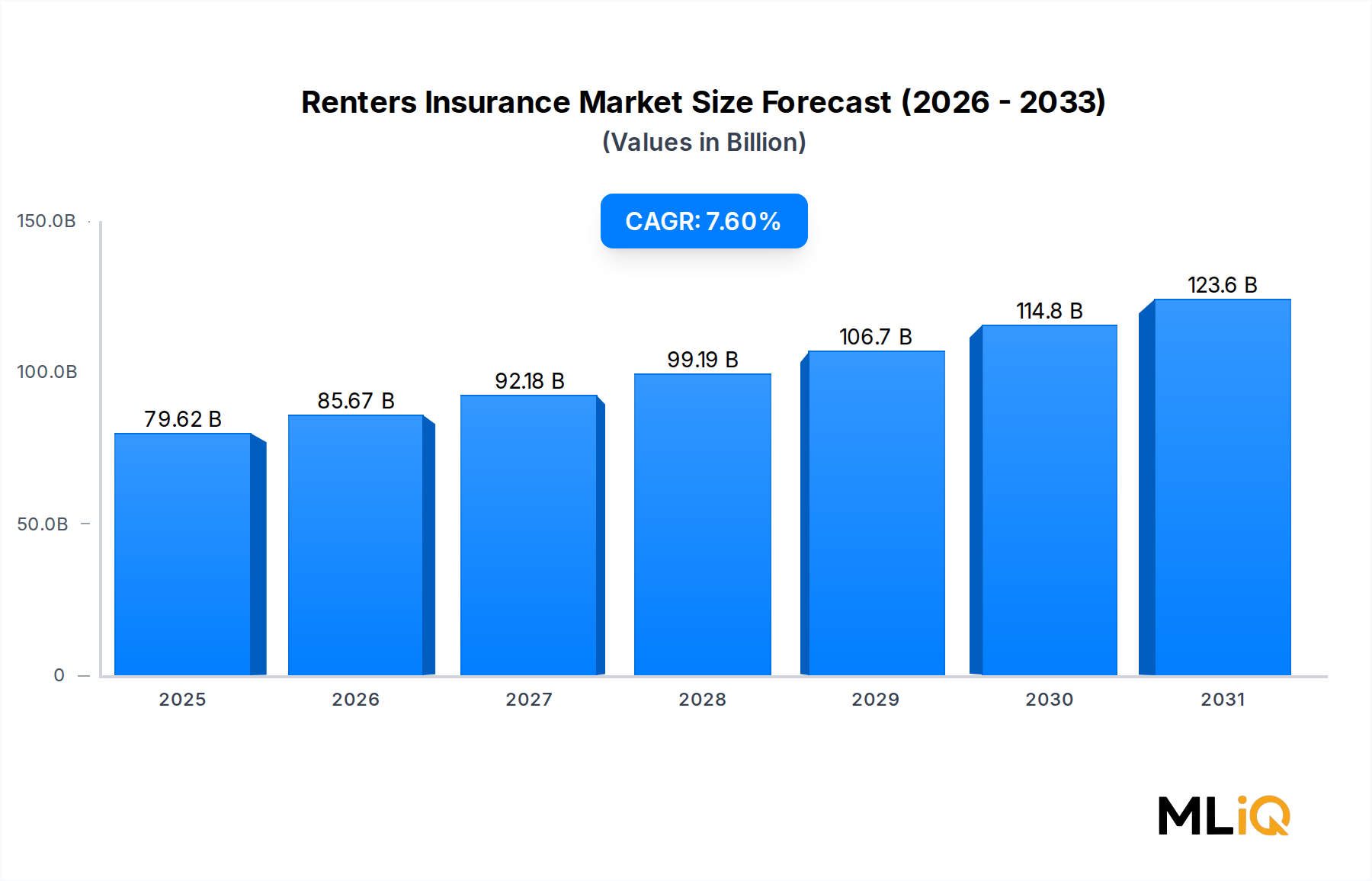

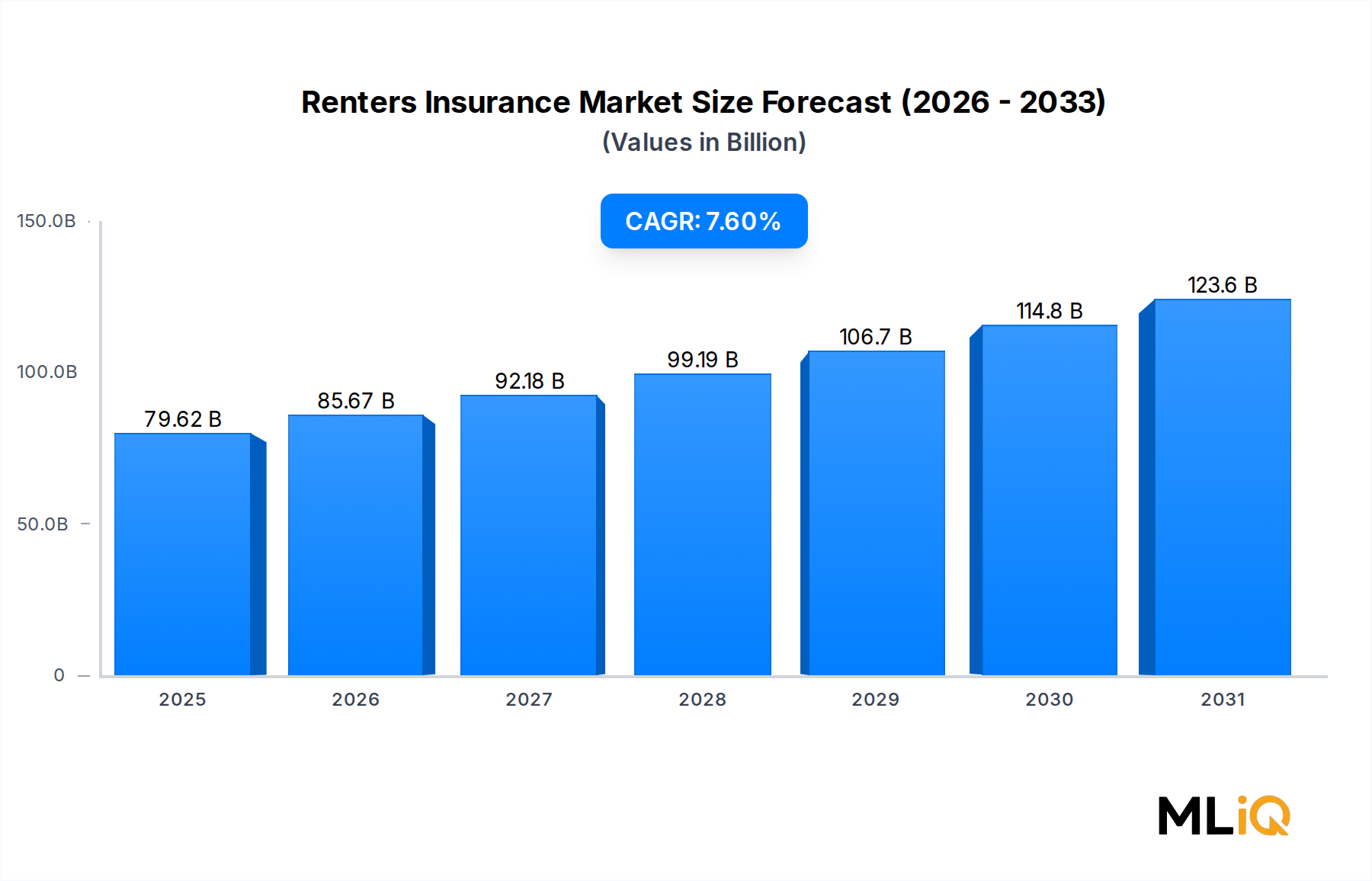

Several quantifiable forces are actively shaping the trajectory of the Renters Insurance Market, spanning structural demand drivers, competitive dynamics, and macroeconomic constraints.

Rising Rental Household Formation: The U.S. Census Bureau and comparable European housing authorities have documented a sustained increase in renter-occupied households. In the United States alone, the share of renter-occupied housing units exceeded 36% of total housing stock as of 2024, up from approximately 31% in 2010. This structural shift, driven by affordability barriers to homeownership, directly expands the addressable market. Similar trends are documented in the United Kingdom, Germany, and Australia, where home price-to-income ratios have reached historical highs, locking working-age populations into long-term rental arrangements.

Digitization of Distribution Channels: The penetration of digital-first insurers and direct-to-consumer online platforms has materially reduced customer acquisition costs and policy issuance timelines. Carriers reporting digital channel adoption rates above 60% of new policy originations have simultaneously reported lower expense ratios, enabling more competitive pricing that draws previously uninsured renters into the market. This is directly relevant to participants in the Digital Insurance Platform Market who are building the infrastructure enabling this shift.

Escalating Personal Property Replacement Costs: Consumer price inflation, particularly in electronics and household goods, has increased the average personal property value per rental unit. Industry surveys suggest average declared property values rose approximately 22% between 2020 and 2024, mechanically increasing premium revenue per policy even before volume growth is applied.

Constraint — Low Awareness and Perceived Necessity: Despite structural tailwinds, a critical restraint remains the fundamental awareness gap. Surveys consistently indicate that upward of 55% of uninsured renters either are unaware that renters insurance exists as a distinct product or believe it is automatically provided by their landlord's building policy. Overcoming this awareness deficit requires sustained marketing investment that many smaller carriers cannot absorb.

Constraint — Catastrophe Loss Volatility: Increasing frequency and severity of natural catastrophes — wildfires in California, flooding in Central Europe, and hurricane activity in the Gulf Coast — are elevating loss ratios and prompting reinsurance cost escalation. Several carriers exited certain high-risk ZIP codes in 2023 and 2024, reducing coverage availability in precisely the markets with the highest demand growth. This constraint creates a geographic tension between market opportunity and underwriting viability that regulators and carriers must collectively resolve.",

"