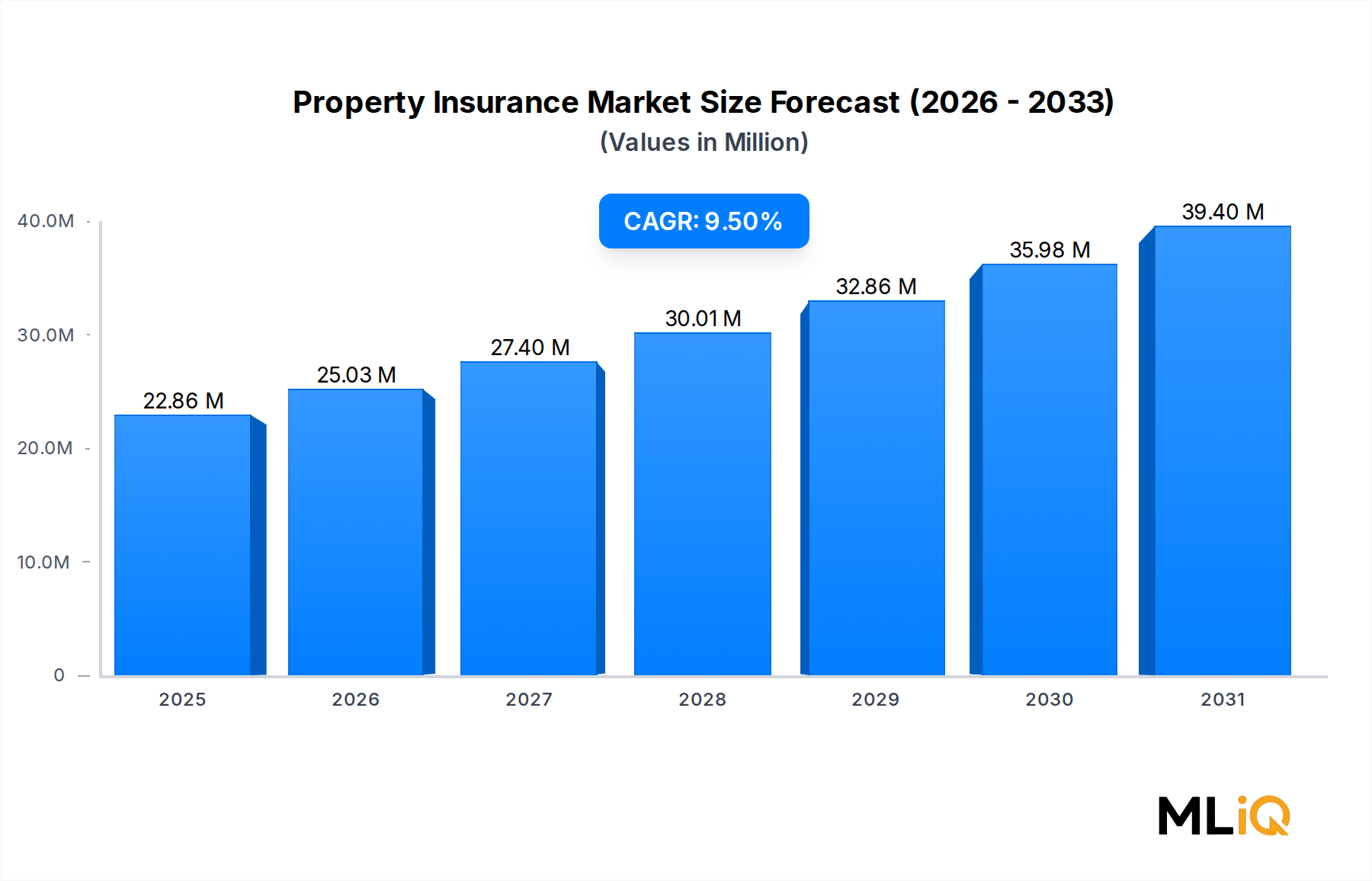

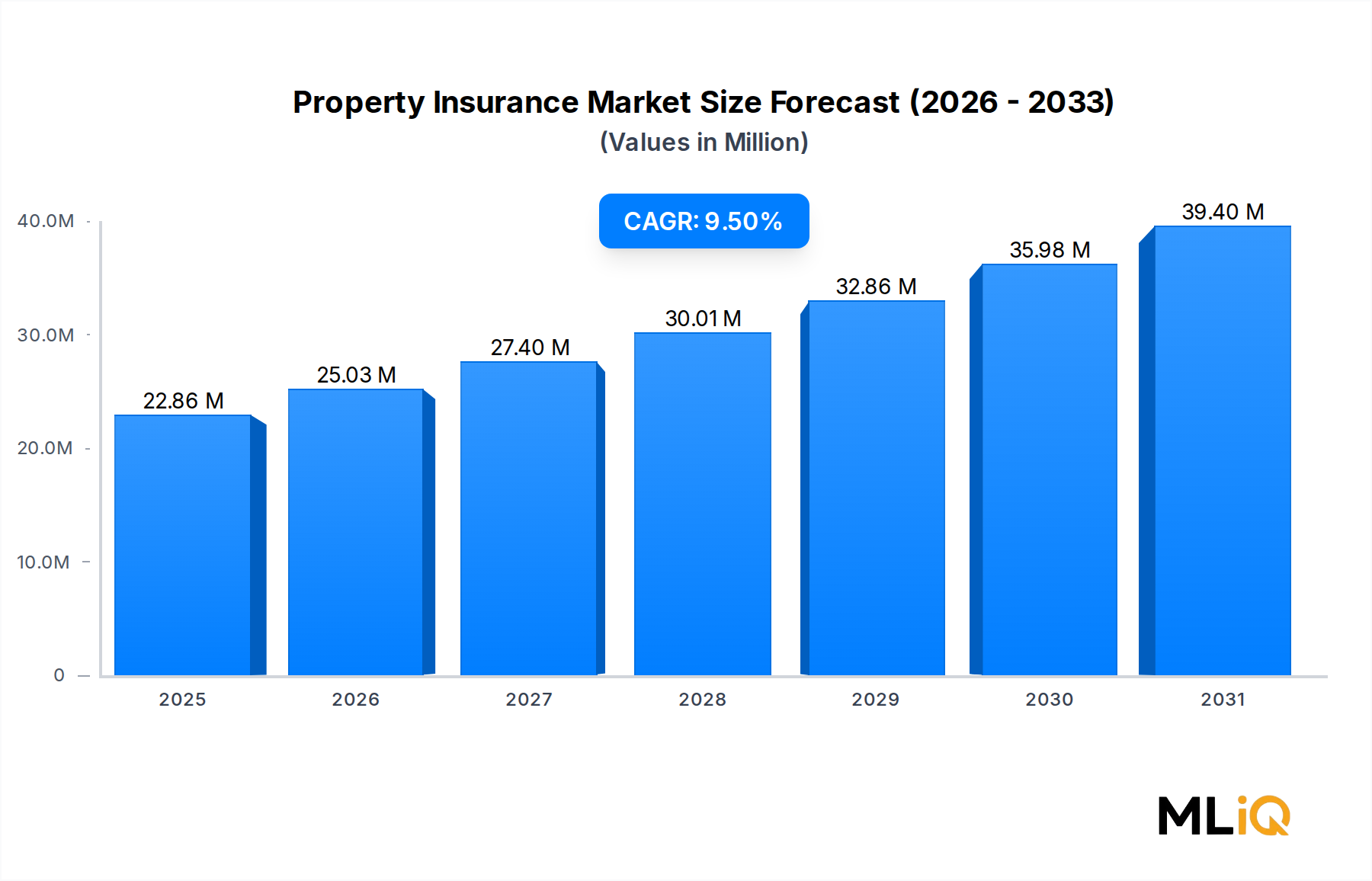

Dominance of the Homeowners Segment in the Property Insurance Market

Among all end-user segments, homeowners constitute the single largest revenue contributor within the Property Insurance Market, accounting for the majority of personal lines premium volume globally. This dominance is rooted in several interlocking structural, regulatory, and behavioral factors that have compounded over decades.

First, the sheer scale of owner-occupied residential housing stock creates an enormous insurable base. In the United States alone, the Census Bureau estimates more than 84 million owner-occupied housing units, each representing a potential policy. Similar density is found across Western Europe and increasingly in China and India as urbanization converts renters into property owners. Mortgage lenders universally require hazard insurance as a loan condition, institutionalizing demand at the point of home purchase and ensuring policy persistence across multi-year loan tenures.

Second, homeowners policies are structurally comprehensive. Unlike single-peril products, a standard homeowners policy bundles dwelling coverage, other structures, personal property, loss of use, personal liability, and medical payments, generating significantly higher average premiums per policy than renters or standalone fire products. This premium density makes the homeowners segment disproportionately valuable to insurers relative to its unit count.

Third, rising replacement costs — driven by construction material inflation, skilled labor shortages, and increasingly stringent building codes — have pushed average insured values upward across most major markets. In the United States, dwelling replacement costs rose by approximately 40% between 2020 and 2024 according to industry reconstruction cost indices, creating corresponding premium growth even without expansion in policy count.

Key players deeply entrenched in this segment include State Farm Mutual Automobile Insurance Company, which retains the largest homeowners market share in the United States, followed closely by Allstate Insurance Company and Liberty Mutual Insurance. Internationally, Allianz and AXA dominate homeowners lines across European markets, while PICC leads in China's rapidly expanding residential insurance sector. Chubb occupies a differentiated position by targeting high-net-worth homeowners, offering guaranteed replacement cost coverage and specialized concierge claims services that command significant premium premiums over standard market rates.

The segment's market share is consolidating rather than fragmenting. Smaller regional carriers are struggling to absorb catastrophe losses without sufficient geographic diversification or reinsurance support, leading to voluntary market exits in states like California and Florida. This withdrawal is driving policyholders toward larger national and multinational carriers, reinforcing concentration at the top of the competitive hierarchy.

The Homeowners Insurance Market remains the anchor of personal lines strategy for most major carriers, and its continued expansion is closely tied to housing market activity, mortgage penetration rates, and post-disaster government mandates. As climate risk repricing accelerates, insurers are deploying predictive analytics to segment risk pools more finely, which is expected to widen the pricing gap between well-located and high-risk properties — shaping the next phase of competitive dynamics in this dominant segment.

The adjacent Renters Insurance Market, while smaller in absolute premium terms, is exhibiting faster unit growth as millennial and Gen Z cohorts delay home purchases, and as landlords increasingly require tenant coverage through lease agreements. This creates a strategic pipeline for insurers to convert future homeowners from existing renters relationships, enhancing lifetime customer value metrics.