1. What are the major growth drivers for the Dinotefuran Market market?

Factors such as are projected to boost the Dinotefuran Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

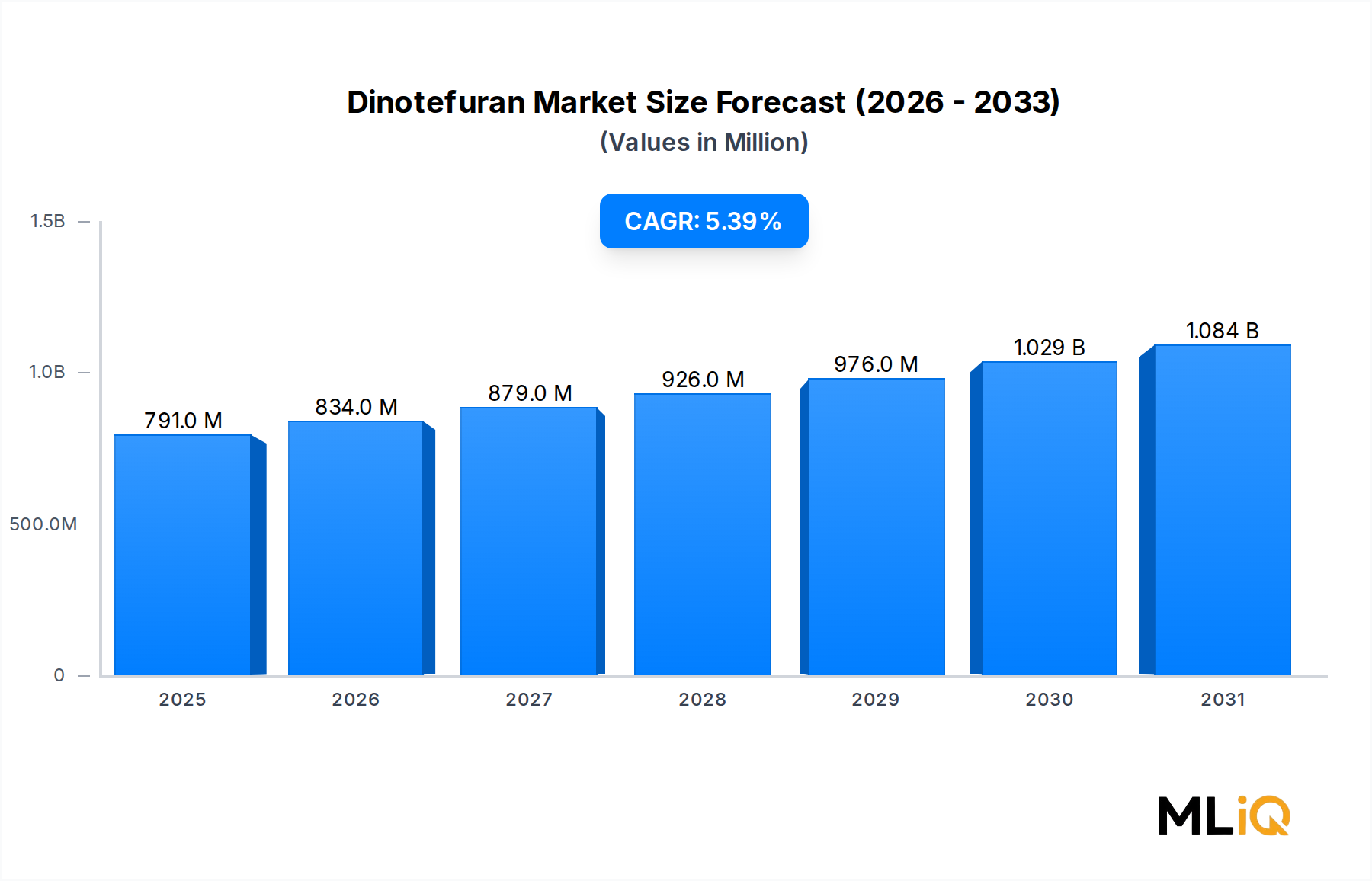

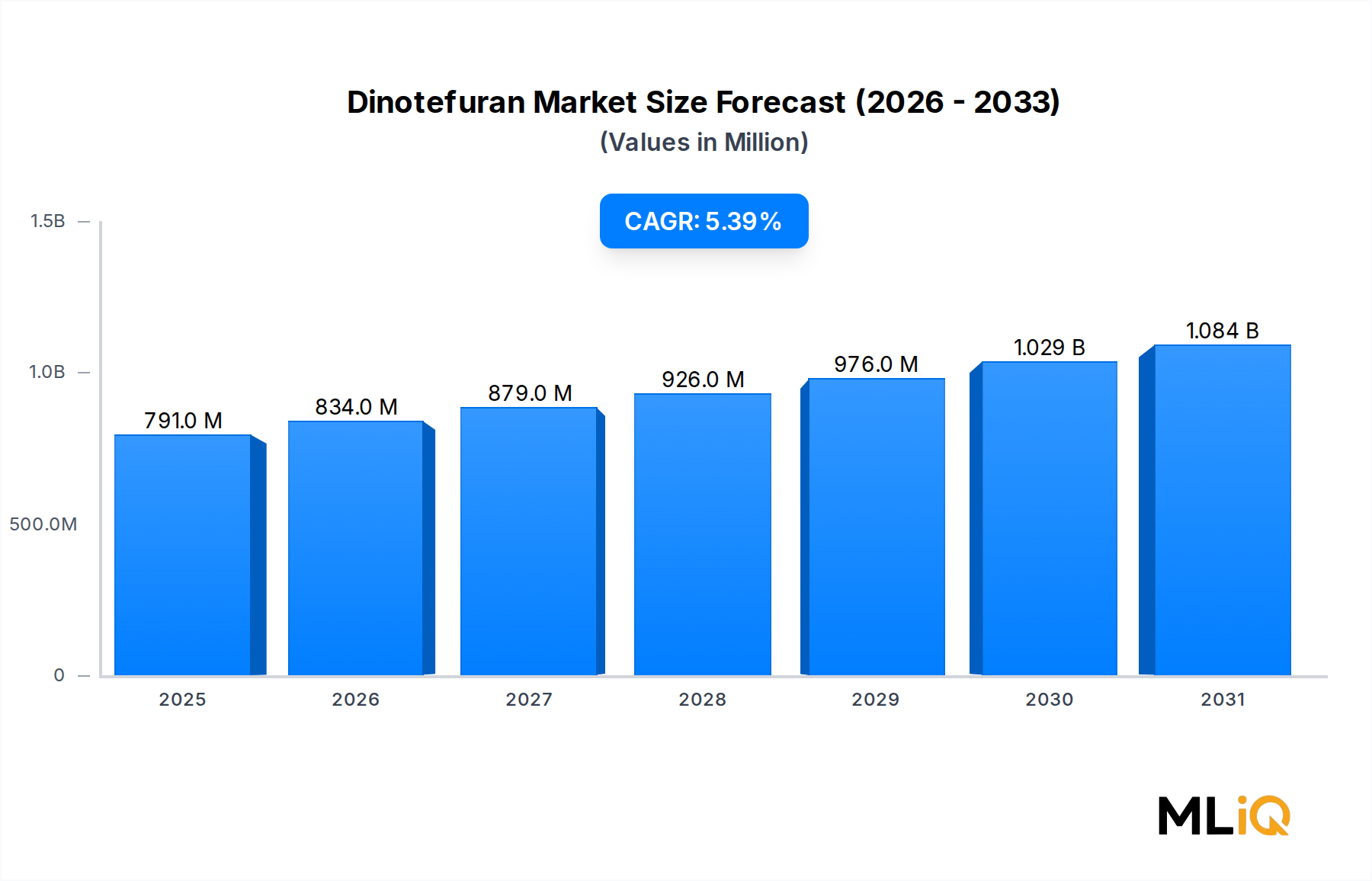

The global Dinotefuran Market was valued at $790.96 million in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 5.4% through the forecast horizon, underpinned by escalating demand for third-generation neonicotinoid insecticides across crop protection, urban pest management, and turf care applications. Dinotefuran, a nitromethylene neonicotinoid first developed by Mitsui Chemicals, distinguishes itself from earlier neonicotinoid generations through rapid systemic translocation, broad-spectrum efficacy against sucking and chewing insects, and a comparatively favorable mammalian toxicity profile, positioning it as a preferred active ingredient in integrated pest management (IPM) protocols worldwide.

Key demand drivers include the accelerating resistance of major insect vectors—including whiteflies, aphids, and soil-dwelling grubs—to organophosphate and pyrethroid chemistries, compelling growers and pest management professionals to adopt next-generation actives such as dinotefuran. The compound's dual systemic and contact action enables effective control in both foliar and soil-drench formulations, which broadens its addressable market across crop fields, residential and commercial buildings, turf farms, and ornamental plant segments. Rising global food security concerns, driven by population growth projected to reach 9.7 billion by 2050, are intensifying pressure on arable yield protection, directly amplifying agrochemical consumption volumes.

Macro tailwinds reinforcing market expansion include the regulatory phase-out of several older-generation organochlorine and carbamate insecticides across the European Union and North American markets, creating structural substitution opportunities for approved neonicotinoids with refined environmental risk assessments. Simultaneously, the rapid urbanization across Asia Pacific and Latin America is stimulating demand in the non-agricultural pest control segment, where dinotefuran-based spot treatments and bait formulations are increasingly deployed in residential buildings, commercial complexes, and public health vector programs.

From a forward-looking perspective, innovation in formulation technology—particularly microencapsulation and controlled-release granules—is expected to extend field efficacy windows, reduce application frequency, and mitigate off-target exposure concerns, thereby supporting regulatory approvals in environmentally sensitive markets. The emergence of precision agriculture platforms integrating drone-based foliar applications is also widening dinotefuran's deployment envelope, particularly in high-value horticultural crops. Collectively, these dynamics position the Dinotefuran Market for sustained mid-single-digit growth, with the Asia Pacific region and Latin America serving as primary volume growth engines through the forecast period.

Among all application segments analyzed, crop fields constitute the single largest revenue-generating segment within the Dinotefuran Market, accounting for an estimated majority share of total market revenue in 2024. This dominance is attributable to a convergence of agronomic, regulatory, and economic factors that structurally favor dinotefuran adoption across a diverse array of commercial crops including rice, vegetables, fruits, cotton, soybeans, and cereals.

The systemic nature of dinotefuran—absorbed through roots and foliage and translocated throughout plant vascular tissue—renders it exceptionally effective against phloem-feeding insects such as aphids, thrips, whiteflies, and leafhoppers, which are among the most economically destructive pest complexes in global agriculture. These pest guilds are responsible for both direct crop damage through sap extraction and indirect losses via vectoring plant viruses such as Tomato Yellow Leaf Curl Virus (TYLCV) and Cucurbit Yellow Stunting Disorder Virus (CYSDV), conditions that can reduce marketable yields by 30–60% in susceptible cultivars. The compound's translaminar movement also ensures coverage of cryptic pests sheltering on the underside of foliage, a limitation that hampers surface-contact insecticides.

Rice cultivation across Asia Pacific represents a particularly significant demand node. Dinotefuran's water-soluble profile makes it highly compatible with paddy field application via soil incorporation and nursery box treatments, targeting the brown planthopper (Nilaparvata lugens), which has historically devastated rice harvests across Japan, South Korea, Vietnam, and China. Japan, where dinotefuran was originally commercialized under the trade name Starkle by Mitsui Chemical Agro, Inc, remains a leading per-hectare consumption market for the active ingredient within the rice segment.

In vegetable and fruit production systems, particularly under greenhouse cultivation, dinotefuran is increasingly applied as a drench or substrate incorporation treatment, offering systemic protection without the foliar residue concerns associated with spray applications. This mode of delivery is gaining traction among fresh produce exporters subject to stringent maximum residue limit (MRL) compliance requirements in destination markets.

Key players maintaining dominant positions within the crop field application segment include Mitsui Chemical Agro, Inc, which retains strong intellectual property positions in Japan and select Asian markets; Arysta Lifescience, which distributes dinotefuran-based crop protection products across multiple geographies; and Gowan Company Llc, which has expanded its dinotefuran portfolio in the North American specialty and vegetable crop segments. Chinese manufacturers, including Jinan Great Chemical Industry Co, Ltd, are intensifying competitive pressure through cost-optimized technical-grade dinotefuran supply chains targeting price-sensitive developing markets.

The crop field segment's revenue share appears to be consolidating rather than expanding proportionally, as non-agricultural pest control applications—particularly in residential and commercial buildings and turf farms—are growing at above-average rates within the overall market. Nevertheless, the absolute volume consumed in crop fields remains unrivaled, and the ongoing development of resistance management programs that incorporate dinotefuran rotations alongside other insecticide classes ensures that crop-oriented demand will underpin total market revenue for the foreseeable future.

Formulation innovation is a critical competitive axis within this segment. Suspension concentrates (SC), wettable granules (WG), and water-dispersible granules (WDG) are the dominant forms, while emulsifiable concentrates (EC) are being supplanted by safer aqueous formulations in response to applicator safety regulations across the European Union and North America.

Several quantifiable drivers are propelling growth in the Dinotefuran Market, alongside a set of regulatory and environmental constraints that modulate the pace of expansion.

Resistance escalation to legacy insecticides is the primary structural driver. Independent studies published in the Journal of Economic Entomology and Pest Management Science have documented resistance ratios exceeding 500-fold in whitefly (Bemisia tabaci) populations against imidacloprid, one of the older first-generation neonicotinoids, in Mediterranean and Asian growing regions. This resistance landscape creates a direct commercial pathway for dinotefuran, which exhibits a distinct binding profile to nicotinic acetylcholine receptors (nAChR) that partially circumvents existing resistance mechanisms.

Urbanization and the associated demand for pest control in non-agricultural settings represent a second major quantitative driver. According to United Nations data, 56% of the global population resided in urban areas as of 2024, a figure projected to rise to 68% by 2050. This demographic trend is directly correlated with growth in the Pest Control Services Market, which relies on professional-grade insecticides including dinotefuran for structural and perimeter pest management.

Climate change is amplifying pest pressure globally. Rising mean temperatures are expanding the geographic range of tropical pest species, increasing overwintering survival rates, and compressing pest generation times, all of which translate to higher insecticide application frequency and volume. This dynamic is particularly evident in markets such as Europe and the northern United States, where historically temperate conditions previously limited pest establishment.

On the constraint side, regulatory scrutiny of neonicotinoids as a class represents the most significant headwind. The European Union's 2018 moratorium on outdoor use of imidacloprid, clothianidin, and thiamethoxam, based on evidence of harm to pollinators, has cast a long regulatory shadow over the entire neonicotinoid class, including dinotefuran. While dinotefuran has not faced equivalent blanket restrictions, regulatory review processes in the EU and United Kingdom are intensifying, creating market access uncertainty. Additionally, groundwater contamination concerns linked to dinotefuran's high water solubility (solubility: 39.83 g/L at 20°C) are prompting scrutiny from environmental agencies in Japan, the United States, and Australia.

The competitive landscape of the Dinotefuran Market is characterized by a mix of originator companies, multinational agrochemical distributors, specialty chemical suppliers, and cost-competitive Chinese generic manufacturers. The following profiles outline the strategic positioning of key participants:

Arysta Lifescience: A major multinational with extensive crop protection and non-crop pest management portfolios, Arysta Lifescience distributes dinotefuran-based formulations across Asia Pacific, Latin America, and North America, leveraging its established agrochemical distribution networks.

Mitsui Chemical Agro, Inc: As the originator and primary intellectual property holder of dinotefuran, Mitsui Chemical Agro, Inc maintains a commanding presence in the Japanese domestic market and holds licensing arrangements in key Asian markets, positioning the company as the technical standard-setter for active ingredient quality.

Agnova Technology Pty Ltd: An Australian specialty agrochemical company, Agnova Technology Pty Ltd focuses on high-value horticulture, turf, and ornamental plant segments within the Oceania region, offering dinotefuran formulations tailored to local regulatory frameworks and pest complexes.

Aurum Pharmatech Llc: Operating as a fine chemical and reference standard supplier, Aurum Pharmatech Llc serves research and analytical laboratories requiring certified dinotefuran standards for residue testing, regulatory submission, and method development applications.

Gowan Company Llc: A privately held specialty crop protection company based in North America, Gowan Company Llc has built a strong dinotefuran distribution presence in specialty crop, ornamental, and turf markets in the United States, particularly through its Venom and Safari branded product lines.

Chemodex Ltd: A European specialty chemicals supplier, Chemodex Ltd provides dinotefuran as a research-grade and technical-grade compound to academic institutions, contract research organizations, and registration dossier compilers across Europe.

Awiner Biotech: A Chinese agrochemical manufacturer, Awiner Biotech supplies dinotefuran technical-grade active ingredient and formulated products to domestic and export markets, competing on cost efficiency and flexible minimum order quantities.

Sigma-Aldrich Co. Llc: A subsidiary of Merck KGaA, Sigma-Aldrich Co. Llc distributes dinotefuran as a certified analytical reference standard for laboratory applications, supporting global pesticide residue monitoring programs and food safety compliance testing.

Jinan Great Chemical Industry Co, Ltd: A Chinese technical-grade manufacturer, Jinan Great Chemical Industry Co, Ltd competes on price-per-kilogram in the bulk active ingredient market, supplying both domestic formulators and international trading houses.

March 2023: The United States Environmental Protection Agency (EPA) completed a registration review of dinotefuran, reaffirming its registration status for agricultural and non-agricultural uses while imposing updated label language requiring buffer zones near aquatic habitats, signaling continued but conditioned market access in the United States.

July 2023: Gowan Company Llc received expanded registrations for dinotefuran-based formulations in additional U.S. states for use in turfgrass management, broadening the addressable market for non-crop applications and reinforcing the segment's growth trajectory.

November 2023: A consortium of Japanese agricultural research institutes published peer-reviewed data demonstrating dinotefuran's efficacy in managing pyrethroid-resistant thrips populations in chrysanthemum cultivation, providing scientific validation supporting label extensions in ornamental plant markets across Asia.

February 2024: Jinan Great Chemical Industry Co, Ltd announced capacity expansion at its dinotefuran technical manufacturing facility in Shandong Province, adding an estimated 500 metric tons per annum of production capacity in response to growing export demand from Southeast Asian and Latin American formulators.

June 2024: The Australian Pesticides and Veterinary Medicines Authority (APVMA) approved a new dinotefuran-based systemic insecticide product from Agnova Technology Pty Ltd targeting soil-borne pests in Australian vegetable production systems, marking a notable regulatory milestone in the Oceania sub-region.

October 2024: Industry analysts reported a 12% year-over-year increase in Chinese dinotefuran technical-grade exports, driven primarily by demand from Brazil and India, where growers are adopting neonicotinoids with more favorable toxicological profiles relative to older organophosphate alternatives.

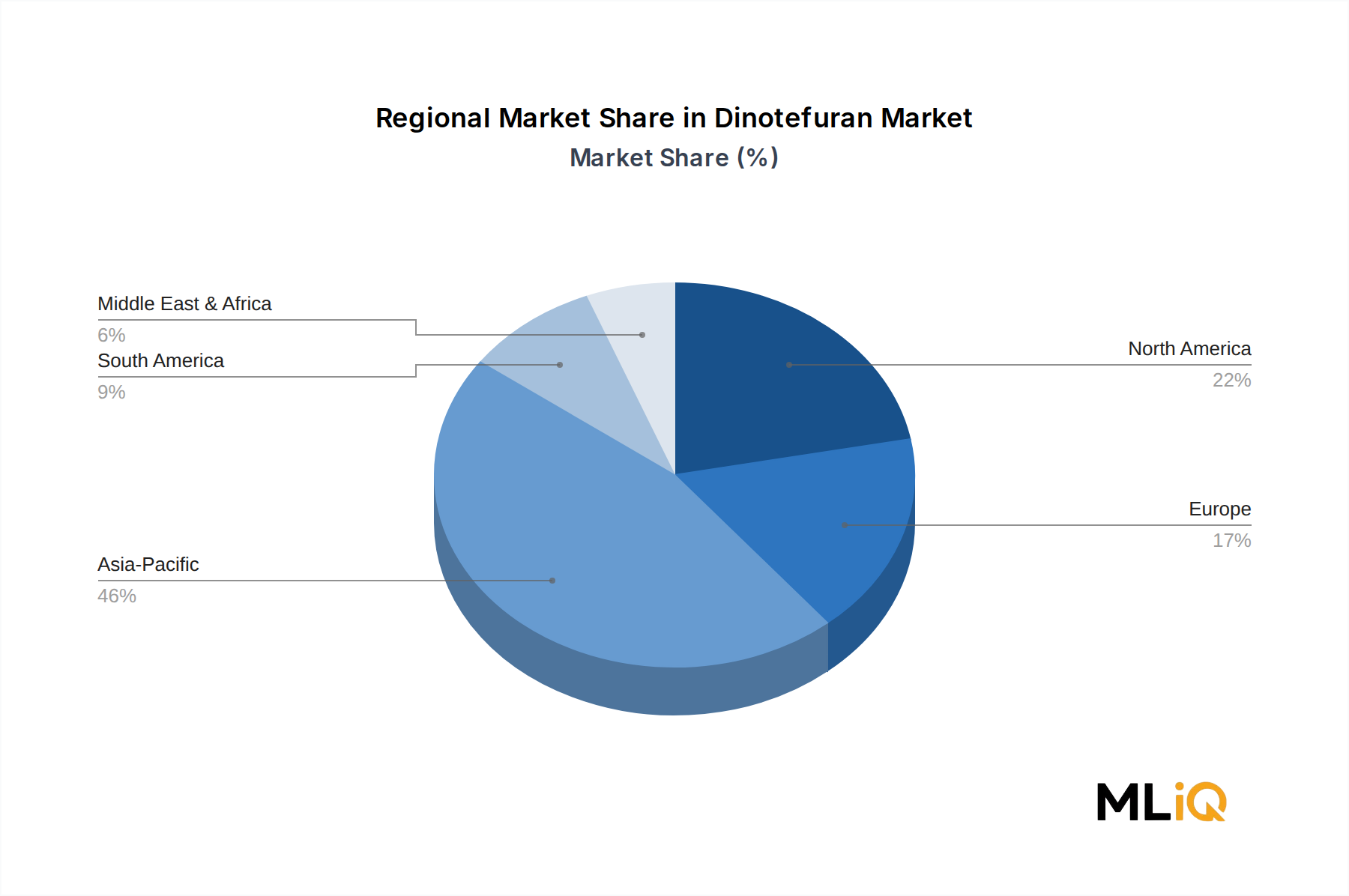

The Dinotefuran Market exhibits distinct regional demand patterns shaped by agricultural systems, regulatory environments, urbanization rates, and pest pressure dynamics.

Asia Pacific represents the largest regional market by revenue, estimated to account for approximately 38–42% of global market value in 2024. Japan remains the historical epicenter of dinotefuran consumption due to its status as the compound's country of origin and the deep penetration of dinotefuran in rice paddy management programs. China and India are experiencing the fastest volume growth within the region, driven by intensifying pest resistance, expanding horticultural production, and government-subsidized crop protection programs. The Asia Pacific region is projected to sustain a CAGR of approximately 6.1%, making it the fastest-growing major regional market globally.

North America constitutes the second-largest regional market, with the United States representing the dominant country-level demand node. Dinotefuran is extensively used in the U.S. turf management segment (golf courses, sports fields, residential lawns) and urban pest control, as well as in high-value horticultural crops including nursery stock and landscape ornamentals. The North American market is projected to grow at a CAGR of approximately 4.8%, reflecting mature penetration in some application segments offset by continued growth in professional pest management services.

Europe represents a constrained but stable market. The regulatory environment surrounding neonicotinoids remains the most restrictive globally, limiting dinotefuran's approved use categories compared to other regions. Revenue growth is modest, estimated at a CAGR of 2.9–3.5%, with demand concentrated in greenhouse ornamental production and professional pest control in urban settings where outdoor restrictions do not apply.

Latin America, led by Brazil and Argentina, is an emerging high-growth market, projected to expand at a CAGR of approximately 5.8%. The region's large-scale soybean, sugarcane, and vegetable production systems face significant aphid and whitefly pressure, and regulatory approvals for dinotefuran are progressing, creating commercial momentum.

Middle East and Africa represents the smallest regional market but offers incremental growth potential linked to expanding commercial horticulture and urban pest management infrastructure in GCC countries and South Africa.

The global trade architecture for dinotefuran is structured around a concentrated upstream production base in Asia—principally China and Japan—supplying technical-grade active ingredient to formulation hubs in India, Brazil, Europe, and the United States. China has emerged as the dominant exporter of dinotefuran technical material, with exports increasing by an estimated 12% in 2024 relative to the prior year, as documented in Chinese customs data. Key importing nations for Chinese technical-grade dinotefuran include Brazil, India, Vietnam, Thailand, and Mexico, all of which host domestic formulation industries that process imported active ingredients into locally registered end-use products.

Japan, while a smaller volume exporter relative to China, exports premium-quality

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.4% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Dinotefuran Market market expansion.

Key companies in the market include Arysta Lifescience, Mitsui Chemical Agro, Inc, Agnova Technology Pty Ltd, Aurum Pharmatech Llc, Gowan Company Llc, Chemodex Ltd, Awiner Biotech, Sigma-Aldrich Co. Llc, Jinan Great Chemical Industry Co, Ltd.

The market segments include Application.

The market size is estimated to be USD 790.96 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Dinotefuran Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Dinotefuran Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.