Tied Credit Intermediation: The Dominant Segment in the Credit Intermediation Market

Among the three primary type-based segments — Tied Credit Intermediation, Ancillary Credit Intermediation, and Non-Tied Credit Intermediation — the Tied Credit Intermediation sub-segment commands the largest revenue share within the global Credit Intermediation Market. This dominance stems from the deep integration of tied intermediation activities within established banking conglomerates and large financial holding companies, where credit origination, distribution, and risk management functions are vertically consolidated under a single institutional umbrella.

Tied credit intermediaries operate by linking borrowers exclusively or predominantly to affiliated funding sources, typically represented by bank-sponsored credit products, captive insurance credit programs, and manufacturer-linked auto and equipment financing schemes. This structural alignment enables tied intermediaries to offer highly competitive pricing due to lower cost of funds, streamlined compliance oversight, and end-to-end customer relationship management. The bundling of credit with ancillary financial services — including deposits, investment products, and insurance — further reinforces retention and cross-selling efficiency.

In terms of revenue concentration, Tied Credit Intermediation benefits from the entrenched market positions of major global banks. Institutions such as JP Morgan Chase, Bank of America, and HSBC Holdings PLC operate sophisticated tied intermediation networks encompassing consumer mortgages, corporate revolving credit facilities, syndicated loans, and trade finance instruments. These banks leverage massive balance sheets, diversified funding bases, and proprietary risk models to maintain competitive advantages that are structurally difficult for smaller or non-tied intermediaries to replicate.

The segment's dominance is further reinforced by regulatory frameworks that favor capitalized, chartered institutions in credit origination. Licensing requirements, capital adequacy standards, and consumer protection mandates create significant barriers to entry, concentrating market share among established tied intermediaries. In the United States, for instance, bank-affiliated credit intermediation accounts for a substantial proportion of total outstanding credit, including residential mortgage portfolios, commercial and industrial loans, and revolving consumer credit lines.

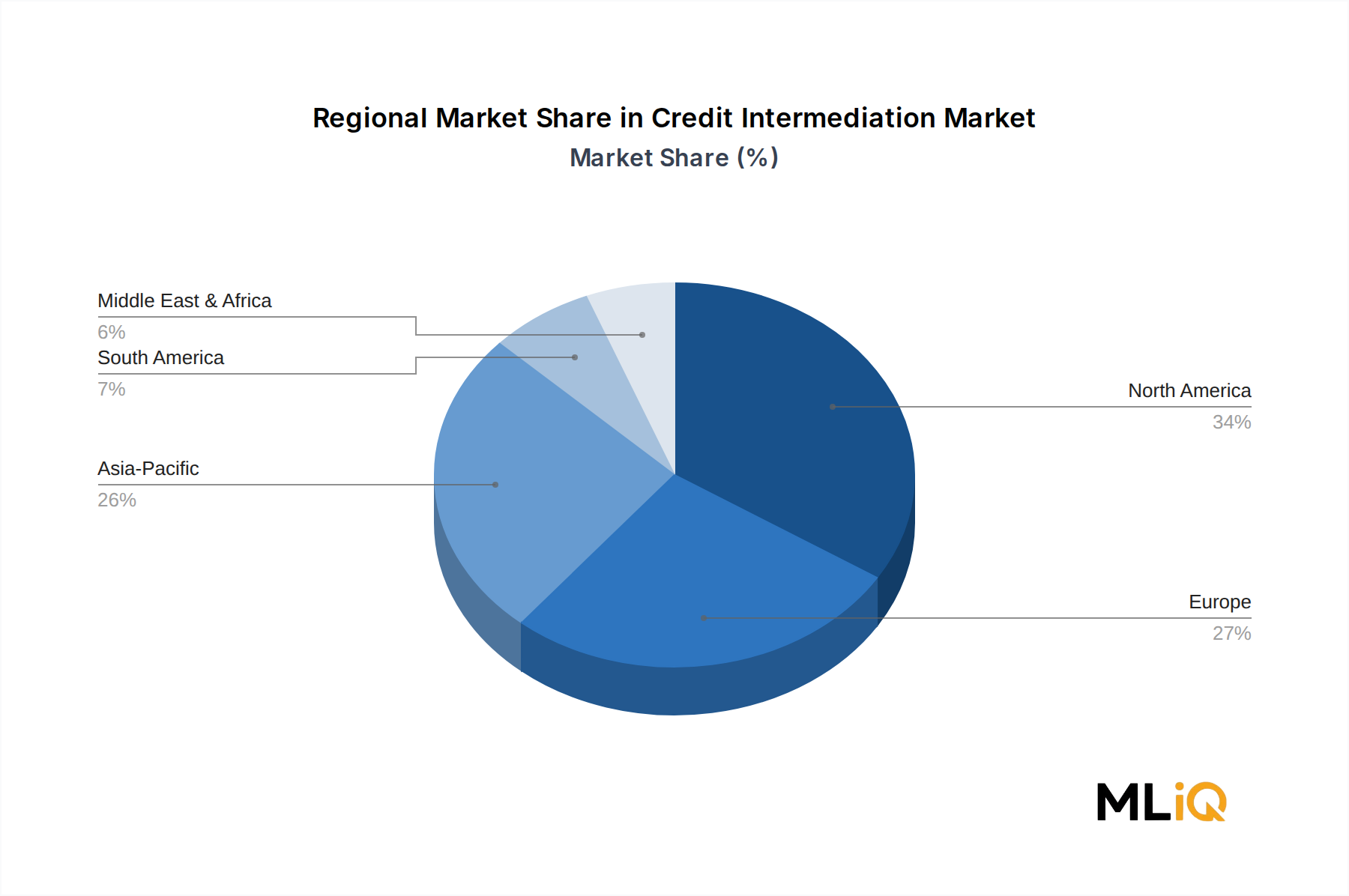

Geographically, Tied Credit Intermediation is strongest in North America and Western Europe, where universal banking models have historically concentrated credit supply within large, diversified financial groups. However, its footprint is expanding rapidly in Asia Pacific as regional banking conglomerates in China, Japan, and South Korea extend their tied intermediation franchises into new customer segments and product categories.

The segment's revenue share is consolidating rather than expanding, reflecting a broader market trend toward platformization and the entry of fintech-enabled non-tied models. Nevertheless, regulatory preferences for prudentially supervised entities, the stickiness of institutional lending relationships, and the capital efficiency advantages of tied models ensure that this segment will retain its leadership position throughout the forecast period. Key competitive dynamics within tied intermediation are increasingly centered on digital transformation investment, with incumbents racing to modernize origination workflows, deploy AI-driven credit decisioning, and integrate Banking Services Market capabilities into unified client platforms. The ability to offer seamless, omnichannel credit experiences while maintaining rigorous underwriting standards will define the competitive hierarchy within this segment through 2030.