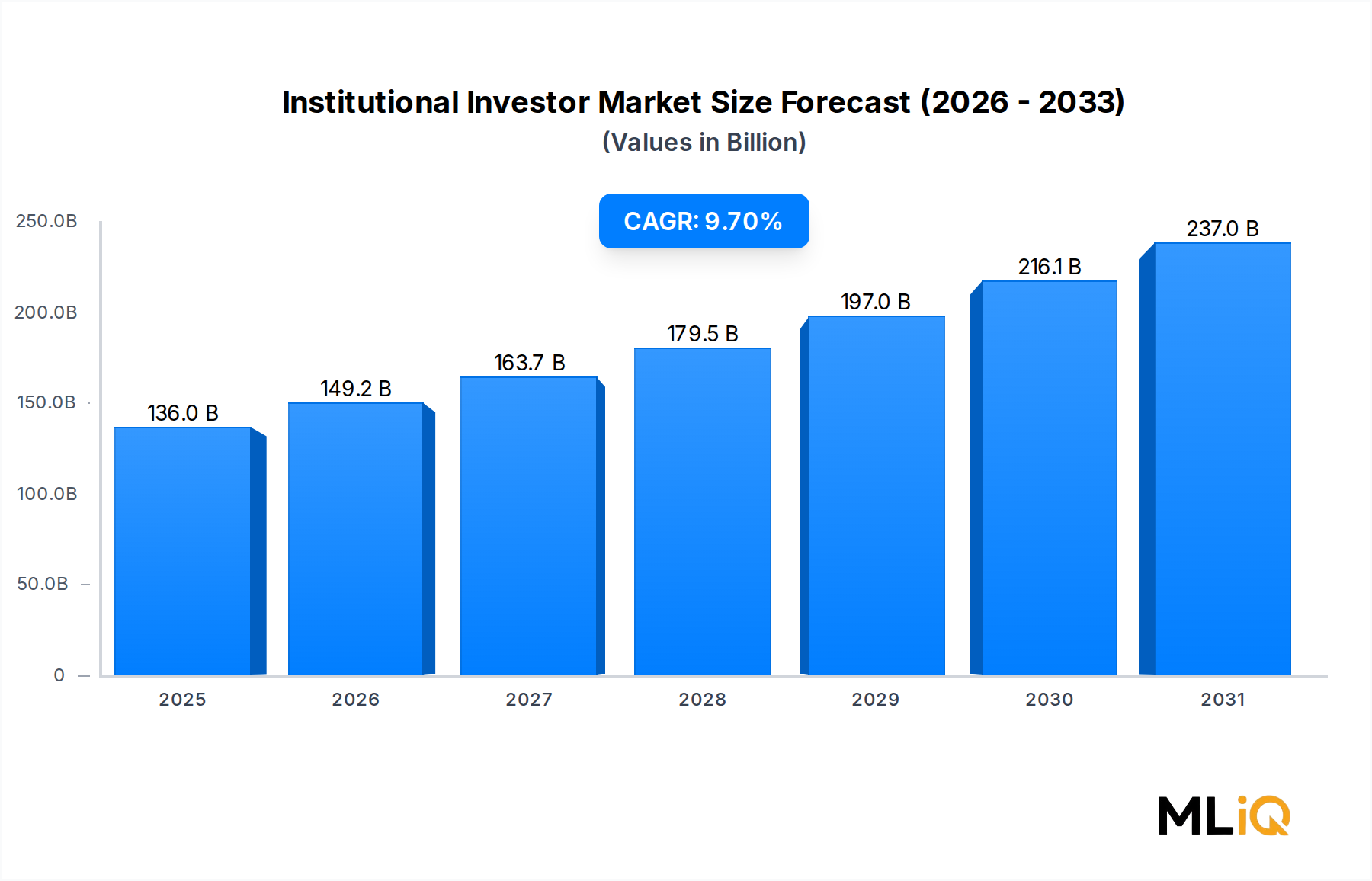

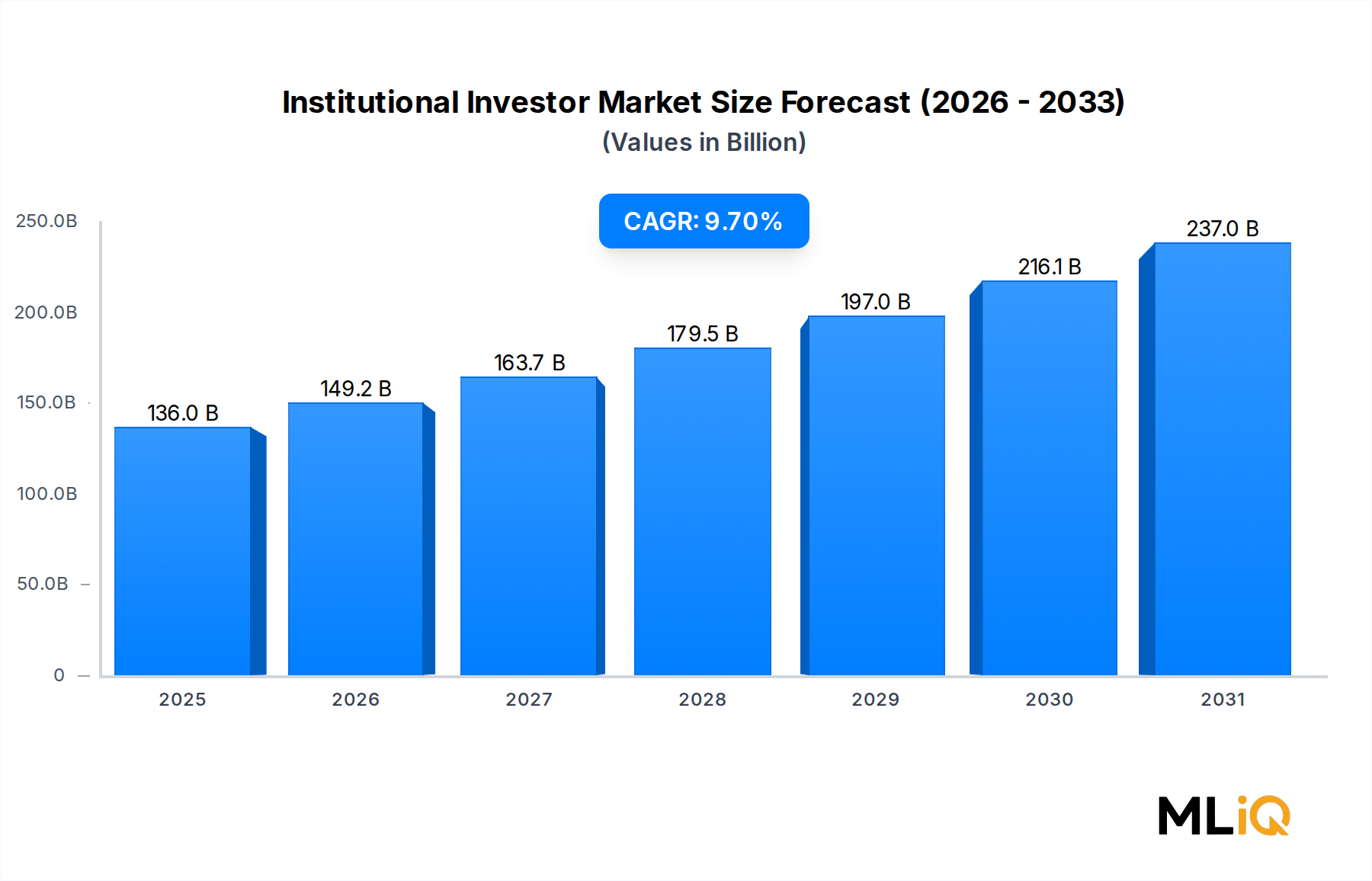

Mutual Fund Dominance and Segment Leadership in the Institutional Investor Market

Among all segments within the Institutional Investor Market, the Mutual Fund segment commands the largest share of revenue and assets under management globally. This dominance is attributable to several structural factors: regulatory familiarity, retail-to-institutional crossover demand, liquidity advantages, and the sheer scale of mutual fund operations across North America, Europe, and Asia Pacific.

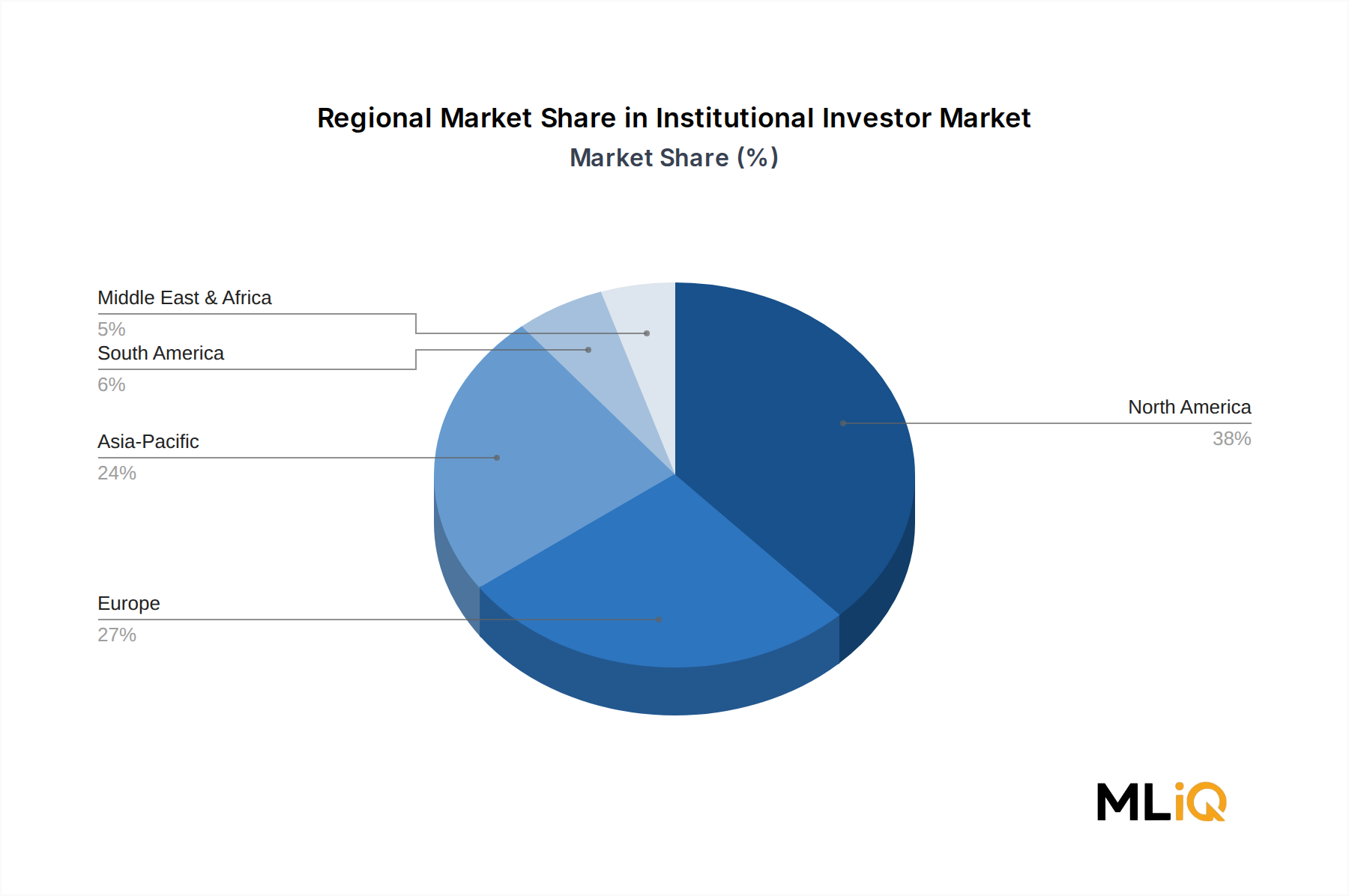

Mutual funds serve as the primary investment vehicle for a wide spectrum of institutional actors — including insurance companies, pension schemes, and corporate treasuries — that require liquid, diversified, and cost-efficient exposure to equity, fixed income, and multi-asset class portfolios. The segment benefits from deep regulatory infrastructure in the United States (governed by the Investment Company Act of 1940), the UCITS framework in Europe, and equivalent frameworks across Asia Pacific jurisdictions.

As of 2024, mutual funds collectively manage an estimated $63 trillion in global assets, representing the single largest pool of institutionally managed capital. The segment's growth is being driven by passive investment strategies, including index-tracking and ETF-adjacent structures, which have gained significant traction among cost-conscious institutional allocators. Fee compression — a defining feature of the past decade — has paradoxically accelerated AUM growth by lowering barriers to entry and increasing adoption among mid-tier institutional investors.

The Mutual Fund Market is deeply relevant here, as it forms the foundational layer upon which broader institutional capital allocation strategies are built. Active management within mutual funds is experiencing a bifurcation: traditional active managers are losing share to passive vehicles, while thematic and factor-based active strategies are attracting net new institutional flows.

Key players in the mutual fund segment include vertically integrated asset managers such as BlackRock, Vanguard, Fidelity Investments, and Amundi, each of which operates mutual fund platforms spanning multiple jurisdictions. These firms leverage economies of scale, proprietary research infrastructure, and distribution networks to maintain competitive moats.

The segment is also experiencing meaningful consolidation. Smaller boutique fund managers are either being acquired by larger platforms seeking distribution breadth or are pivoting toward niche strategies — such as ESG-screened equity, infrastructure debt, or climate transition funds — that command premium fees and attract mission-driven institutional capital.

Within the Institutional Investor Market, mutual funds are further segmented by asset class (equity, fixed income, money market, balanced/hybrid, and alternatives) and by investor type (retail-institutional hybrids vs. pure institutional). The institutional share class structures — characterized by lower expense ratios and higher minimum investment thresholds — are growing faster than retail equivalents, reflecting the increasing sophistication and scale of institutional allocators.

Looking forward, the mutual fund segment is expected to maintain its dominant position, even as hedge funds and private equity vehicles attract disproportionate media and regulatory attention. The combination of liquidity, regulatory compliance, and global distribution infrastructure ensures that mutual funds will remain the preferred vehicle for institutional capital deployment across the forecast period of 2025–2033.