1. What are the major growth drivers for the Invoice Factoring Market market?

Factors such as are projected to boost the Invoice Factoring Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

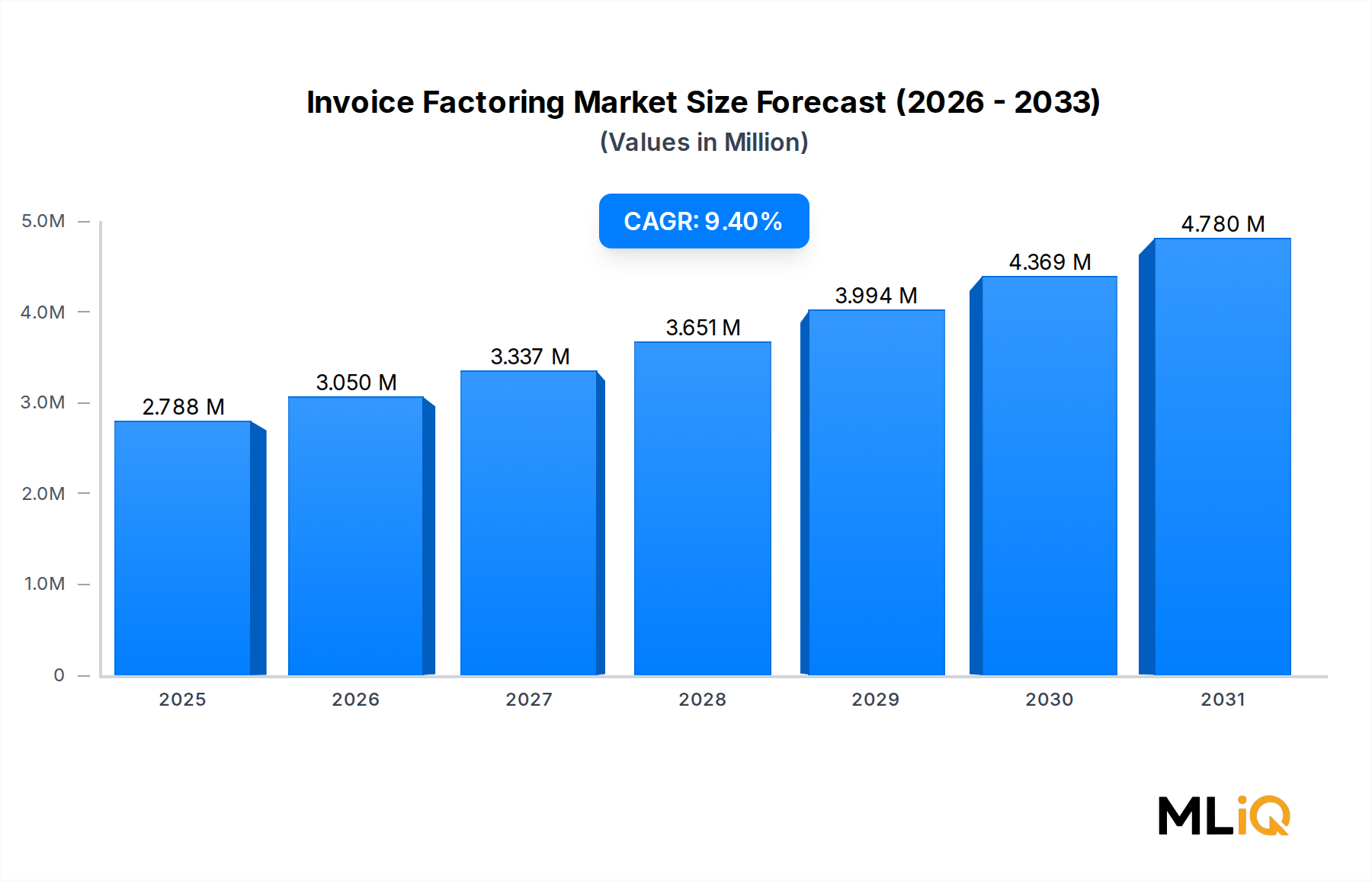

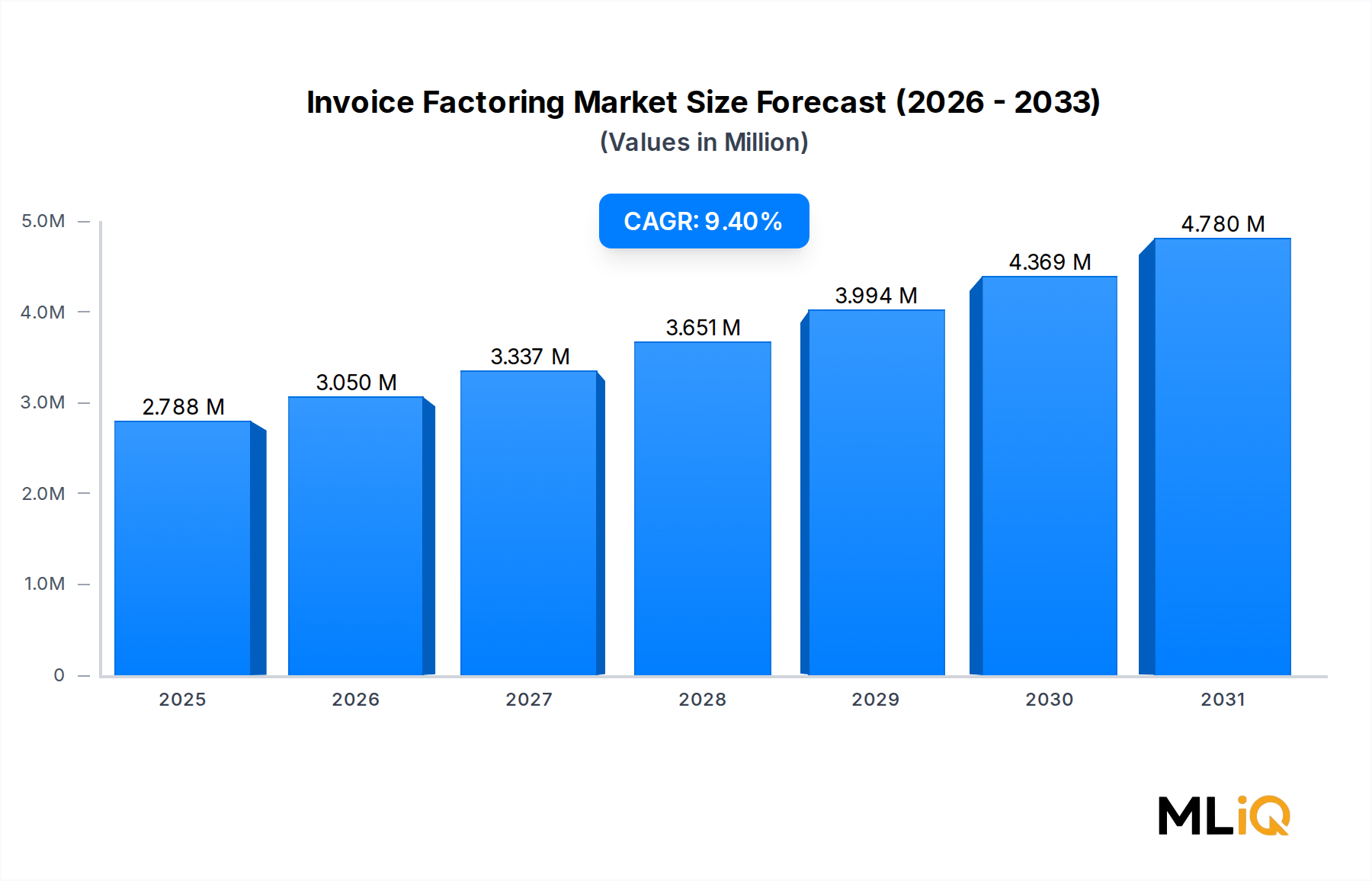

The global Invoice Factoring Market is valued at $2,788.20 billion as of the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 9.4% through 2033, reflecting robust demand for short-term liquidity solutions across industries navigating extended payment cycles. This market occupies a critical niche within the broader financial services ecosystem, enabling businesses—particularly small and medium-sized enterprises—to convert outstanding receivables into immediate working capital without incurring traditional debt obligations.

Several macro-level tailwinds are converging to sustain this trajectory. First, the structural mismatch between invoice issuance and payment settlement—often spanning 30 to 120 days in sectors such as construction, healthcare, and logistics—creates persistent cash flow pressure that factoring services are uniquely positioned to alleviate. Second, tightening credit conditions in conventional banking channels have redirected capital-hungry businesses toward alternative financing instruments. Third, digitization of financial workflows, including e-invoicing mandates in the European Union and ASEAN economies, is dramatically reducing friction in the factoring process, enabling real-time funding decisions.

The proliferation of fintech-enabled factoring platforms has disrupted legacy models dominated by traditional banks and non-banking financial companies (NBFCs). New entrants leveraging machine learning-based credit underwriting and API-integrated accounting software are compressing approval timelines from weeks to hours, democratizing access for micro-enterprises and seasonal businesses. This technological shift is particularly evident in emerging markets across South and Southeast Asia, where formal credit infrastructure remains underdeveloped.

Demand is also being shaped by international trade complexity. Exporters requiring advance liquidity against overseas receivables—without taking on currency or counterparty risk—are increasingly using non-recourse factoring structures. The Accounts Receivable Financing Market and the Invoice Factoring Market share overlapping clientele but differ in risk transfer mechanics, a distinction that continues to drive product differentiation among providers.

Looking forward through 2033, the market outlook remains constructive. The integration of blockchain-based invoice verification, open banking APIs, and embedded finance within enterprise resource planning (ERP) systems is expected to further accelerate adoption. Regulatory harmonization in cross-border factoring—particularly within the EU's single market framework—will reduce legal friction and stimulate international volume. Meanwhile, the continued growth of gig economy platforms and staffing firms creates a new, high-velocity receivables segment that factors are actively targeting. The combined effect of technological enablement, macroeconomic necessity, and regulatory support positions the Invoice Factoring Market for sustained double-digit momentum across most major geographic corridors.

Within the Invoice Factoring Market segmented by type, recourse factoring commands the largest revenue share, consistently accounting for the majority of transaction volume globally. Under recourse factoring arrangements, the client (seller) retains the credit risk if the end debtor fails to pay the invoice. In exchange for bearing this residual risk, clients receive more favorable advance rates and lower service fees compared to non-recourse structures, making recourse factoring the preferred instrument for cost-sensitive businesses with high-quality debtor portfolios.

The dominance of recourse factoring is fundamentally economic. For factors—whether banks or NBFCs—non-recourse arrangements require substantially larger credit reserves and more sophisticated underwriting infrastructure because the factor absorbs default risk outright. These additional costs are passed through to the client via higher discount rates, typically 0.5% to 2.0% higher than equivalent recourse facilities. As a result, businesses that have reasonable confidence in their debtors' creditworthiness actively self-select into recourse structures to minimize financing costs.

From a provider perspective, recourse factoring also allows institutions to scale their portfolios more rapidly. Because the credit exposure remains with the originating client rather than the factor, capital adequacy requirements under Basel III frameworks are comparatively lower for recourse-based receivable portfolios. This structural advantage enables banks—including large institutions such as Lloyds Bank and Barclays Bank UK PLC—to offer competitive pricing on recourse facilities while maintaining regulatory capital efficiency. It also allows NBFCs and fintech-native platforms to participate in the market without maintaining the heavy loss reserves associated with non-recourse books.

In large enterprise segments, recourse factoring is frequently embedded within broader revolving credit facilities or supply chain finance programs. Companies in manufacturing and construction—two of the highest-volume industry verticals in this market—tend to have recurring, high-value invoices against established counterparties (government agencies, Tier 1 manufacturers, large retailers), where default probability is manageable and recourse exposure is an acceptable trade-off for pricing benefits.

For small and medium-sized enterprises (SMEs), recourse factoring is often the only practically accessible option. Non-recourse facilities require the factor to conduct deep credit analysis on the SME's debtor base, which involves significant underwriting cost that cannot be amortized over small ticket sizes. Recourse arrangements sidestep this barrier, enabling SMEs in staffing, transportation and logistics, and IT services to access liquidity against invoices that would otherwise sit locked in 60-to-90-day payment terms.

The share of recourse factoring is consolidating rather than declining, even as non-recourse volumes grow in absolute terms. The non-recourse segment is gaining traction in international factoring corridors—particularly cross-border transactions involving emerging market debtors where counterparty risk assessment is difficult—but it remains a minority share globally. Fintech platforms such as Velotrade and Waddle have introduced hybrid structures that blend elements of both, using algorithmic debtor scoring to price risk dynamically, yet their core product architecture still defaults to recourse mechanics for domestic receivables.

From a geographic standpoint, recourse factoring is most dominant in mature European markets (Germany, France, the United Kingdom) and North America, where established legal frameworks for receivables assignment and debt recovery give factors confidence in exercising recourse rights. In these markets, the legal enforceability of recourse clauses is well-tested, reducing the operational risk that would otherwise undermine the model's attractiveness. This legal maturity further entrenches recourse factoring as the segment of choice for high-volume, institutionally-originated invoice portfolios.

The Invoice Factoring Market is propelled by a confluence of structural and cyclical drivers, while facing a set of quantifiable constraints that factors and policymakers must navigate carefully.

Driver 1 — SME Credit Gap: The World Bank estimates the global SME financing gap at approximately $5.2 trillion annually, with the shortfall most acute in Asia Pacific and Sub-Saharan Africa. This unmet demand directly translates into factoring opportunity, as SMEs unable to secure bank credit lines turn to receivables monetization. The Small Business Lending Market and invoice factoring are increasingly viewed as complementary, with factors filling gaps that traditional lenders cannot profitably serve.

Driver 2 — Extended Payment Terms: Average days sales outstanding (DSO) across industries rose to 66 days globally in recent years, driven by large buyers leveraging their negotiating power to extend supplier payment cycles. Every additional day of DSO represents incremental demand for factoring services, particularly in construction (90–120 day terms) and healthcare (government payer settlement delays averaging 45–75 days).

Driver 3 — Digital Integration: The Trade Finance Market is undergoing rapid digitization, with e-invoicing adoption rates exceeding 80% in Scandinavian markets and accelerating across the EU, ASEAN, and Latin America. Digital invoice trails reduce fraud risk for factors, enabling automation of credit decisioning and dramatically improving unit economics.

Driver 4 — Regulatory Support: The EU Late Payment Directive reform proposals target maximum payment terms of 30 days for B2B transactions, paradoxically incentivizing factoring as companies adjust cash flow management during the transition period.

Constraint 1 — Fraud and Invoice Duplication Risk: Double-pledging of invoices—submitting the same receivable to multiple factors—remains an unresolved operational risk, estimated to represent 3–5% of fraudulent factoring transactions in markets lacking centralized invoice registries.

Constraint 2 — High Cost of Capital for NBFCs: Rising benchmark interest rates have increased the cost of funds for non-bank factors by 150–200 basis points in key markets since 2022, compressing margins and limiting their ability to compete with bank-sponsored facilities.

Constraint 3 — Regulatory Fragmentation: Cross-border factoring faces inconsistent legal treatment of receivables assignment across jurisdictions, raising compliance costs and limiting the addressable market for international transactions.

American Express Company: Operates commercial lending and working capital solutions through its business financing division, leveraging its global merchant network and deep data analytics to offer invoice-based financing to SMEs with integrated spend management capabilities.

Sonovate: A UK-based specialist factor focused exclusively on the staffing and recruitment sector, providing embedded payroll financing and invoice funding to recruitment agencies, with technology-driven onboarding that reduces time-to-funding to under 24 hours.

Lloyds Bank: One of the United Kingdom's largest providers of invoice finance, offering both disclosed and confidential factoring products through its commercial banking arm, with particular strength in mid-market manufacturing and distribution clients.

Barclays Bank UK PLC: Provides a comprehensive suite of receivables financing solutions including selective invoice finance, whole-ledger factoring, and asset-based lending, targeting large corporates and fast-growth SMEs across the UK and European markets.

Adobe: Participates tangentially through its Document Cloud and Acrobat Sign platforms, which underpin e-invoicing and digital contract execution workflows that form the documentary foundation of modern factoring transactions, particularly in the fintech integration layer.

Velotrade: A Hong Kong-headquartered fintech platform enabling cross-border invoice trading between Asian exporters and institutional investors, using a marketplace model that creates secondary liquidity for trade receivables across ASEAN and Greater China corridors.

Waddle: An Australian fintech-native factoring platform that integrates directly with cloud accounting software (Xero, QuickBooks), offering automated invoice financing to SMEs with a fully digital underwriting process and same-day funding capability.

Intuit Inc.: Through its QuickBooks platform, Intuit has embedded invoice financing features that allow SMEs to access early payment on outstanding invoices within their existing accounting ecosystem, blurring the boundary between software and financial services.

ICBC (Industrial and Commercial Bank of China): The world's largest bank by assets, ICBC offers domestic and cross-border factoring services through its trade finance division, with dominant market presence in China's manufacturing export corridors and growing reach across Belt and Road Initiative trade routes.

Porter Capital: A US-based independent factoring company specializing in high-touch, relationship-driven factoring for SMEs in staffing, transportation, and manufacturing, competing on speed of service and sector expertise rather than price.

January 2024: The European Commission published final guidelines under the revised Late Payment Regulation, mandating maximum 30-day B2B payment terms across EU member states, triggering increased factoring adoption as suppliers restructure cash flow management strategies.

March 2024: Intuit Inc. expanded its QuickBooks Capital invoice financing product to three additional markets in the Asia Pacific region, extending embedded factoring access to over 500,000 new SME users on its platform.

May 2024: Velotrade announced a strategic partnership with a Singaporean sovereign wealth-backed trade finance fund, securing $150 million in institutional capital to expand its cross-border invoice marketplace across Southeast Asian export corridors.

August 2024: The UK's Financial Conduct Authority (FCA) issued updated guidance on disclosure requirements for invoice finance agreements, requiring greater transparency on fee structures and recourse conditions, effective from Q1 2025.

October 2024: Sonovate raised a £100 million credit facility from a consortium of European institutional lenders to scale its staffing-sector factoring operations, targeting 30% year-over-year growth in funded invoices through 2025.

December 2024: ICBC's trade finance division launched a blockchain-integrated factoring platform for Chinese manufacturing exporters, reducing invoice verification time from 3 days to under 4 hours and enabling real-time funding decisions for cross-border receivables.

February 2025: Porter Capital announced expansion into the healthcare staffing vertical, launching a dedicated product line for travel nurse agencies facing 60–90 day government payer delays, with an initial portfolio target of $75 million in funded receivables.

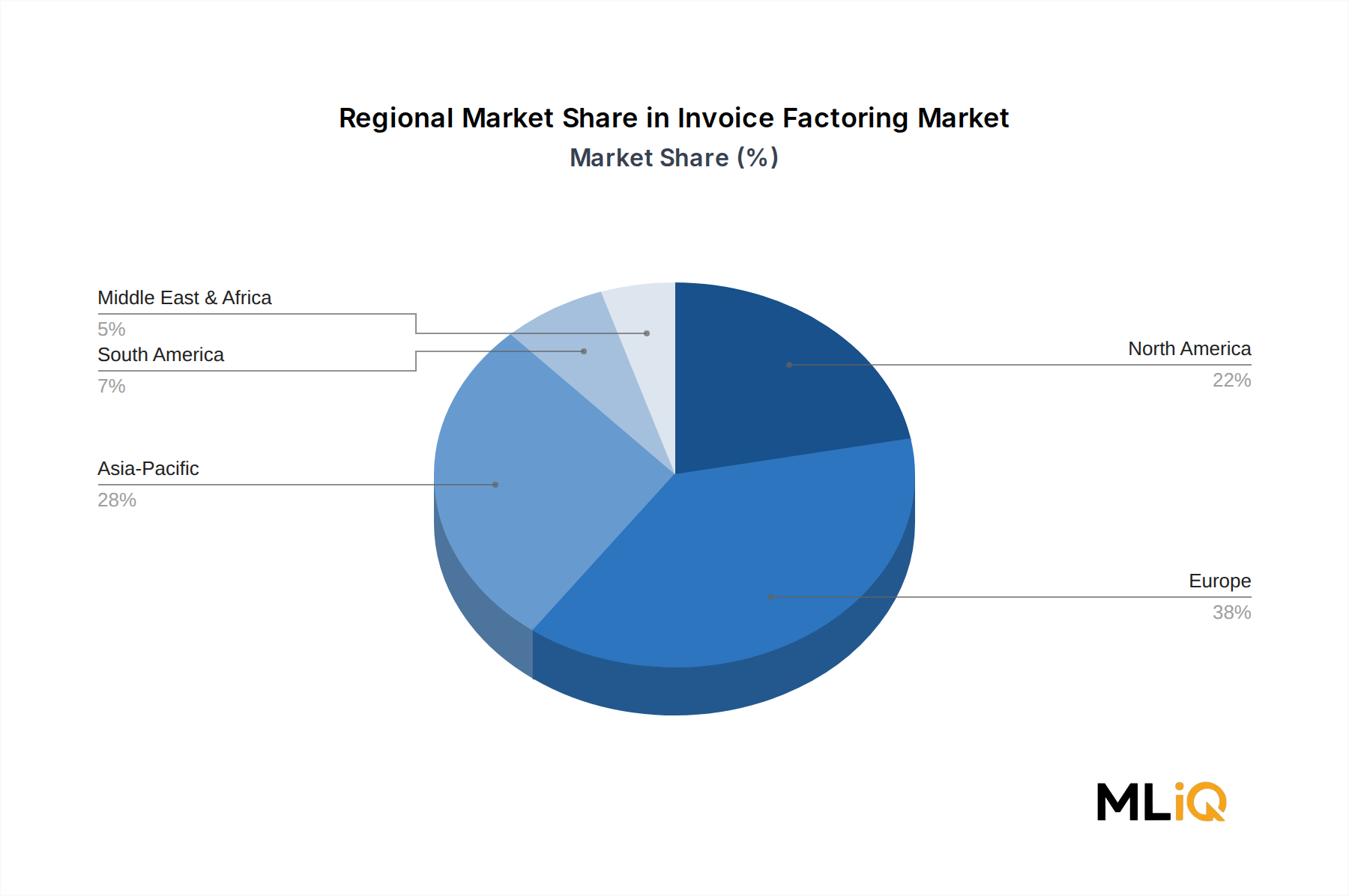

The Invoice Factoring Market exhibits significant regional variation in maturity, growth velocity, and dominant use case, reflecting differences in financial infrastructure, regulatory environment, and SME credit access.

Europe remains the most mature and largest regional market, accounting for an estimated 40–45% of global factoring volume. The EU's well-established legal framework for receivables assignment, combined with the Factors Chain International (FCI) network facilitating cross-border two-factor transactions, positions Western Europe as the structural anchor of global factoring activity. Germany, France, and the United Kingdom collectively represent the lion's share of European volume. Regional CAGR is estimated at 6.5–7.5% through 2033, reflecting slower but deeply entrenched growth in an already-penetrated market.

Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR of 12–14% over the forecast period. China alone accounts for a disproportionate share of regional volume, driven by the manufacturing export sector's extensive use of both domestic and cross-border factoring. India is emerging as a high-momentum sub-market, with the Reserve Bank of India's Trade Receivables Discounting System (TReDS) platform catalyzing SME factoring adoption. Japan and South Korea contribute stable institutional volumes through bank-affiliated factoring arms.

North America represents the second-largest market by revenue, with the United States dominating regional activity. The US market is characterized by high fragmentation—thousands of independent factors serve niche verticals including transportation, staffing, and construction—alongside large bank-affiliated programs. Regional CAGR is estimated at 8.0–9.0%, driven by persistent SME credit gaps and increasing fintech penetration.

The Middle East and Africa region is at an early but accelerating stage, with Gulf Cooperation Council (GCC) economies—particularly the UAE and Saudi Arabia—investing in trade finance infrastructure aligned with Vision 2030 diversification goals. Regional factoring volumes remain small in absolute terms but are growing at an estimated 11–13% CAGR, underpinned by expanding intra-regional trade and government-backed SME finance initiatives.

South America, led by Brazil and Argentina, faces macroeconomic volatility that suppresses predictable growth. Brazil's robust receivables discounting market (nota fiscal infrastructure) provides a foundation, but currency risk and inflationary pressures constrain cross-border factoring expansion. Regional CAGR is estimated at 7.0–8.5%, with growth contingent on macroeconomic stabilization.

Cross-border invoice factoring—commonly structured as international two-factor transactions under FCI conventions—represents a growing share of global factoring volume, estimated at 25–30% of total market activity. The primary trade corridors driving international factoring demand include China-to-Europe manufacturing exports, intra-EU trade flows (Germany-France-Italy), US-to-Latin America commercial transactions, and emerging ASEAN-to-Middle East commodity and light manufacturing flows.

China is the world's largest exporter of manufactured goods and correspondingly the largest originator of cross-border factoring receivables. Chinese exporters face persistent collection risk on foreign invoices, particularly from emerging market buyers, driving strong demand for non-recourse international factoring structures. The Belt and Road Initiative has extended Chinese trade credit exposure across Central Asia, Eastern Africa, and Southern Europe, creating new corridors for factoring intermediation.

Tariff escalation—particularly the successive rounds of US-China trade tariffs since 2018, augmented by additional measures in 2024–2025—has created two countervailing effects on international factoring. First, trade flow diversion toward alternative manufacturing hubs (Vietnam,

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.4% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Invoice Factoring Market market expansion.

Key companies in the market include American Express Company, Sonovate, Lloyds Bank, Barclays Bank UK PLC, Adobe, Velotrade, Waddle, Intuit Inc., ICBC, Porter Capital.

The market segments include Type, Enterprise Size, Provider, Application, Industry Vertical.

The market size is estimated to be USD 2788.20 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Invoice Factoring Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Invoice Factoring Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.