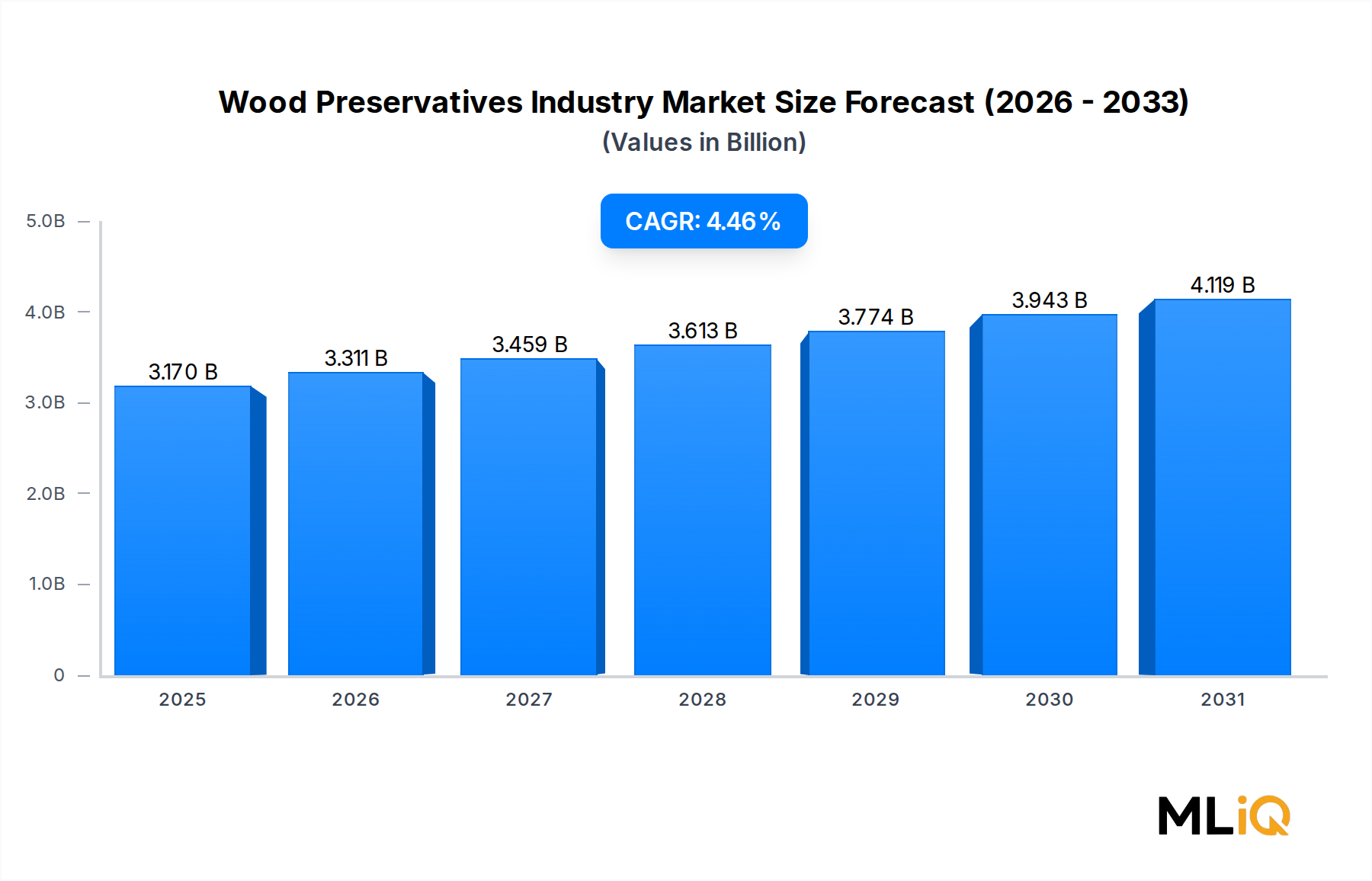

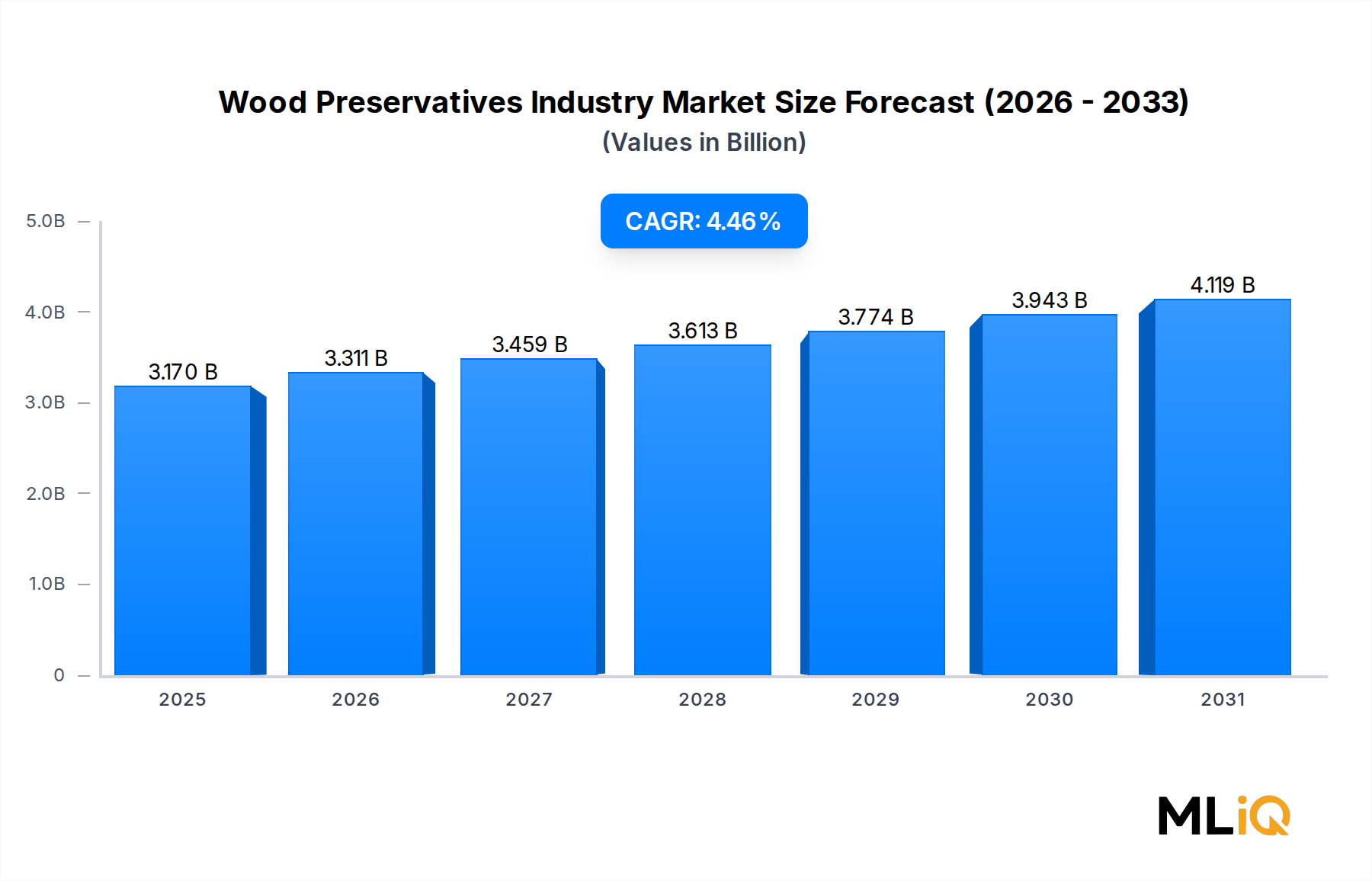

The global Wood Preservatives Industry Market is valued at $3.17 billion as of the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 4.46% over the forecast horizon. This sustained growth trajectory reflects the confluence of rising global construction activity, accelerating furniture manufacturing output, and expanding infrastructure investments across both developed and emerging economies.

The market is fundamentally underpinned by the dual imperatives of extending timber service life and complying with increasingly rigorous building standards. Wood preservatives—spanning water-based, oil-based, and specialty chemical formulations—protect structural and decorative timber against biological degradation caused by fungi, insects, and marine borers. As wood remains a preferred material in residential, commercial, and infrastructural construction due to its cost efficiency, aesthetic properties, and relative sustainability compared to steel and concrete, the demand for effective preservation treatments continues to grow in lockstep.

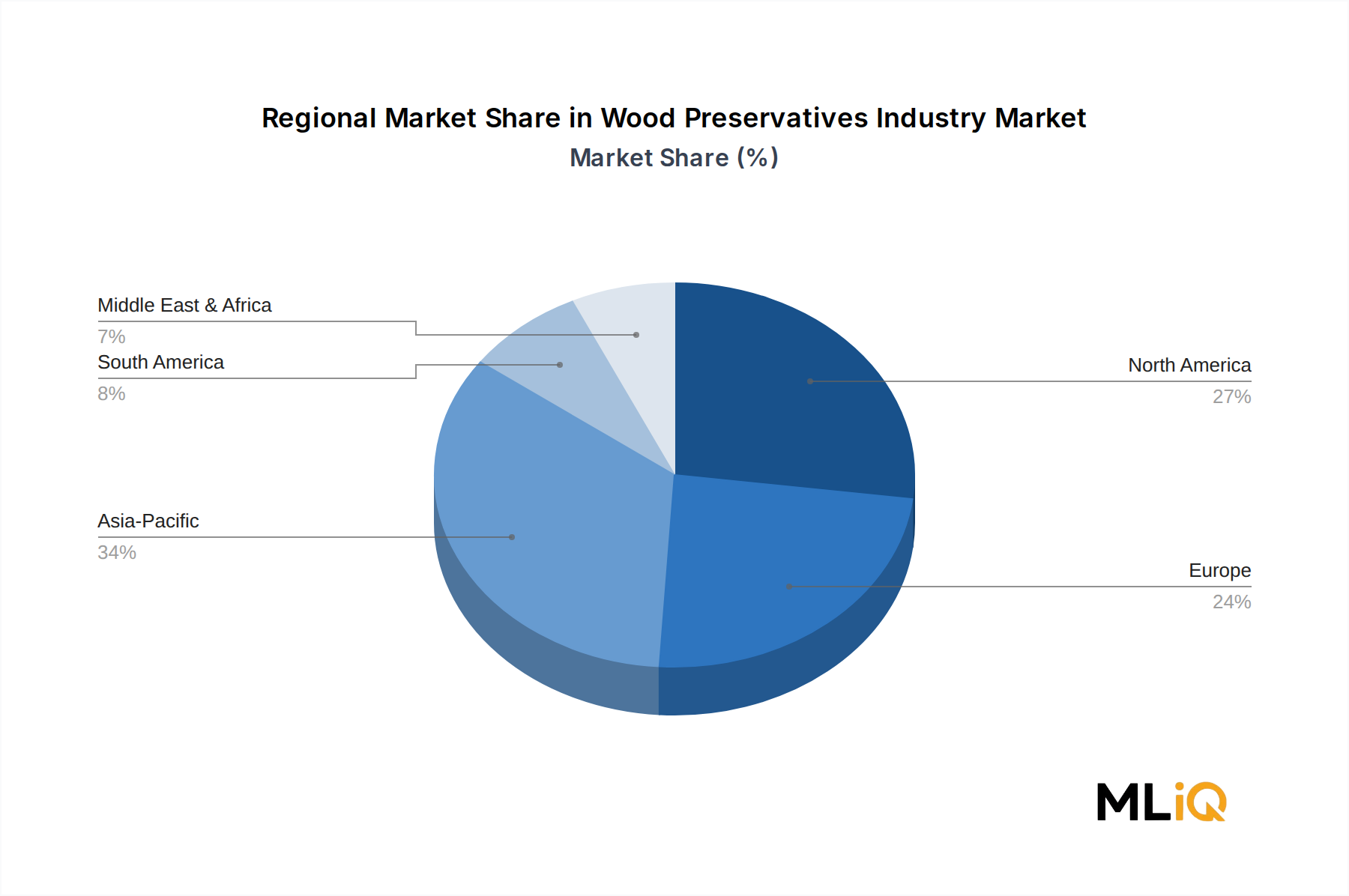

Macro tailwinds driving the market include rapid urbanization in Asia Pacific and Sub-Saharan Africa, which is stimulating housing starts and thereby increasing consumption of treated lumber. In North America and Europe, renovation and retrofit activity in aging building stock is sustaining preservative demand even as new construction rates fluctuate with interest rate cycles. The residential construction sector is identified as the dominant end-use segment, and this dynamic is expected to persist throughout the forecast period.

Additionally, the global push toward sustainable forestry and certified timber (FSC, PEFC) is creating new avenues for preservative chemistries that align with eco-label requirements, opening a premium product tier that commands higher margins. Manufacturers are investing in low-toxicity, bio-based, and waterborne formulations as alternatives to legacy solvent-based systems, responding to both regulatory pressure and procurement preferences from large-scale commercial builders.

The competitive landscape is moderately consolidated, with multinational specialty chemical companies holding significant share alongside regional players offering localized formulation expertise. Strategic mergers and joint ventures—particularly those oriented toward biocide innovation and renewable feedstock integration—are reshaping the supply side of the market.

Looking forward, the Wood Preservatives Industry Market is expected to surpass $4.5 billion by the end of the forecast period, driven by volume growth in Asia Pacific and value growth in Western markets where premium, low-VOC, and REACH-compliant formulations are increasingly mandated. The intersection of environmental regulation, rising wood consumption, and material science innovation positions this market for stable, compounding expansion across all major geographies.