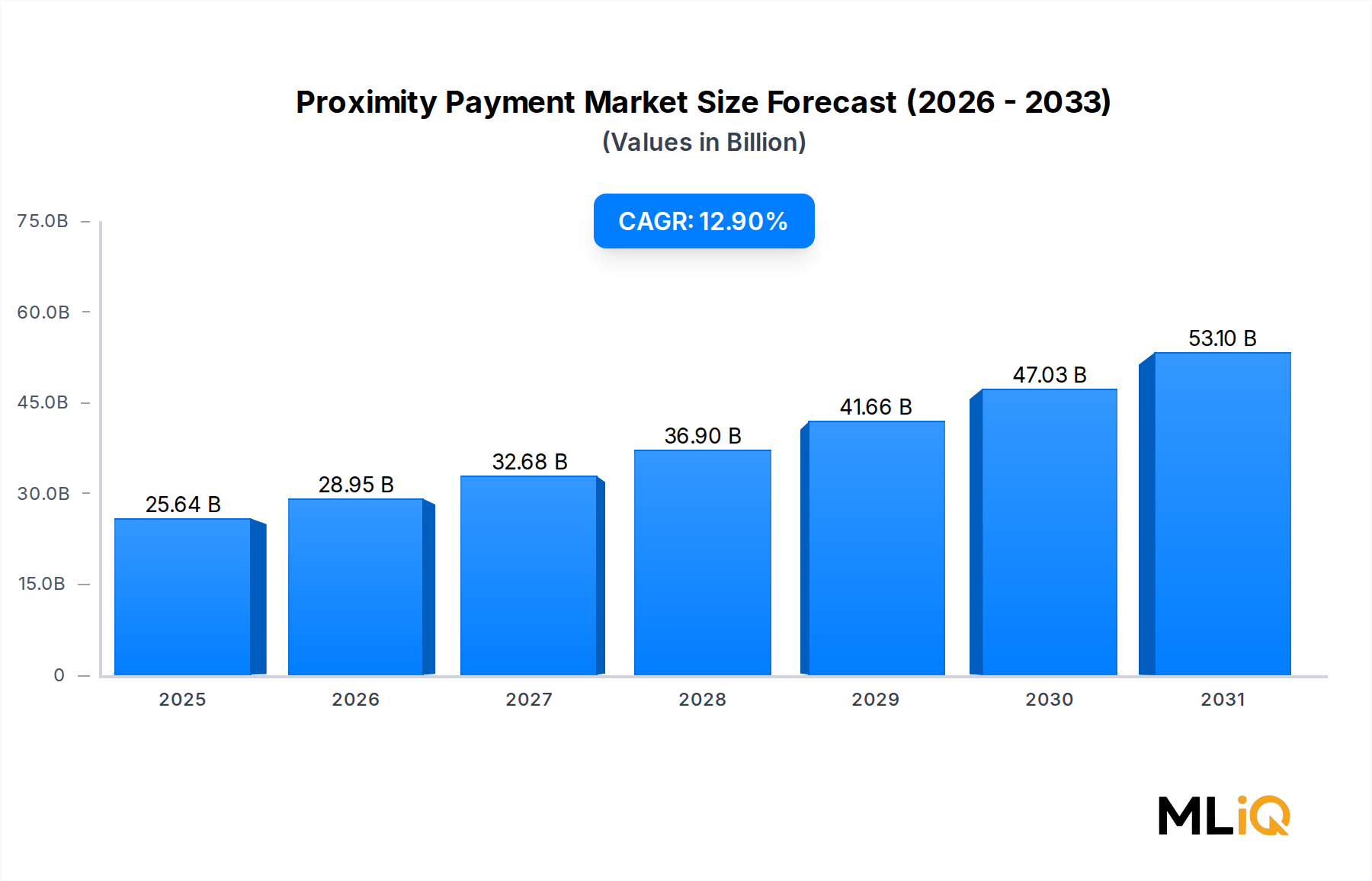

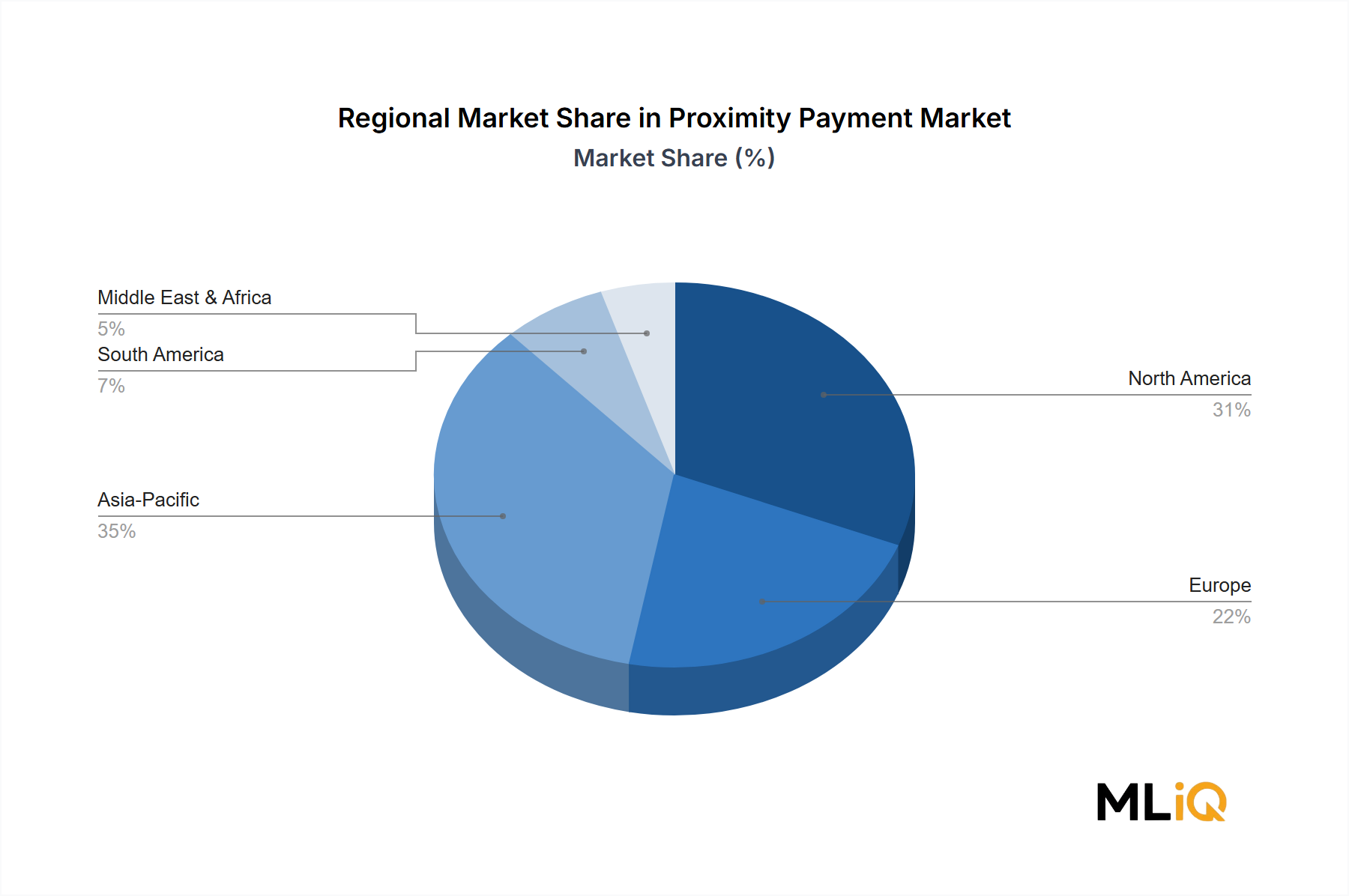

Solution and Service Segment Dominance in the Proximity Payment Market

Within the Proximity Payment Market, the solution and service offering segment represents the single largest revenue-generating category, underpinned by the complex software, middleware, and managed service ecosystems that enable end-to-end contactless transaction processing. This segment encompasses payment gateway software, NFC-enabled terminal management platforms, tokenization engines, fraud detection services, merchant onboarding solutions, and the recurring service contracts that sustain them — all of which generate high-margin, recurring revenue streams for market participants.

The dominance of this segment is rooted in several structural factors. First, the technical complexity of proximity payment infrastructure necessitates ongoing software maintenance, security patch deployment, and compliance updates — particularly as Payment Card Industry Data Security Standard (PCI DSS) requirements evolve. Merchants cannot operate contactless payment infrastructure on a one-time hardware purchase alone; they require continuous integration support, real-time transaction monitoring, and interoperability management across card networks, bank issuers, and device operating systems. This creates deep vendor lock-in and high switching costs, which in turn sustain premium pricing for solution providers.

Second, the proliferation of mobile wallet ecosystems — most notably Apple Pay, Google Pay, and Samsung Pay — has generated a parallel demand surge for back-end tokenization and authentication services. Every proximity payment transaction initiated through a mobile wallet requires the real-time exchange of device-specific tokens with issuing banks, card networks, and merchant acquirers, all of which must be orchestrated by software platforms operating at millisecond latency. Companies such as Visa Inc and Mastercard have invested heavily in their tokenization service infrastructure, positioning it as a core revenue lever within the solution and service segment.

Third, the enterprise and SME merchant segments have increasingly shifted toward software-as-a-service (SaaS) models for payment acceptance, driving recurring revenue recognition rather than episodic hardware sales. Providers such as FIS, ACI Worldwide, and INGENICO have restructured their product portfolios to prioritize cloud-hosted payment orchestration platforms that bundle proximity payment capability with broader omnichannel commerce management, data analytics, and working capital financing tools.

The solution and service segment's revenue share is not merely holding steady — it is actively expanding as a proportion of total market value. Hardware commoditization, driven by competitive pricing pressure on NFC terminal manufacturing and the widespread adoption of software-defined point-of-sale systems running on commercial-off-the-shelf tablets and smartphones, has shifted value creation decisively toward the software and services layer. Gross margins in the solution and service segment routinely exceed 40–60% for established platform providers, compared to 10–20% margins typical of hardware-centric competitors.

Key players driving this segment's growth include PayPal Holdings Inc, which has built a comprehensive merchant services ecosystem layered atop proximity payment rails; FIS, which operates one of the largest payment processing networks globally; and IDEMIA, which specializes in secure element technology and identity-linked payment services. The segment is expected to maintain its dominant position throughout the 2025–2033 forecast period, with SaaS transition momentum and API-driven payment infrastructure adoption serving as the primary growth accelerants.