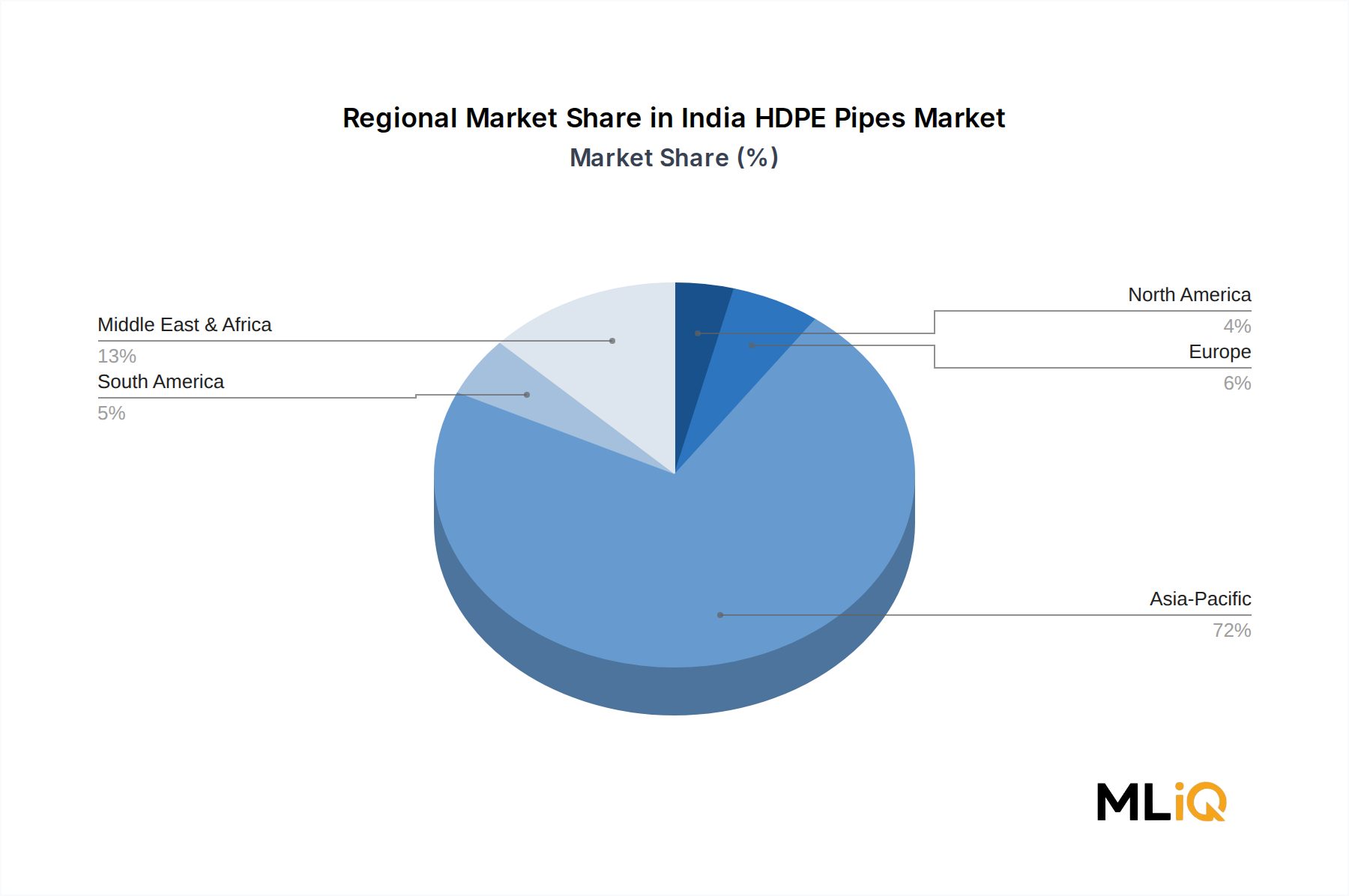

The India HDPE Pipes Market exhibits pronounced regional differentiation driven by infrastructure investment patterns, agricultural activity, and urbanization rates across the country's diverse geographies.

North India (Uttar Pradesh, Punjab, Haryana, Rajasthan): This region represents the largest absolute revenue contributor to the India HDPE Pipes Market, accounting for an estimated 32%–35% of national demand. The primary drivers are large-scale Jal Jeevan Mission implementation across densely populated rural districts, agricultural canal modernization in the Indo-Gangetic plain, and the rapid expansion of city gas distribution networks in UPCL and GAIL-served zones. State-level procurement volumes in Uttar Pradesh alone — driven by its population of over 240 million — create a structural demand base that no other state can match.

West India (Maharashtra, Gujarat): The western region is the second-largest market, driven by industrial HDPE pipe demand in chemical processing clusters (Dahej, Surat, Pune), municipal water supply augmentation in the Mumbai Metropolitan Region, and agricultural drip irrigation adoption in Maharashtra's horticulture belt. Gujarat's petrochemical industry proximity to HDPE resin production also enables regional manufacturers to access competitively priced feedstock. This region's CAGR is estimated at 10.5%–11.0%, broadly in line with the national average.

South India (Karnataka, Andhra Pradesh, Tamil Nadu, Telangana): The southern region is the fastest-growing in percentage terms, with an estimated regional CAGR of 12.0%–13.5%, supported by aggressive BharatNet fiber rollout, robust IT-driven urban construction in Bengaluru and Hyderabad, and large-scale irrigation infrastructure investment in Andhra Pradesh's Polavaram project and related canal systems. The south is also a key hub for HDPE pipe manufacturers serving the Water Infrastructure Market and the Underground Cable Ducting Market.

East India (West Bengal, Odisha, Bihar, Jharkhand): The eastern region is the least penetrated but offers the highest latent upside. Low baseline infrastructure density, combined with increasing central government allocations under schemes like AMRUT 2.0 and Jal Jeevan Mission, positions the east for above-average growth over the medium term. Current market share is estimated at 12%–15%, with a CAGR potential of 13%–14% if government disbursements are executed on schedule.

Central India (Madhya Pradesh, Chhattisgarh): A mid-sized market with steady growth anchored in agricultural irrigation and mining-sector industrial piping applications. Regional CAGR is estimated at 9.5%–10.5%, slightly below the national average due to lower urbanization rates and project execution capacity constraints.