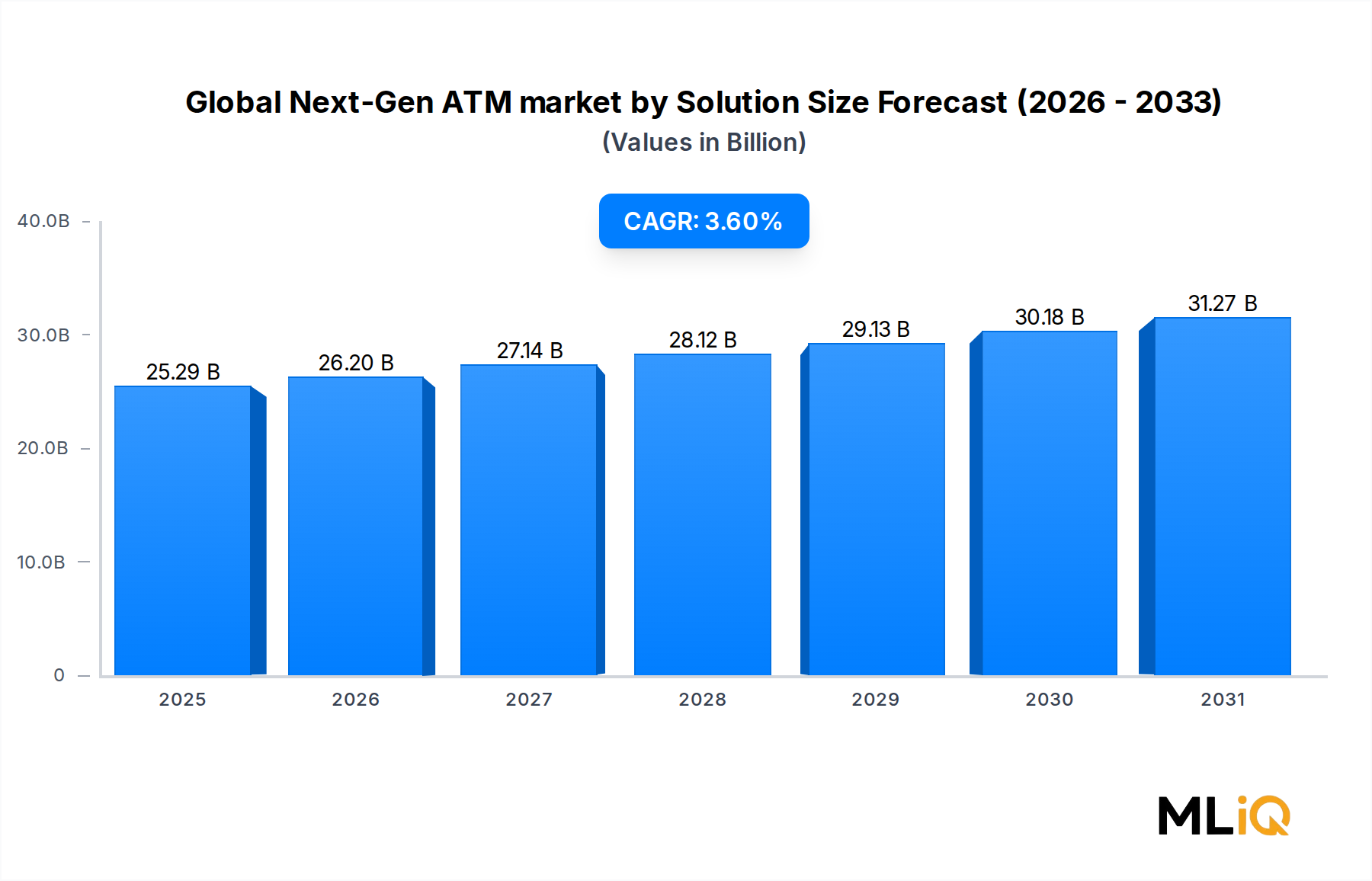

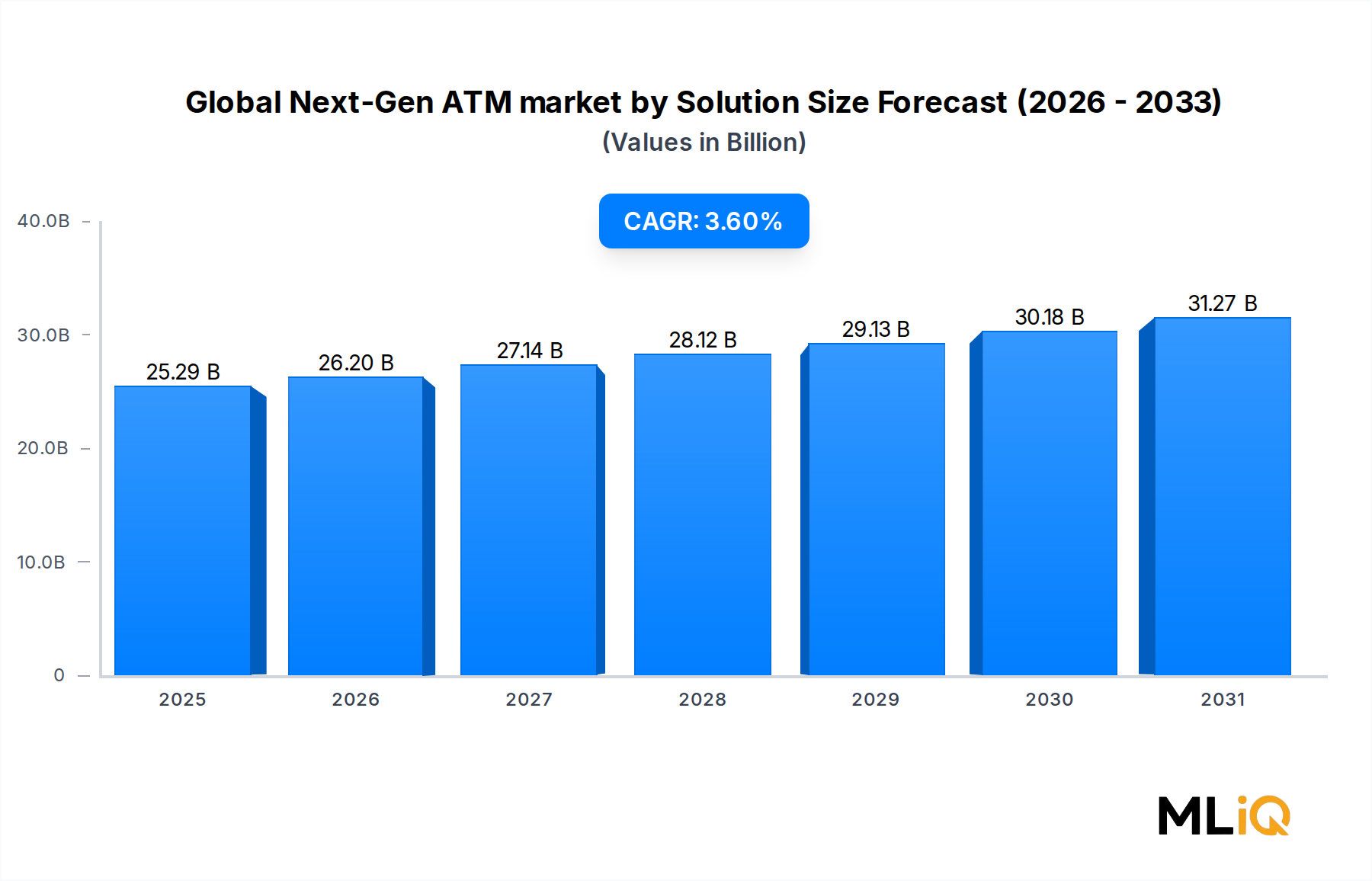

Deployment Solutions Dominance in the Global Next-Gen ATM Market by Solution

Within the solution segmentation of the Global Next-Gen ATM market by Solution, the Deployment segment commands the largest revenue share, underpinned by persistent hardware refresh cycles, expanding ATM network footprints in emerging markets, and the technological imperative to replace legacy units incapable of supporting modern security protocols, contactless transactions, and cloud integration.

Deployment encompasses the design, installation, configuration, and commissioning of next-generation ATM hardware across bank-owned, white-label, and brown-label models. It spans a broad product taxonomy including Smart ATMs, Cash Dispenser ATMs, Through-the-Wall ATMs, Free-Standing ATMs, Solar Powered ATMs, Self-Cashed ATMs, and Brown and White Label variants, each addressing distinct geographic, operational, and customer service contexts.

Smart ATMs represent the highest-value subsegment within Deployment, integrating multifunction capabilities such as cardless transactions via QR code or NFC, biometric authentication, envelope-free deposits, real-time fraud scoring, and remote diagnostic connectivity. These units command a significant price premium over conventional models, elevating average revenue per deployment and skewing segment mix toward higher-margin configurations.

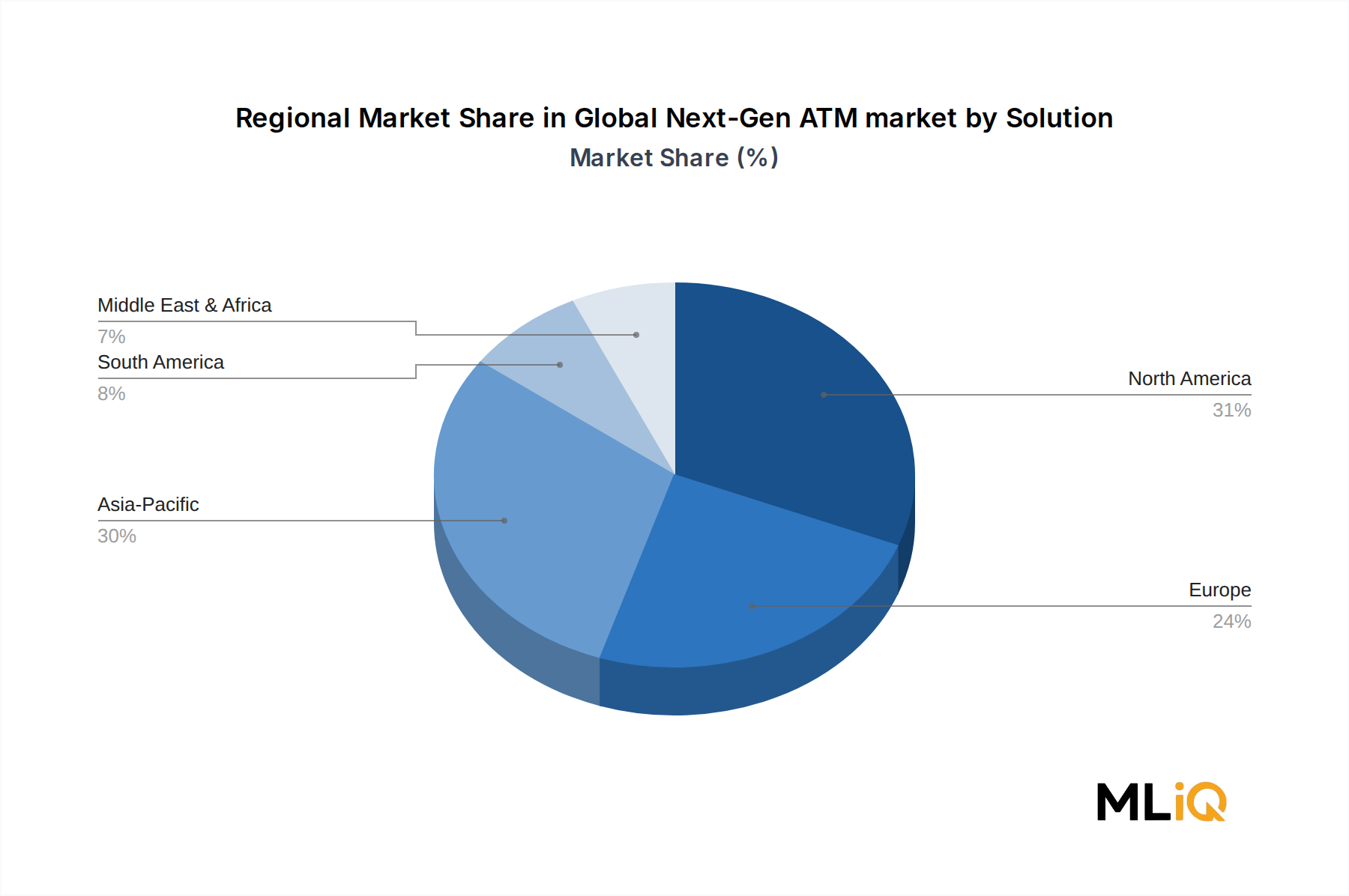

Geographically, the Deployment segment is strongest in Asia Pacific, where China and India are executing large-scale network modernization programs. India's push toward financial inclusion under regulatory frameworks has catalyzed deployment of white-label ATMs in semi-urban and rural districts, with independent ATM deployers partnering with public sector banks to serve underbanked populations. China's state-owned banking sector is simultaneously upgrading urban ATM estates with AI-enhanced interfaces and multi-modal authentication.

In North America and Europe, Deployment activity is characterized more by replacement than net expansion — retiring aging infrastructure that lacks EMV compliance, contactless payment capability, or cybersecurity hardening. Regulatory mandates around PCI DSS compliance and accessibility standards (ADA in the US, EN 301 549 in Europe) are creating non-discretionary refresh cycles that sustain deployment revenue regardless of broader network contraction trends.

Key players anchoring the Deployment segment include NCR Corporation, which maintains one of the broadest global ATM hardware portfolios spanning multifunction and cash recycling units; Diebold Nixdorf (formed through the merger of DIEBOLD INC and Wincor Nixdorf AG), which serves major financial institutions across the Americas and Europe; Nautilus Hyosung, a dominant force in North American retail and financial ATM deployments; GRG Banking, which leads in Asia Pacific with cost-competitive smart ATM platforms; and Fujitsu, whose recycler-based ATM technology holds significant share in Japan and select European markets.

The Deployment segment's dominance is gradually consolidating rather than expanding its revenue share differential over Managed Services. As ATM networks mature in developed markets and operational outsourcing grows, Managed Services is narrowing the gap. However, in absolute terms, Deployment retains primacy through 2033 due to the volume and value of hardware programs in Asia Pacific, the Middle East, and Africa. The shift toward modular, software-defined ATM architectures is extending unit lifespans through hardware upgrades rather than full replacements, adding a nuanced dynamic — reducing pure replacement cycles while creating upgrade-led deployment revenues.

Vendors differentiating within Deployment are investing in open platform ATM architectures, enabling financial institutions to run third-party applications and integrate with digital banking ecosystems. This positions Deployment not merely as a hardware sale but as the foundation of a broader platform engagement, reinforcing long-term customer relationships and enabling cross-sell into managed services contracts.