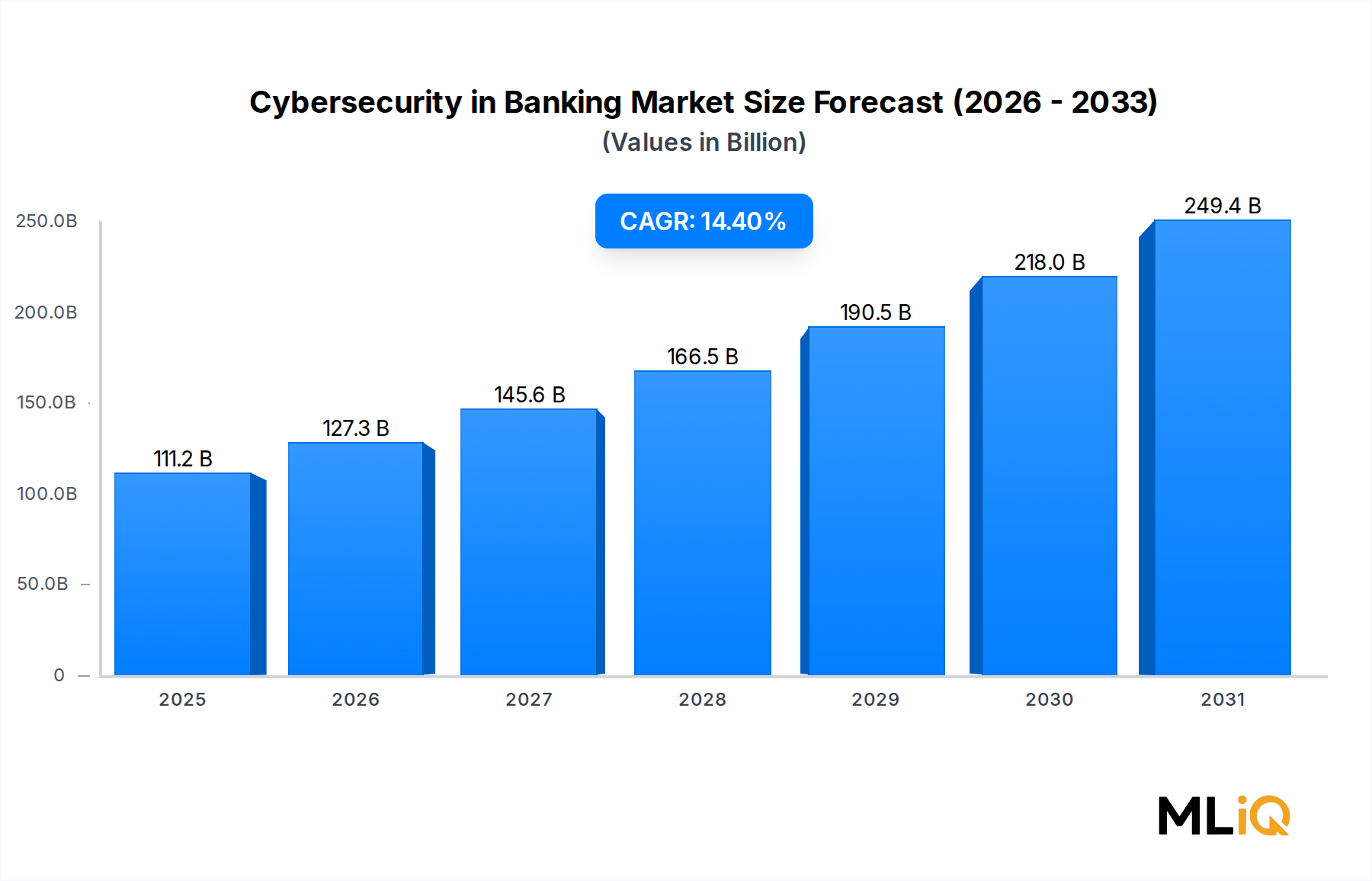

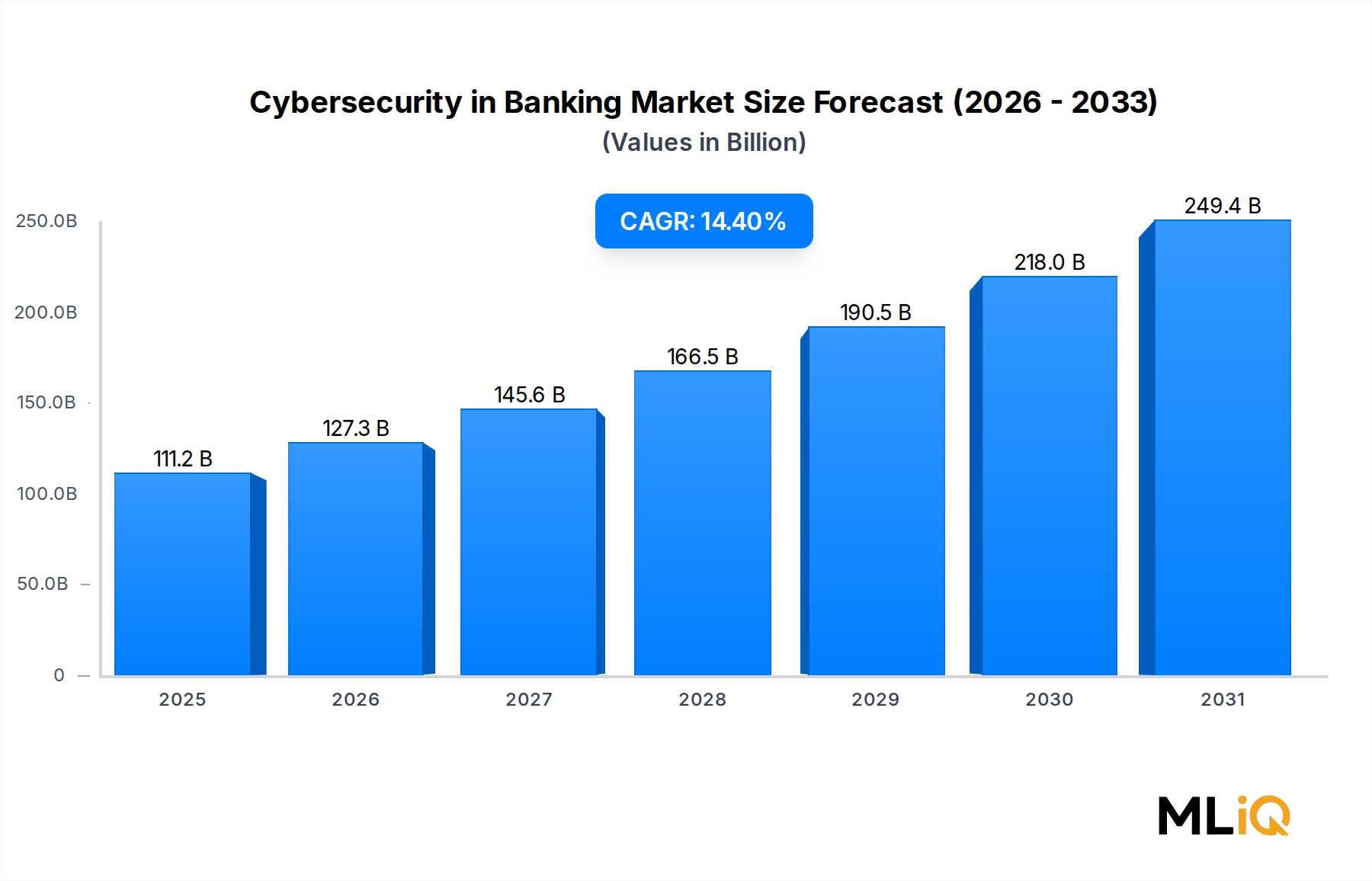

The global Cybersecurity in Banking Market is valued at $111.24 billion as of the base assessment period and is projected to expand at a compound annual growth rate of 14.4% through 2033, reflecting the sector's urgent and accelerating need for robust digital defense infrastructure. As banking institutions worldwide transition toward cloud-native architectures, open banking ecosystems, and AI-driven financial services, the threat surface has widened dramatically, compelling both regulatory bodies and enterprise risk officers to substantially increase cybersecurity budgets.

Several macro tailwinds are reinforcing this trajectory. First, the global proliferation of digital banking channels — spanning mobile payments, peer-to-peer lending platforms, and neobanks — has exponentially increased the volume of sensitive financial data being transmitted and stored, making institutions lucrative targets for state-sponsored threat actors, ransomware operators, and organized cybercriminal syndicates. Second, post-pandemic regulatory tightening across major jurisdictions — including the European Union's Digital Operational Resilience Act (DORA), the U.S. Federal Financial Institutions Examination Council (FFIEC) cybersecurity framework updates, and tightening mandates from the Monetary Authority of Singapore — has imposed mandatory investment floors on financial institutions' cybersecurity programs.

Third, the rapid adoption of hybrid multi-cloud environments within banking infrastructure has created complex identity perimeters that legacy security architectures are ill-equipped to defend. This has fueled demand specifically for zero-trust frameworks, advanced identity verification tools, and behavioral analytics platforms that can detect anomalous transactions in real time.

The market spans a diverse array of solution types including data protection, network security, cloud security, identity and access management, endpoint security, application security, email security and awareness, web security, IoT/OT security, governance, risk and compliance (GRC), security consulting, and security operations management. Each of these sub-categories is experiencing measurable investment growth, though cloud security and identity and access management solutions are demonstrating the fastest year-over-year spend acceleration.

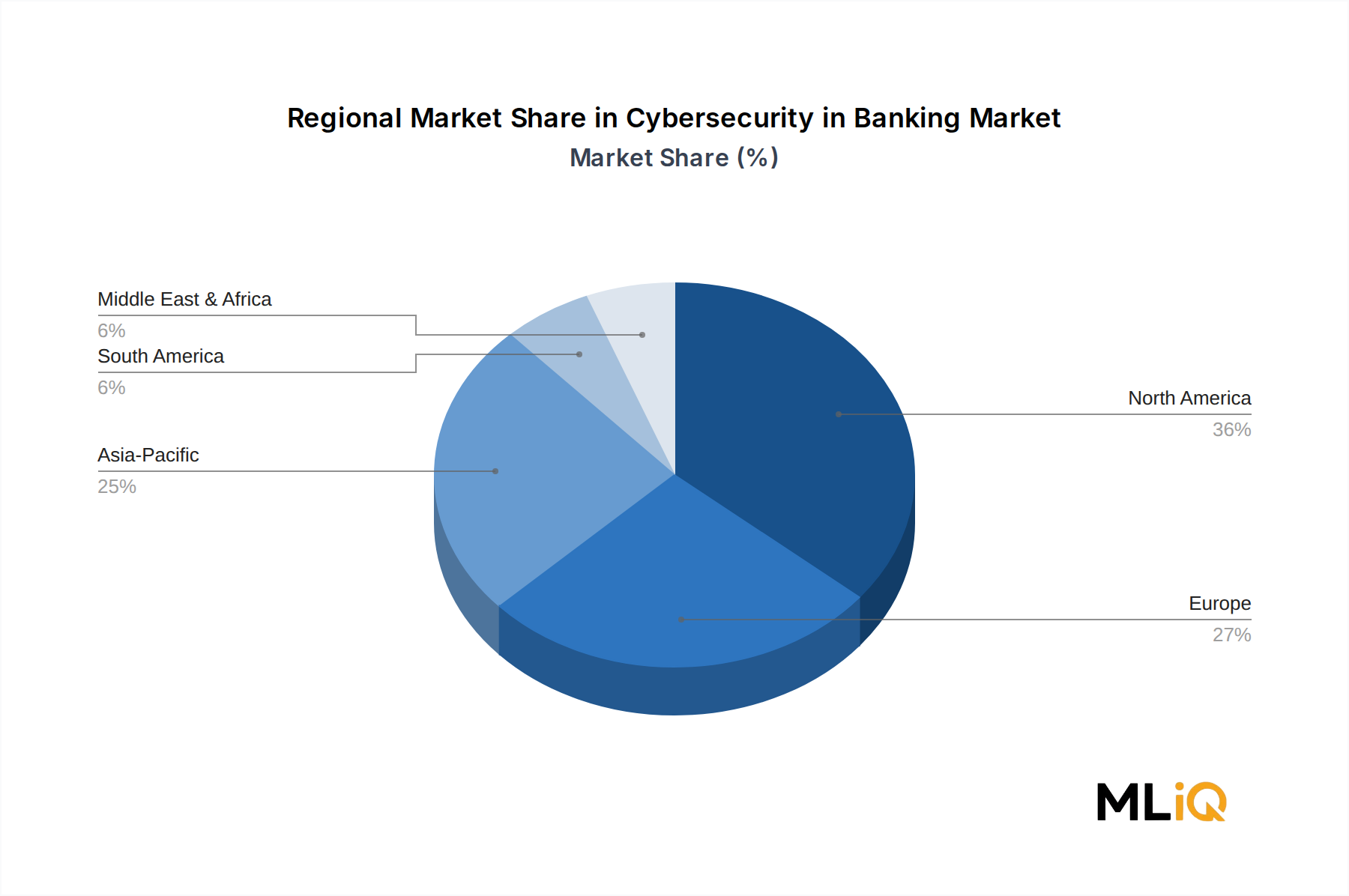

Geographically, North America dominates current revenue share, anchored by the dense concentration of global financial institutions and the maturity of domestic regulatory frameworks. Meanwhile, Asia Pacific is emerging as the fastest-growing regional market, driven by the explosive expansion of digital banking across India, China, Southeast Asia, and South Korea.

Looking forward through 2033, the market outlook remains strongly bullish. As generative AI is weaponized by adversaries to craft more convincing phishing attacks and automate vulnerability exploitation, defensive AI investment within banking cybersecurity will intensify. Institutions that delay modernization of their security operations centers risk regulatory penalties, reputational damage, and direct financial losses from breach events that increasingly surpass $5 million per incident in the banking sector.