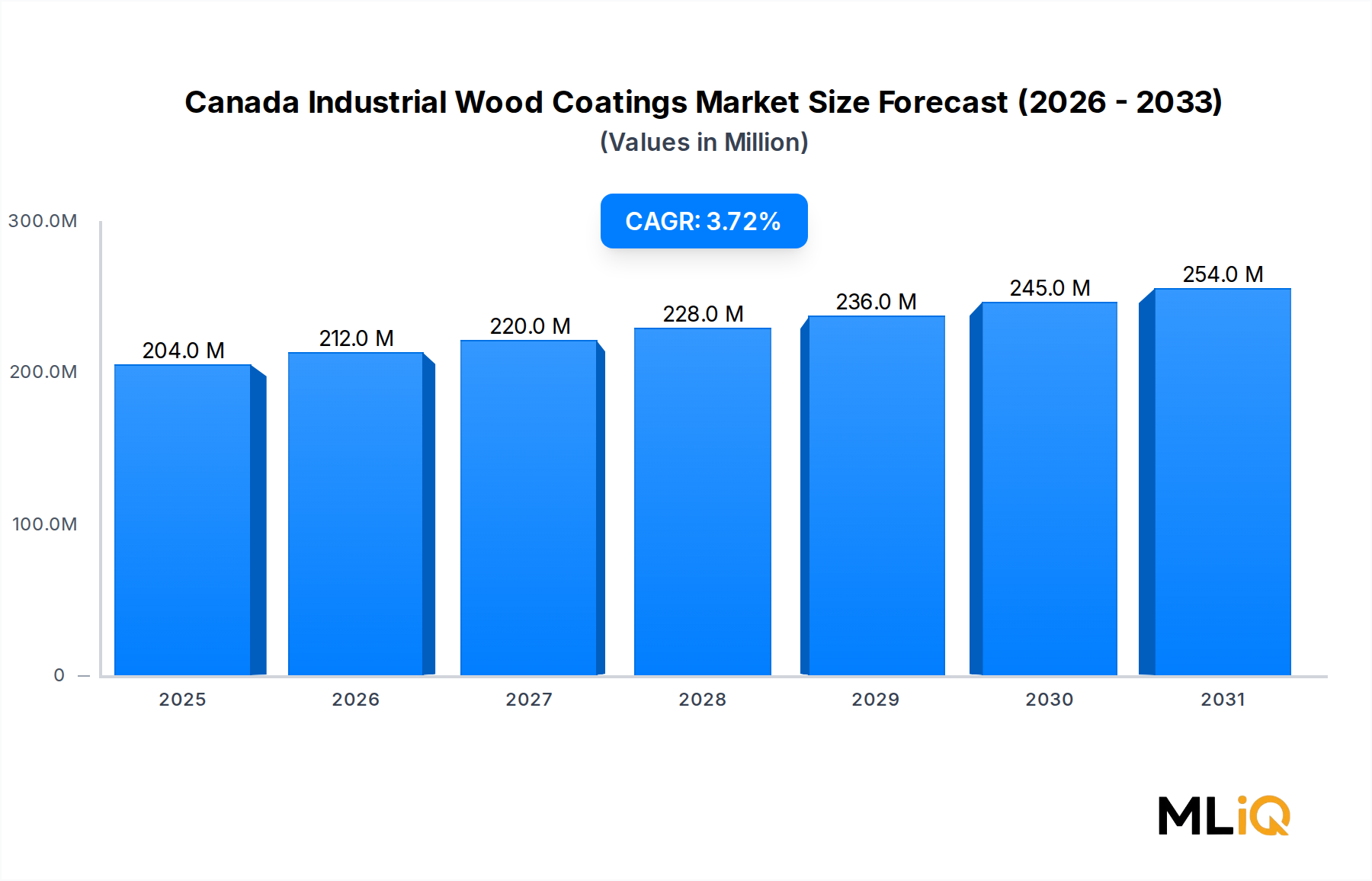

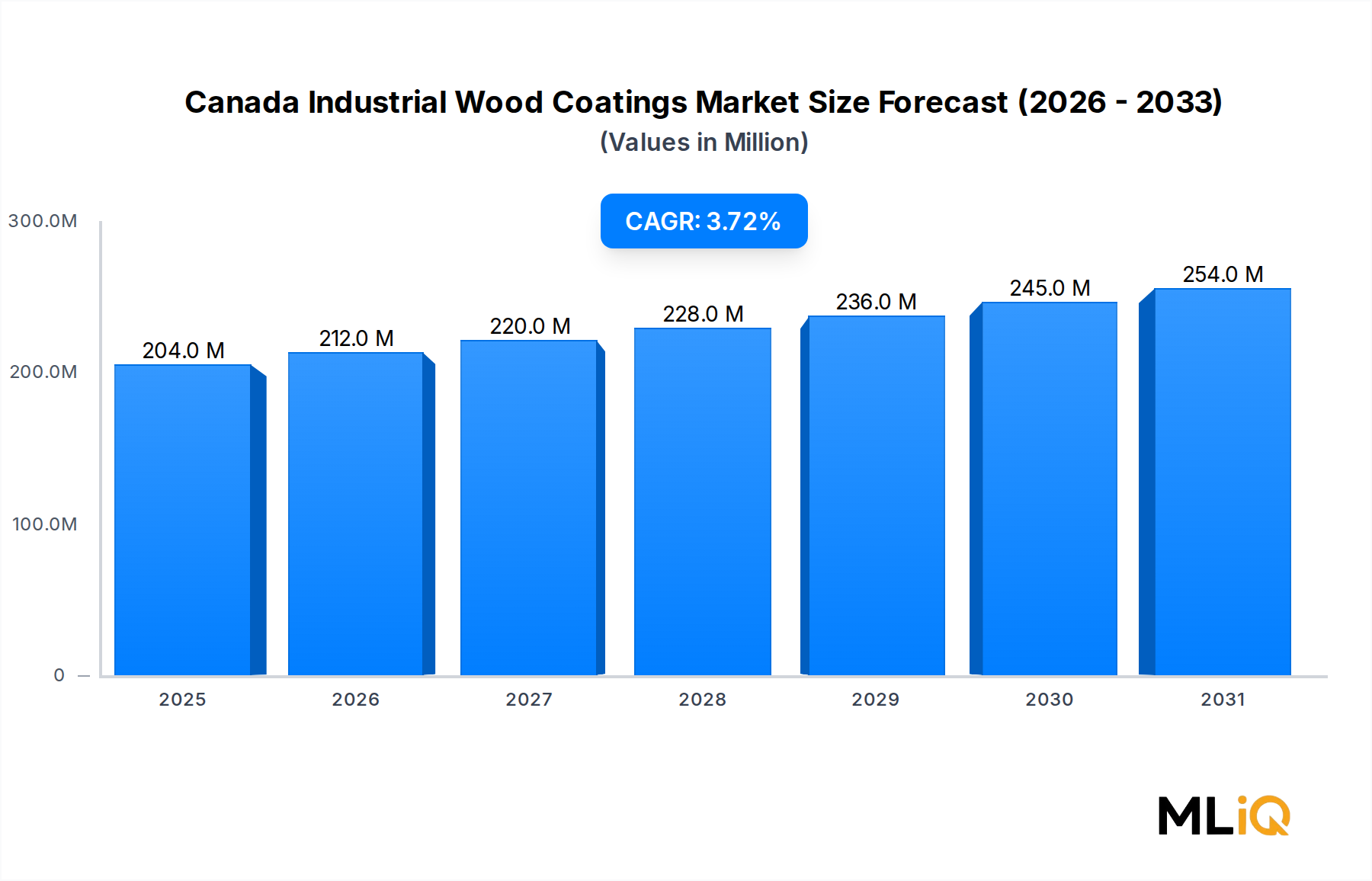

The Canada Industrial Wood Coatings Market is governed by a specific set of quantifiable drivers and measurable constraints that shape investment decisions, product development priorities, and competitive positioning.

Growing Usage of Wooden Furniture: Canada's residential construction sector has sustained elevated activity, with Statistics Canada reporting housing starts consistently above 200,000 units annually in recent years. Each new residential unit generates downstream demand for wood furniture and cabinetry, directly stimulating industrial wood coatings consumption. The premium furniture segment, which commands higher coating spend per unit, has been expanding as Canadian consumers increase expenditures on home improvement post-pandemic.

Increasing Demand from the Construction Industry: The federal government's USD 3.5 million investment in Vancouver's 2150 Keith Drive hybrid mass timber building, announced in July 2023, exemplifies a broader policy-driven push toward engineered wood in commercial construction. Mass timber structures require specialized coatings for fire resistance, moisture management, and aesthetic finishing, representing a structurally new demand vector for industrial wood coating formulators.

Increasing Demand from the Joinery Sector: Architectural joinery — encompassing doors, windows, staircases, and millwork — is a high-value coating application growing at an above-average rate within the market. The trend toward custom residential and commercial interiors is driving millwork producers to invest in high-performance, rapid-cure coating systems that support just-in-time production models.

VOC Emission Regulations: Environment and Climate Change Canada's increasingly stringent VOC content limits for architectural and industrial coatings represent a material compliance cost for solvent-borne coating producers. Companies that have not yet transitioned to compliant water-borne or high-solids formulations face regulatory risk and potential market exclusion, acting as a growth restraint on legacy product lines.

Availability of Alternative Materials: The penetration of high-pressure laminate (HPL), medium-density fiberboard (MDF) with paper foil, and powder-coated metal in the furniture and cabinetry markets provides end-users with cost-competitive alternatives to solid and veneer wood surfaces, reducing the addressable substrate base for wood coatings.