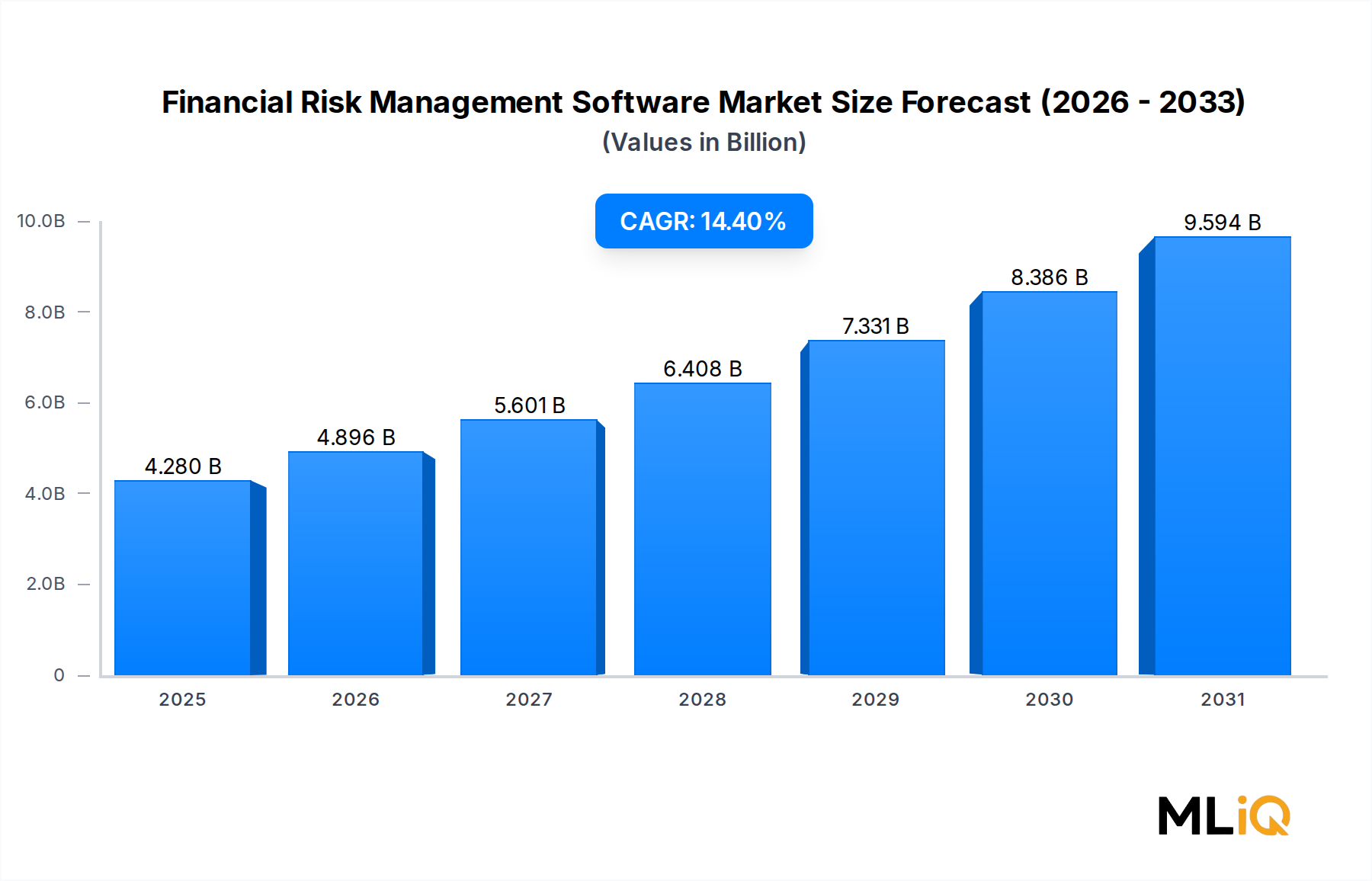

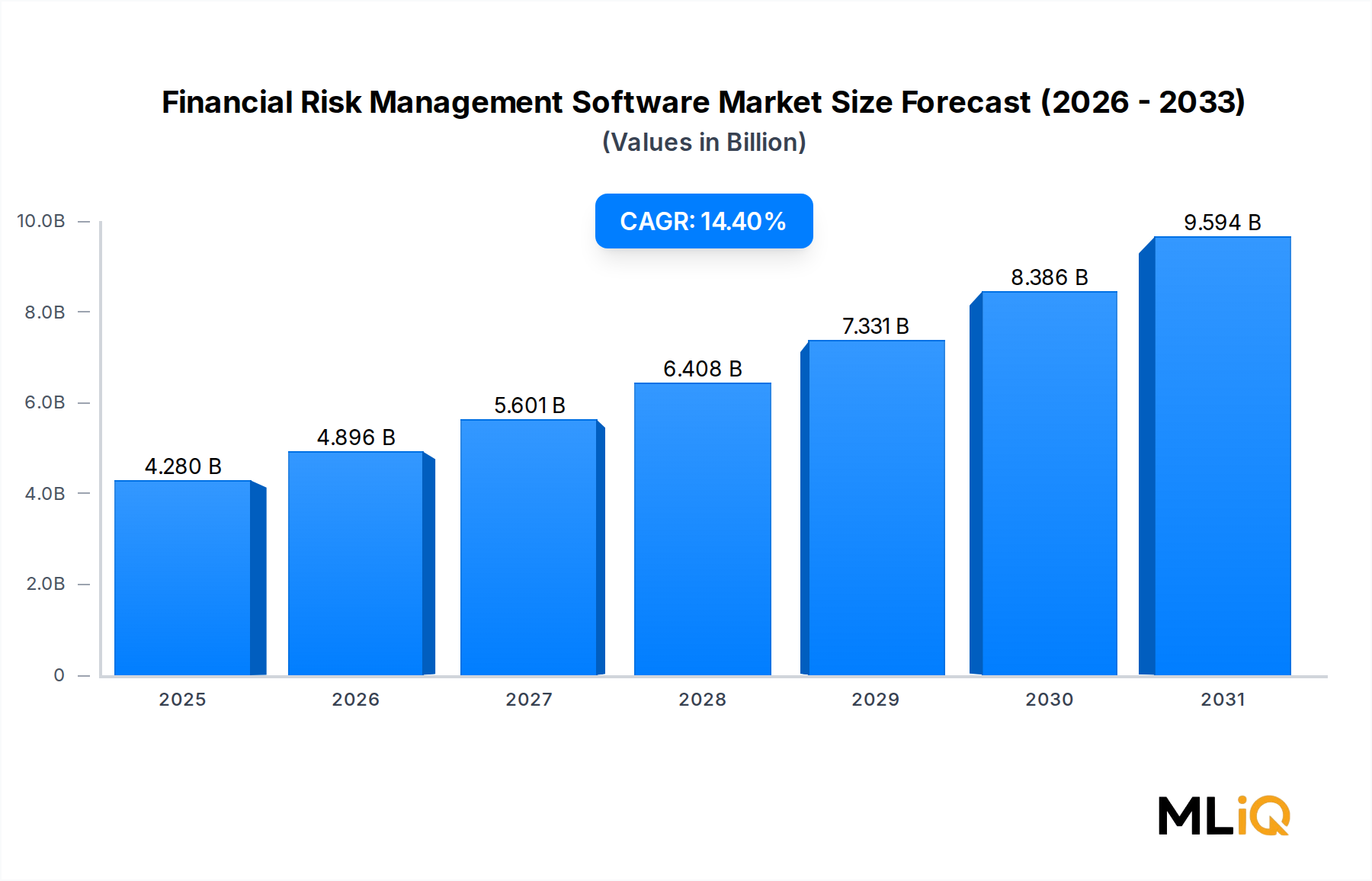

The global Financial Risk Management Software Market is valued at $4.28 billion as of the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 14.4% over the forecast horizon. This robust trajectory positions the market to more than double its current valuation within the next several years, driven by a confluence of regulatory intensification, digital transformation across banking and insurance verticals, and the accelerating adoption of cloud-native architectures across enterprises of all sizes.

At the macro level, several structural forces are amplifying demand. Global financial regulators — including the Basel Committee on Banking Supervision, the Financial Stability Board, and regional authorities across the European Union, the United States, and Asia Pacific — have substantially raised the bar for risk governance, stress testing, and capital adequacy reporting. These mandates compel financial institutions to move beyond legacy, spreadsheet-driven risk management workflows toward automated, auditable, and real-time software platforms. The aftermath of multiple high-profile bank failures and liquidity crises in recent years has further underscored the systemic importance of robust risk infrastructure.

On the technology side, the integration of artificial intelligence, machine learning, and advanced predictive analytics into risk platforms is fundamentally reshaping what organizations can detect, model, and prevent. Modern financial risk software now provides dynamic scenario modeling, counterparty exposure analysis, and portfolio stress testing at a granularity that was computationally prohibitive just a decade ago. This capability expansion is broadening the addressable customer base beyond Tier 1 global banks to include mid-market banks, non-banking financial companies (NBFCs), credit unions, and insurance carriers.

The cloud deployment model is emerging as the dominant growth vector within the market, enabling institutions to reduce total cost of ownership, achieve elastic scalability during peak regulatory reporting cycles, and accelerate time-to-value for new risk modules. Small and medium-sized enterprises (SMEs) in particular are leveraging SaaS-based delivery to access enterprise-grade risk capabilities without the capital expenditure burden historically associated with on-premise deployments.

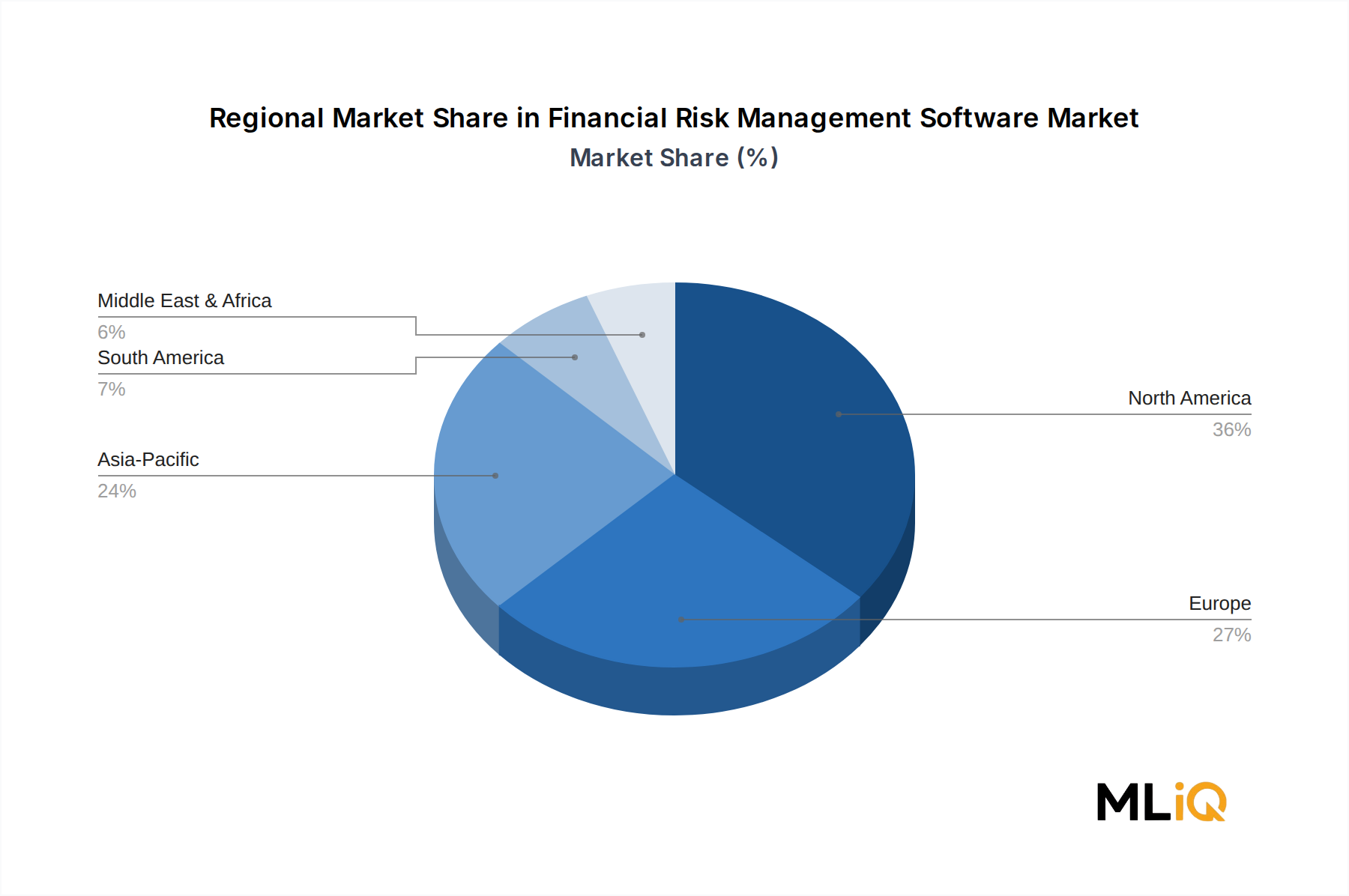

North America currently commands the largest revenue share, underpinned by the density of financial institutions, the stringency of Dodd-Frank and SEC risk disclosure requirements, and the region's mature technology vendor ecosystem. However, Asia Pacific is the fastest-growing region, propelled by rapid financial sector formalization, central bank-driven stress testing mandates in China and India, and widespread adoption of digital banking infrastructure. Europe maintains strong growth momentum driven by Basel IV implementation timelines and DORA (Digital Operational Resilience Act) compliance requirements.

Forward-looking indicators suggest that the convergence of ESG risk integration, geopolitical risk quantification, and real-time liquidity monitoring will define the next competitive frontier. Vendors that can offer a unified, modular, and API-first risk platform will capture disproportionate market share as financial institutions seek to consolidate point solutions into enterprise-wide risk intelligence ecosystems.