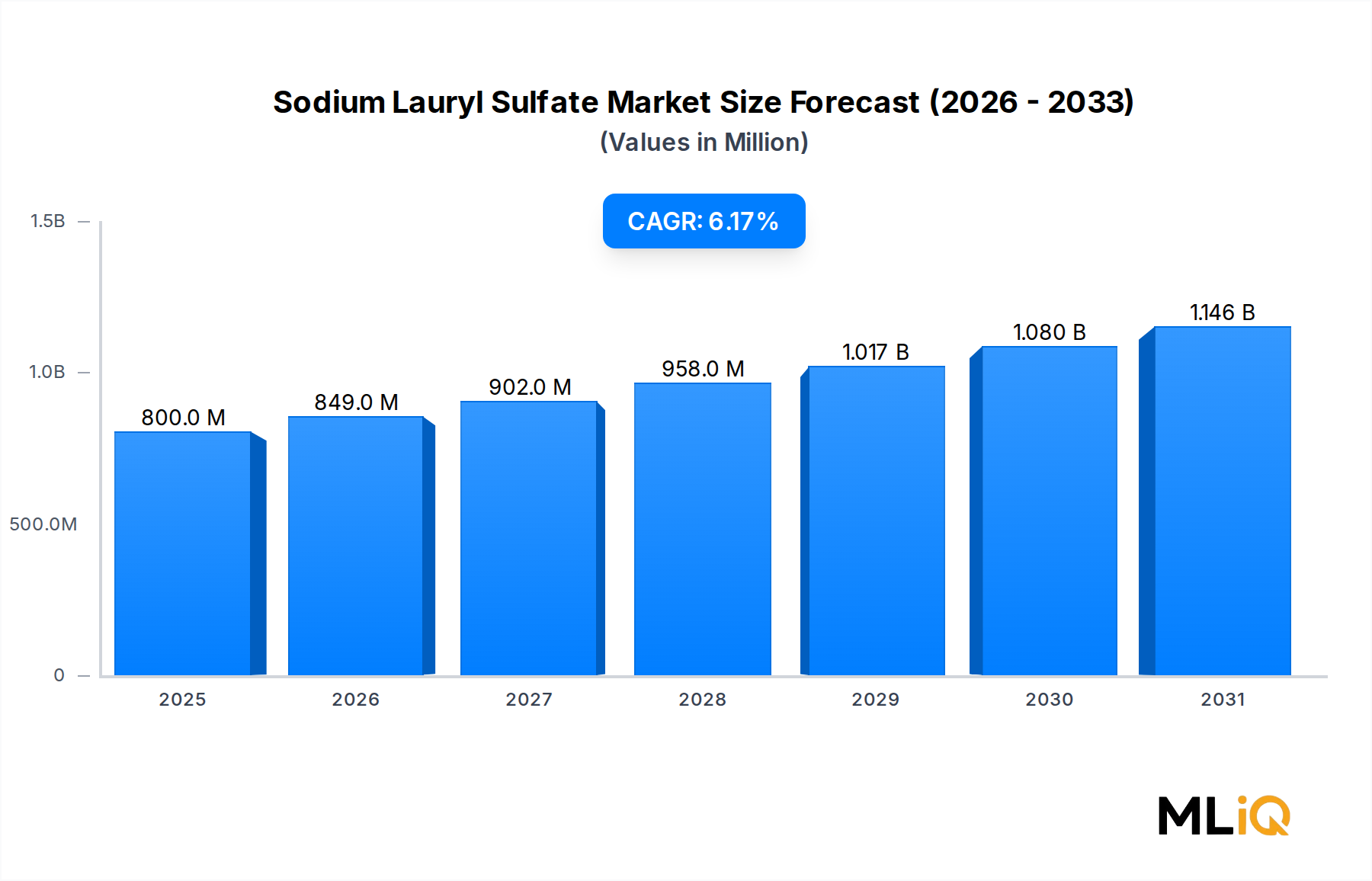

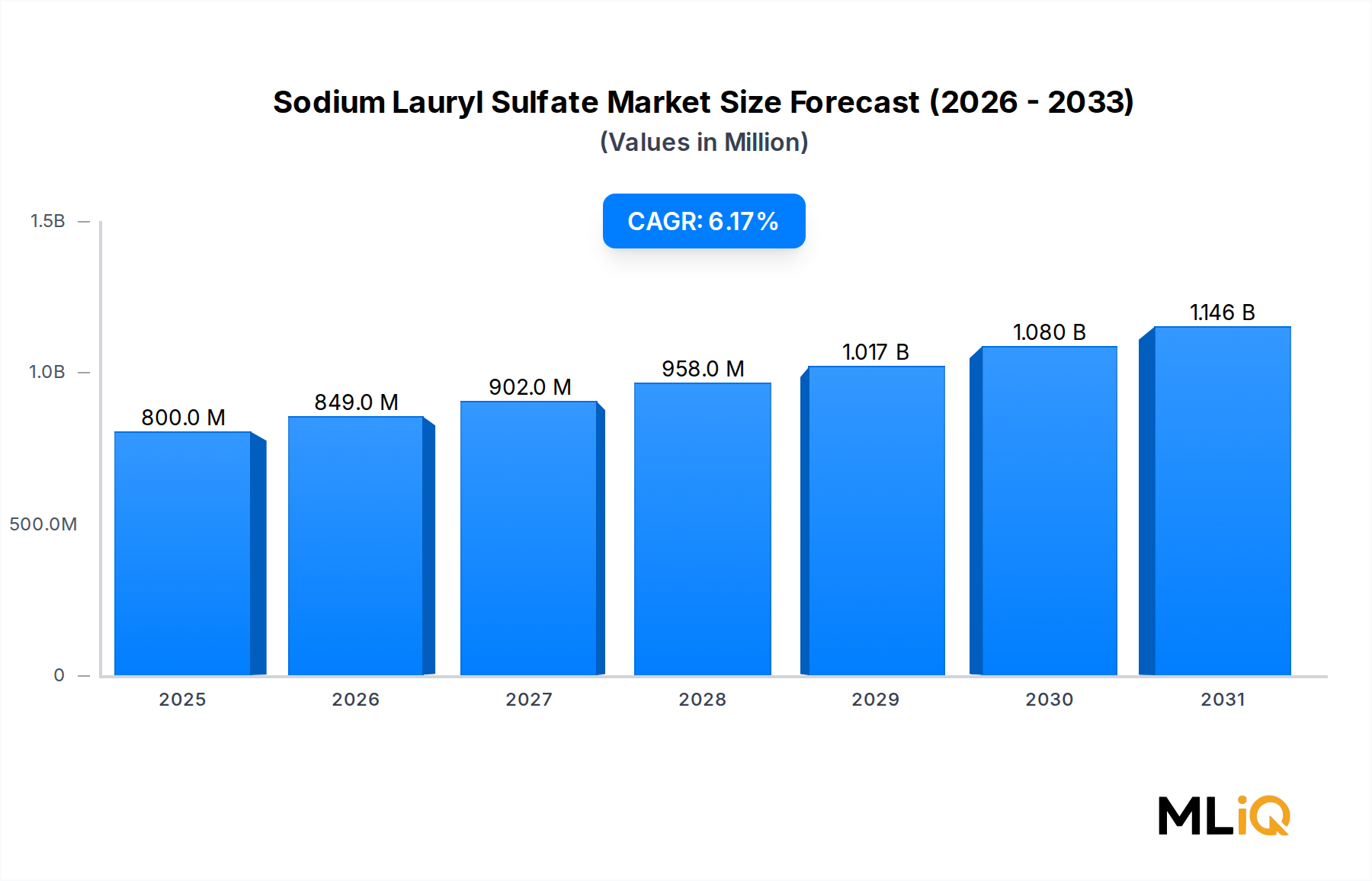

The global Sodium Lauryl Sulfate Market is valued at approximately $0.8 billion as of the base year and is projected to expand at a compound annual growth rate (CAGR) of 6.18% through the forecast period of 2025 to 2033. This steady trajectory reflects entrenched demand from household and industrial cleaning applications, alongside an accelerating uptake in personal care and cosmetic formulations across emerging economies. By 2033, the market is anticipated to reach a substantially higher valuation, underpinned by rising consumer awareness of hygiene, urbanization-led consumption patterns, and the continued proliferation of premium personal care products in Asia-Pacific.

Sodium Lauryl Sulfate (SLS), an anionic surfactant derived primarily from lauryl alcohol, is recognized for its exceptional foaming, emulsifying, and cleaning properties. These functional characteristics make it a preferred ingredient across detergents, shampoos, toothpastes, body washes, and a wide range of industrial cleaning agents. The ingredient's cost-effectiveness relative to alternatives continues to reinforce its dominant position in mass-market formulations globally.

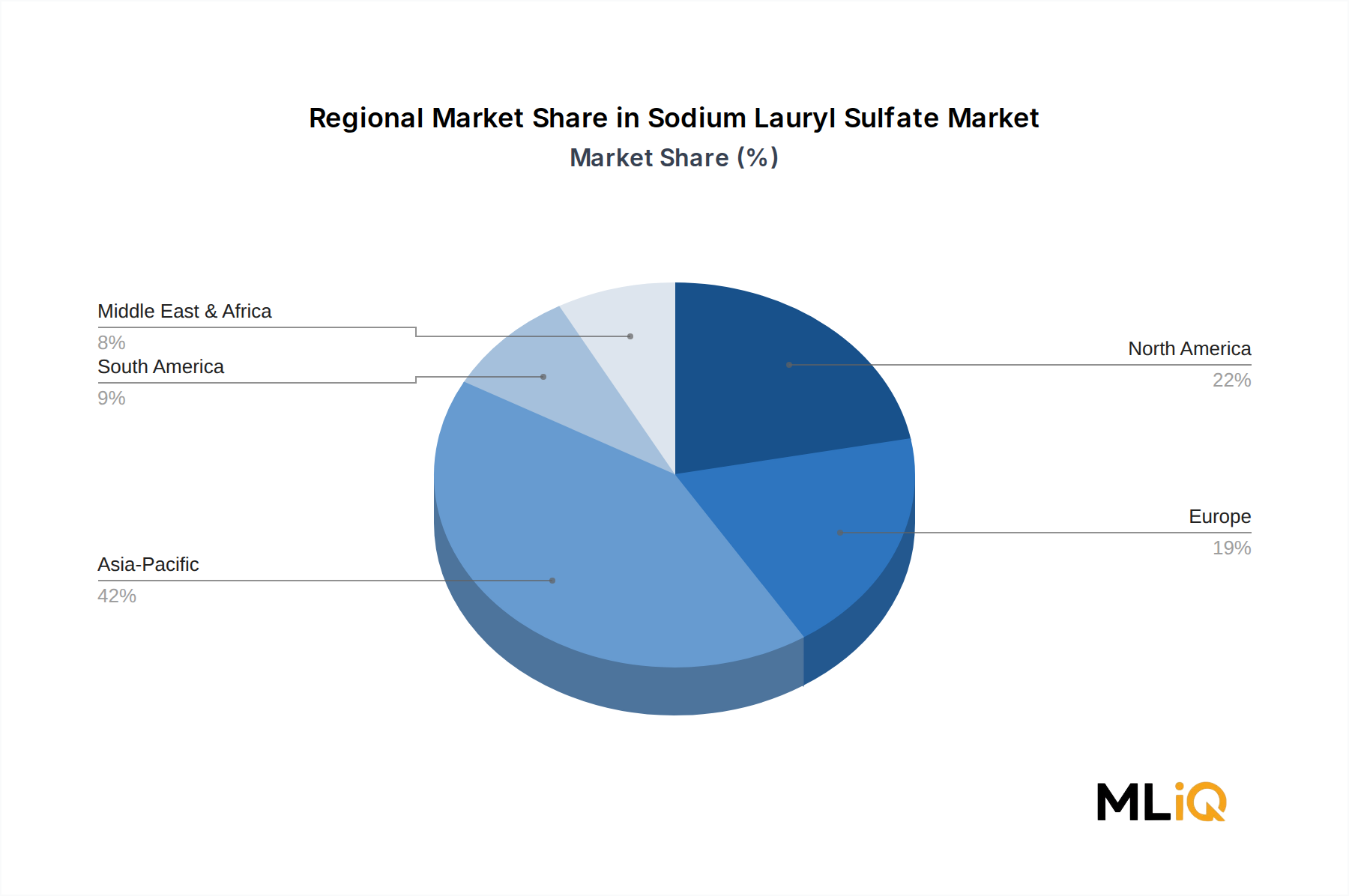

Key demand drivers include robust growth in the detergent and cleaner segment, which benefits from heightened hygiene consciousness following pandemic-era behavioral shifts that have proven structurally persistent. In Asia-Pacific, rising disposable incomes and the rapid expansion of the personal care industry — particularly in China, India, and ASEAN nations — are creating incremental volume demand at a pace that outstrips other regions. The personal care ingredients segment, which draws heavily on SLS formulations, is recording some of the fastest adoption rates globally.

On the macroeconomic side, expanding middle-class populations in South and Southeast Asia, Latin America, and Sub-Saharan Africa are translating into first-time buyers of branded personal care and household cleaning goods. This democratization of consumer spending is structurally favorable for SLS, which remains price-competitive versus bio-based alternatives.

However, the market faces notable headwinds. Growing regulatory scrutiny around SLS's dermatological and environmental impact is prompting formulators in Europe and North America to reformulate with milder surfactants. Bio-based and sulfate-free product trends, driven by clean-beauty advocacy and green labeling requirements, are gradually eroding SLS's share in premium product segments. The competitive pressure from Sodium Laureth Sulfate Market products — which offer a milder skin-contact profile — and from emerging biosurfactant technologies adds further complexity to the longer-term demand outlook.

Despite these constraints, the overall forward-looking outlook for the Sodium Lauryl Sulfate Market remains positive through 2033, with volume growth supported by high-growth emerging markets compensating for gradual share erosion in mature, sustainability-sensitive markets. Strategic investment in process optimization and greener production routes is expected to sustain the commercial viability of SLS in a diversifying surfactants landscape.