Within the Polytetrahydrofuran Market, the spandex fiber application segment represents the single largest revenue contributor, consistently accounting for approximately 60–65% of total global PolyTHF consumption in 2024. This dominance is structural rather than cyclical, rooted in the chemical essentiality of PolyTHF as the soft-segment precursor in spandex synthesis.

Spandex, or elastane, is a segmented polyurethane-polyurea copolymer whose extraordinary stretch-recovery properties derive directly from long-chain PolyTHF soft segments alternating with rigid diisocyanate hard segments. No technically or economically competitive substitute for PolyTHF in mainstream spandex manufacturing has emerged, creating a durable demand moat. Standard spandex grades typically utilize PolyTHF with molecular weights in the 1,000–2,000 Da range, with higher-denier specialty fibers increasingly demanding tighter molecular weight distribution.

The Spandex Fiber Market has itself expanded briskly, growing at an estimated 6–8% CAGR globally through the early 2020s, propelled by the structural shift toward stretch fabrics in casual wear, activewear, intimate apparel, and medical textiles. Each percentage point of penetration gain in global fabric output translates directly into proportional PolyTHF demand uplift, creating a reliable long-cycle demand corridor.

Key players anchoring the spandex-linked segment of PolyTHF demand include INVISTA (the producer of the LYCRA brand), Hyosung Chemical Fiber, Formosa Asahi Spandex, and Jianfeng Chemical. These manufacturers operate integrated or quasi-integrated supply chains, often securing long-term PolyTHF offtake agreements with upstream producers such as BASF, Korea PTG, and Dairen Chemical Corporation. The vertical integration tendency among major spandex producers moderates spot market volatility but can create captive demand silos that limit independent PolyTHF distributors.

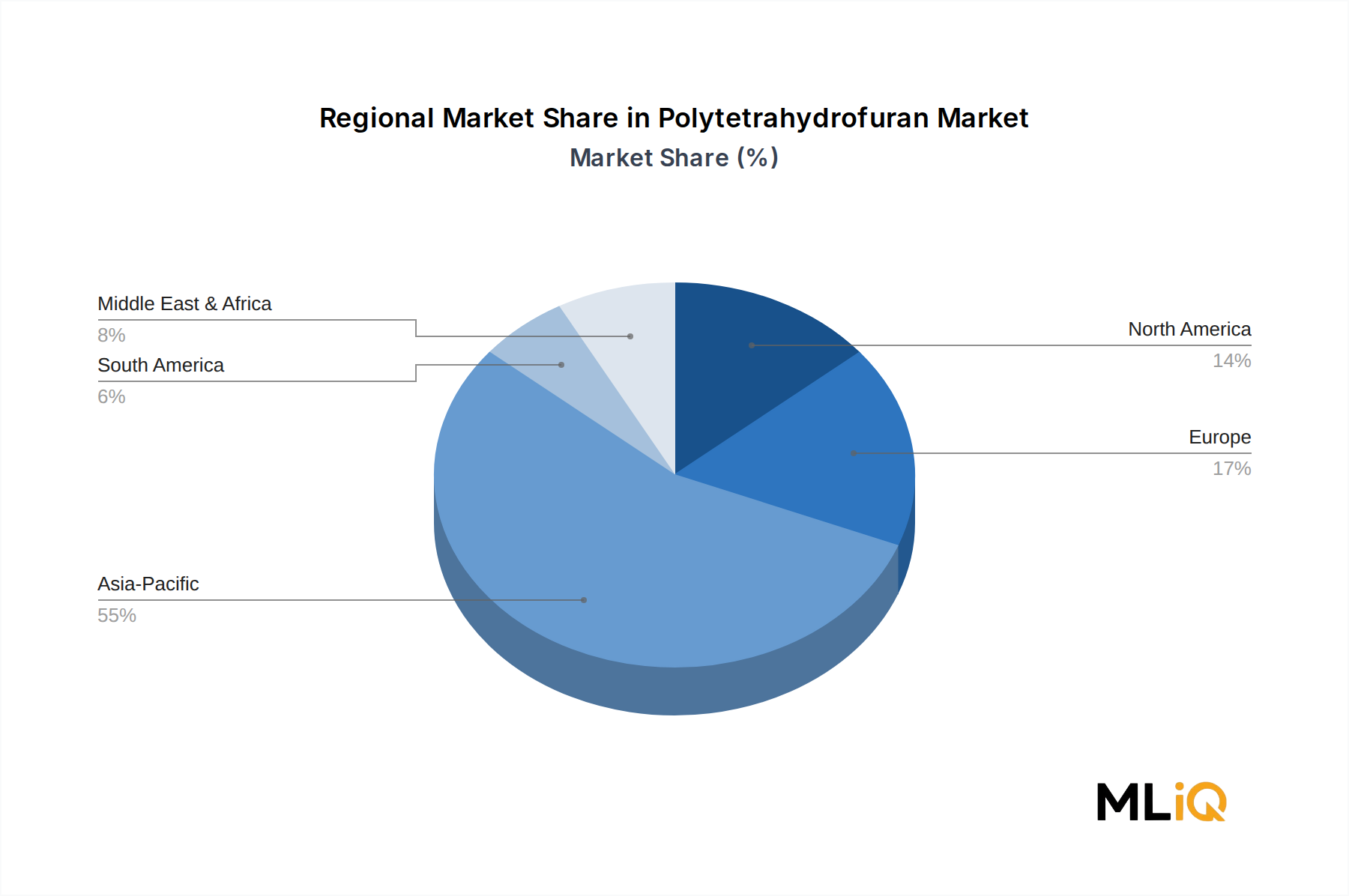

Geographically, China dominates spandex production capacity, housing more than 70% of global installed nameplate capacity as of 2024, with Hyosung Chemical Fiber and Jianfeng Chemical among the most prominent domestic capacity holders. India has emerged as the second-fastest growing spandex demand market, driven by its expanding domestic textile manufacturing ecosystem and export-oriented garment sector. South Korea, historically a spandex innovation hub, maintains high-value specialty grade advantages.

The segment's share is not merely holding steady — it is gradually consolidating further as developing-market consumption penetration deepens. In markets such as Southeast Asia, sub-Saharan Africa, and Latin America, spandex content per garment is still rising from low baseline levels, providing incremental demand increments that aggregate to meaningful PolyTHF volume growth annually.

Grade premiumization is a critical sub-trend. High-performance spandex applications — including compression sportswear, medical hosiery, and swimwear — require PolyTHF with tighter specifications around molecular weight distribution, viscosity, and color. These premium-grade volumes command 15–25% price premiums over commodity grades, incentivizing producers such as BASF and INVISTA to invest in quality control infrastructure and specialty grade portfolios.

Looking ahead, the continued global ascendancy of activewear and athleisure as normalized fashion categories, combined with demographic aging (which drives medical compression garment use), ensures that the spandex fiber application segment will retain its dominant position within the Polytetrahydrofuran Market for the foreseeable forecast period.