Solution Segment Dominance in Multi-Cloud Networking in Fintech Market

Among the two primary component segments — Solution and Service — the Solution segment commands the dominant revenue share within the Multi-Cloud Networking in Fintech Market. This dominance is attributable to the capital-intensive, one-time deployment nature of networking platforms, combined with the recurring but contract-embedded software licensing models that vendors have adopted. The Solution segment encompasses cloud networking platforms, SD-WAN (Software-Defined Wide Area Networking) tools, cloud interconnect software, network policy engines, and observability dashboards tailored for multi-cloud financial environments.

The primary reason the Solution segment leads is structural: fintech firms and traditional financial institutions both require purpose-built networking layers that can abstract the complexity of operating across AWS, Azure, Google Cloud, and private data centers simultaneously. Off-the-shelf networking tools designed for single-cloud environments are insufficient for managing cross-cloud routing tables, latency SLAs, and data encryption standards simultaneously. As a result, specialized multi-cloud networking solutions command premium pricing and high switching costs, reinforcing revenue concentration in this segment.

Key players driving the Solution segment include Cisco Systems Inc., which leverages its market-leading position in enterprise networking hardware and software to deliver cloud-agnostic networking fabric. Aviatrix has positioned itself as a pure-play multi-cloud networking vendor, offering a controller-based architecture that automates routing between hyperscale clouds. VMware, Inc. provides NSX-based network virtualization that integrates with its Tanzu portfolio for container-native financial applications. Juniper Networks, Inc. contributes AI-driven networking through its Mist and Apstra platforms, which deliver intent-based networking policies suitable for regulated financial environments.

The Solution segment's share is not merely holding — it is consolidating. As fintech firms mature their cloud strategies from lift-and-shift migrations to cloud-native architectures, the complexity of their networking requirements increases nonlinearly. Each additional cloud provider added to an institution's estate multiplies the number of peering relationships, security policy permutations, and compliance checkpoints that must be managed. This complexity gradient ensures that demand for advanced Solution-tier products grows faster than demand for advisory or managed services.

A critical sub-trend within the Solution segment is the rise of Network-as-Code (NaC) frameworks, which allow financial engineering teams to define, version, and deploy networking configurations using infrastructure-as-code toolchains. This approach reduces human error in cross-cloud routing changes — a historically significant source of financial service outages — and aligns with DevSecOps mandates increasingly enforced by financial regulators in the US, EU, and UK.

Another growth vector for the Solution segment is the integration of AI and machine learning capabilities into multi-cloud networking platforms. Vendors are embedding anomaly detection, traffic prediction, and automated failover logic directly into their networking control planes. For fintech firms running high-frequency trading systems, payment gateways, or fraud detection pipelines, these capabilities translate directly into reduced latency variance and improved uptime SLAs, justifying the premium pricing commanded by advanced Solution offerings.

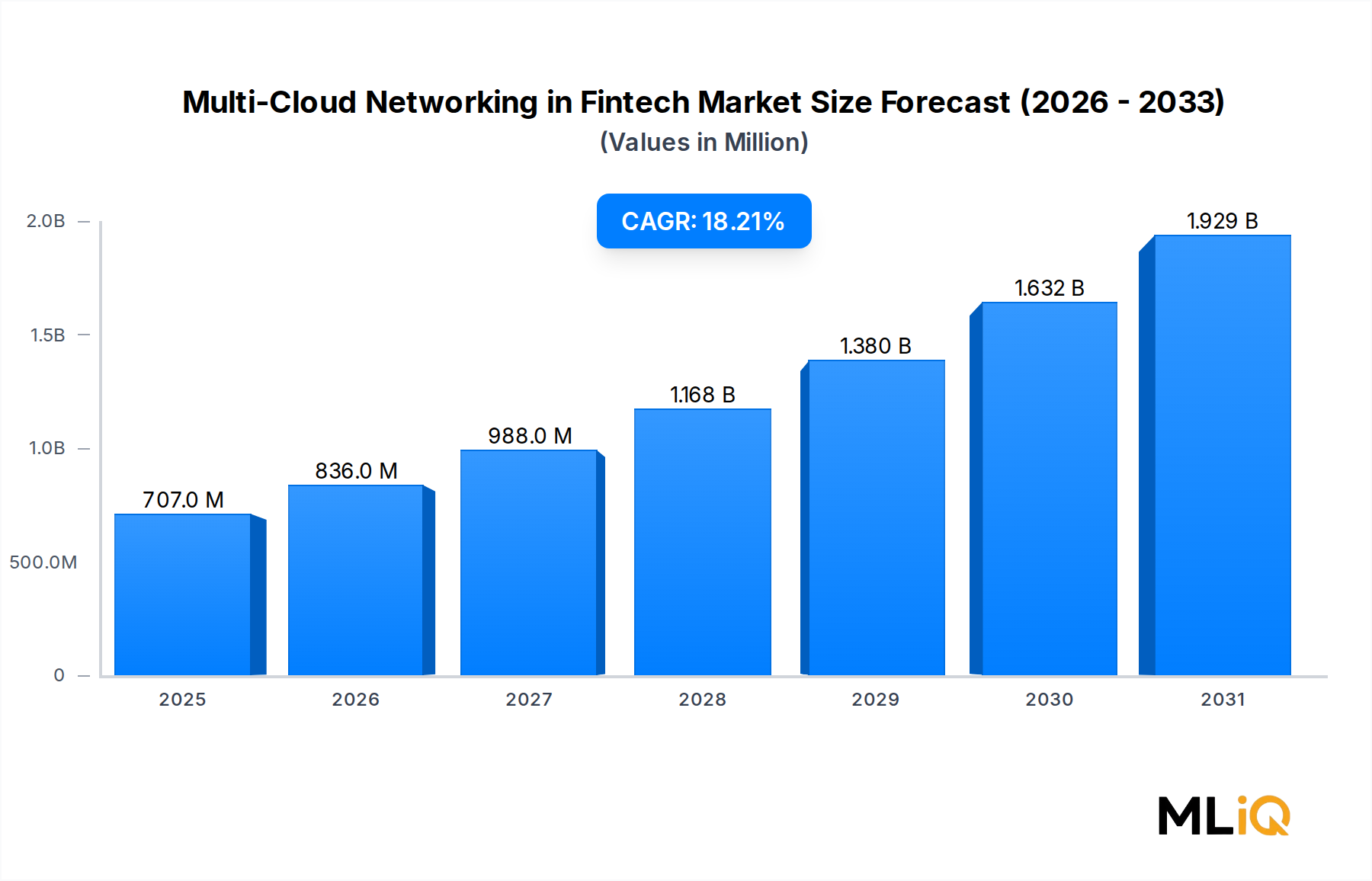

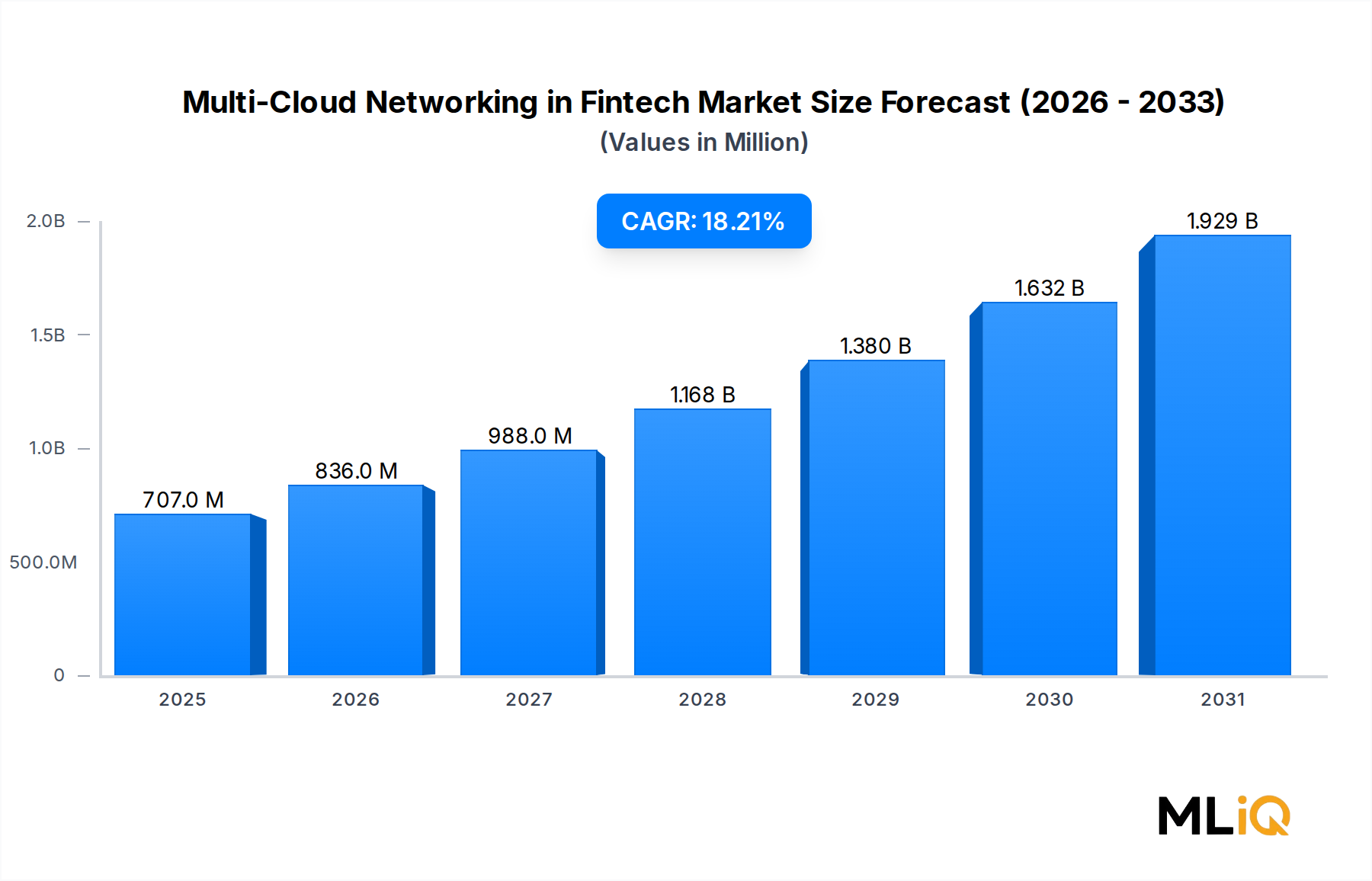

The segment's growth rate is expected to outpace the overall market CAGR of 18.2% through 2027, after which the Services segment may begin to narrow the gap as institutions outsource managed network operations to reduce internal IT overhead. However, through the medium term, the Solution segment will remain the primary revenue engine of the market.