Although the Qatar Automotive Lubricants Market is a single-country market, it is instructive to position it within the broader global and GCC regional context to understand relative growth dynamics and trade exposure.

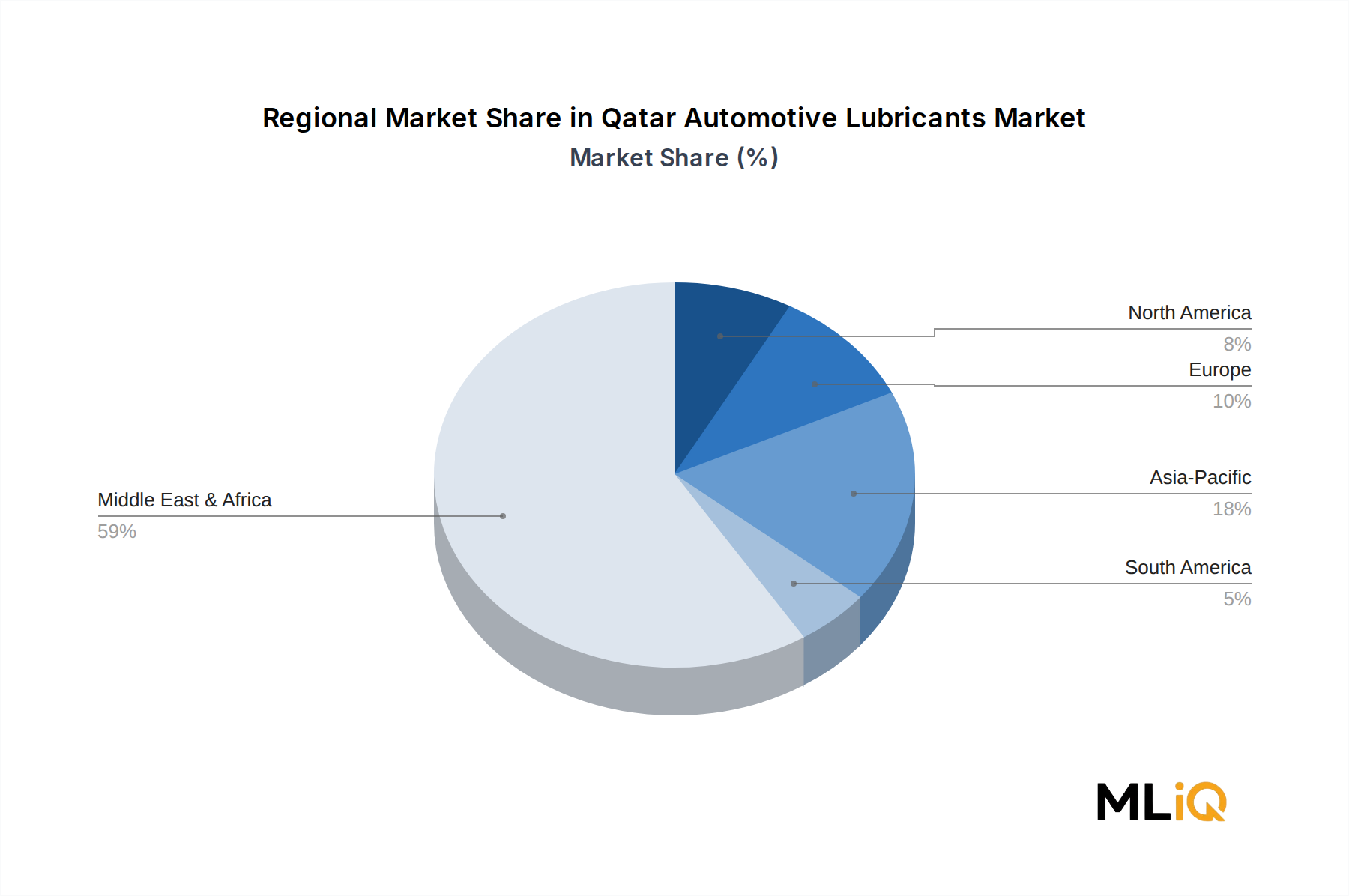

The Middle East & Africa region, within which Qatar operates, is one of the faster-growing lubricant consumption zones globally, driven by high vehicle density per capita, extreme operating temperatures that accelerate oil degradation, and large-scale infrastructure and construction activity. Qatar's market CAGR of 2.98% is broadly in line with GCC averages, though slightly more moderate than high-growth markets in Africa or Southeast Asia. The GCC sub-region benefits from a concentration of premium vehicle fleets, high consumer spending on vehicle maintenance, and a mature distribution infrastructure.

North America represents the most mature global lubricant market, characterized by high synthetic penetration, stringent API and ILSAC specifications, and slower volume growth near 1.5%–2.0% CAGR, as EV adoption and extended drain intervals temper volume expansion. However, it remains the largest absolute revenue market globally, which influences global base oil and additive pricing with downstream effects on Qatar's import costs.

Asia Pacific, led by China, India, and Southeast Asia, is the fastest-growing regional bloc for automotive lubricants globally, with CAGRs in key markets exceeding 4.0%–5.5% driven by rapid motorization, expanding commercial fleets, and urbanization. The Synthetic Lubricants Market is expanding rapidly in this region, creating competitive supply dynamics that benefit importers in markets like Qatar through improved product availability and pricing.

Europe presents a contracting volume outlook as stringent emissions regulations, EV adoption acceleration, and extended drain intervals structurally reduce lubricant demand, with regional CAGRs near 0.5%–1.5%. However, European lubricant technology innovation — particularly in the Lubricant Additives Market — continues to set the performance benchmarks adopted globally, including in Qatar's premium vehicle segment.

South America, particularly Brazil, exhibits moderate growth near 2.5%–3.0% CAGR, driven by a large and aging vehicle fleet with high mineral oil consumption, presenting a contrasting product mix profile versus Qatar's premium-skewed demand.