1. 消費者の行動変化は、銀行ソフトウェア市場の購買トレンドをどのように変えていますか?

銀行や金融機関は、レガシーなオンプレミスシステムよりも、クラウドネイティブおよびAPIファーストのソフトウェア調達を優先する傾向を強めています。セルフサービス型のデジタルバンキング機能とリアルタイム決済処理が主要な購入要因となり、ベンダー選定サイクルが加速しています。フィサーブとFISは、SaaSベースのコアバンキングプラットフォームへの移行を捉えるため、製品ポートフォリオを再編成しました。

+1 2315155523

銀行ソフトウェア市場

銀行ソフトウェア市場Research Associate

Market Lens IQ は、国際市場に展開する組織に対し、高度なシンジケート調査レポート、カスタマイズされた業界分析、競合インテリジェンス、およびデータ主導のアドバイザリーソリューションを提供する、グローバルな市場インテリジェンスおよび戦略コンサルティング企業です。分析の卓越性とイノベーションへの強いコミットメントにより、Market Lens IQ は企業、投資家、コンサルタント、意思決定者に対し、競争の激しい業界における戦略的成長、業務効率化、および長期的なビジネス変革を推進するための実践的なインサイトを提供します。当社は、ライフサイエンス、消費財、半導体・電子機器、素材・化学、建設・製造、食品・飲料、エネルギー・電力、自動車・輸送、ICT・メディア、航空宇宙・防衛、BFSI(銀行、金融サービス、保険)など、幅広い業界を対象としています。深いドメイン専門知識と高度なアナリティクスを組み合わせることで、Market Lens IQ は進化するビジネス要件に合わせて調整された、包括的な市場評価、技術トレンド分析、投資インテリジェンス、サプライチェーンインサイト、価格分析、顧客行動調査、および将来の市場予測を提供します。

Market Lens IQ の機能の核心には、一次調査、二次調査、専門家インタビュー、データの三角測量、AIを活用したアナリティクス、およびリアルタイムの市場モニタリングを統合した、堅牢な360度調査方法論があります。当社の調査フレームワークは、業界データベース、企業情報のファイリング、政府刊行物、業界専門誌、規制枠組み、ホワイトペーパー、投資家向けプレゼンテーション、および世界的な経済指標を活用することにより、最高水準のデータ精度、信頼性、および戦略的妥当性を保証します。当社は、世界中の産業における新興市場の機会、破壊的テクノロジー、イノベーションエコシステム、競争のベンチマーキング、規制の変更、および高成長の投資セグメントを特定することに特化しています。顧客中心のアプローチにより、Market Lens IQ はスタートアップ、中小企業、多国籍企業、プライベートエクイティファーム、機関投資家、およびフォーチュン500企業と協力し、情報に基づいた意思決定と持続可能な競争優位性をサポートする高価値のビジネスインテリジェンスソリューションを提供します。継続的なイノベーション、デジタルインテリジェンス機能、および業界に焦点を当てた専門知識を通じて、Market Lens IQ は世界の市場調査およびコンサルティング業界における信頼できる戦略的パートナーとしての地位を確立し、組織が市場の複雑さを乗り越え、変革的な成長の機会を活用できるよう支援しています。

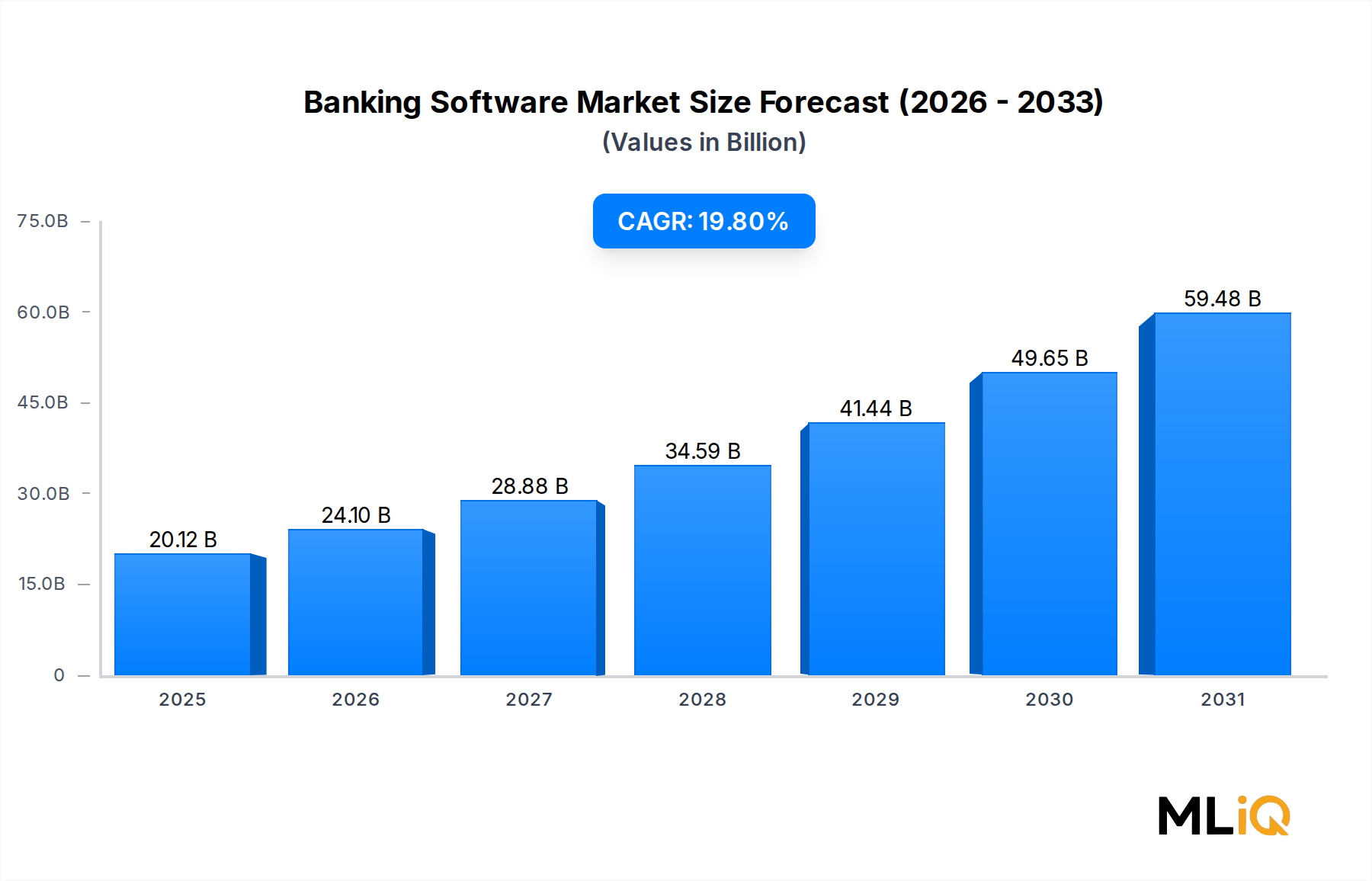

世界のバンキングソフトウェア市場は、デジタル化の加速、規制の進化、クラウドネイティブアーキテクチャの主流化によって定義される変革の10年に入っています。基準年現在、市場規模は201.2億ドル(約3兆180億円)と評価されており、2025年から2033年までの予測期間において、年平均成長率(CAGR)19.8%で拡大すると予測されており、この分野はより広範な金融サービステクノロジー市場の中で最も急速に成長している垂直市場の一つに位置づけられています。2033年までに、累積的な成長軌道は、デジタル変革、規制遵守インフラ、顧客中心の製品革新への持続的な企業投資に牽引され、市場が約970億ドル~1,000億ドルに達する可能性があることを示唆しています。

いくつかのマクロな追い風が、この成長モメンタムを維持しています。第一に、世界の金融機関は、俊敏なネオバンクやフィンテックチャレンジャーとの競争力を維持するために、多くが1970年代から1980年代に遡るレガシーなコアシステムの近代化という増大するプレッシャーに直面しています。第二に、100カ国以上での中央銀行デジタル通貨(CBDC)イニシアチブは、金融機関にプログラマブルマネーと分散型台帳統合を処理できる新しいソフトウェア層への投資を促しています。第三に、エスカレートするサイバーセキュリティの脅威は、バンキングソフトウェアスイートに組み込まれた不正検知、アンチマネーロンダリング(AML)モジュール、本人確認プラットフォームへの支出を加速させています。

欧州のPSD2やアジア太平洋地域の同等のフレームワークといった規制によって義務付けられているオープンバンキングフレームワークの急速な採用も、需要をさらに強化しています。これにより、銀行はAPI管理、開発者ポータル、サードパーティ統合ミドルウェアへの投資を必要としています。これらの要件は、一時的な移行プロジェクトをはるかに超える、持続的なソフトウェア支出サイクルを生み出しています。

供給側では、主要ベンダーは永続ライセンスモデルからサブスクリプションベースのSaaS提供へと移行しており、中堅銀行の初期費用を圧縮しつつ、これまでエンタープライズグレードのソフトウェアへのアクセスがなかった地域銀行や信用組合への総獲得可能市場を拡大しています。人工知能、機械学習、リアルタイムデータ分析のバンキングソフトウェアプラットフォームへの統合もまた、インテリジェントな意思決定エンジン、超パーソナライズされた顧客エンゲージメントツール、予測的なリスク管理モジュールを通じて新たな収益源を生み出しています。

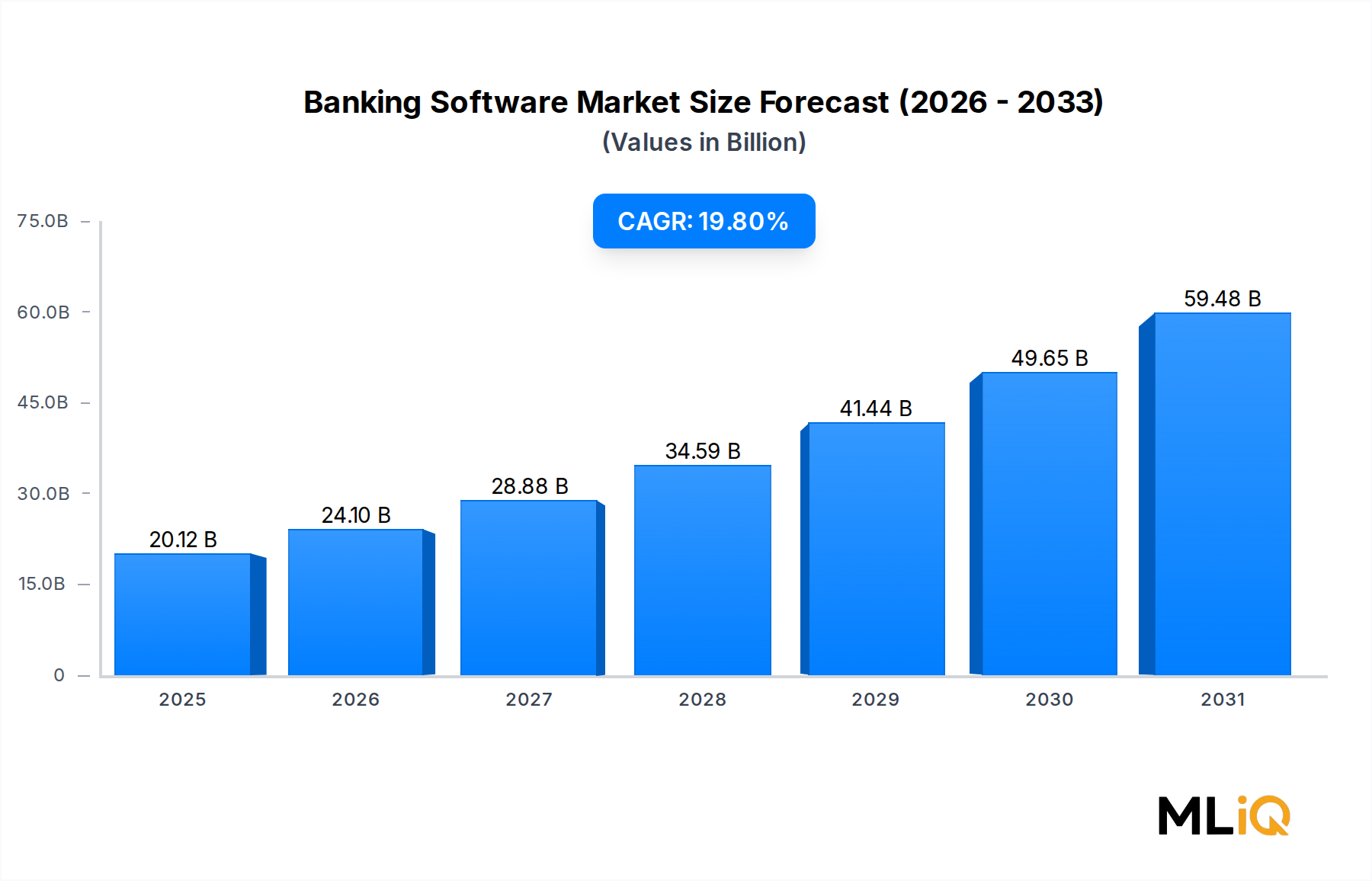

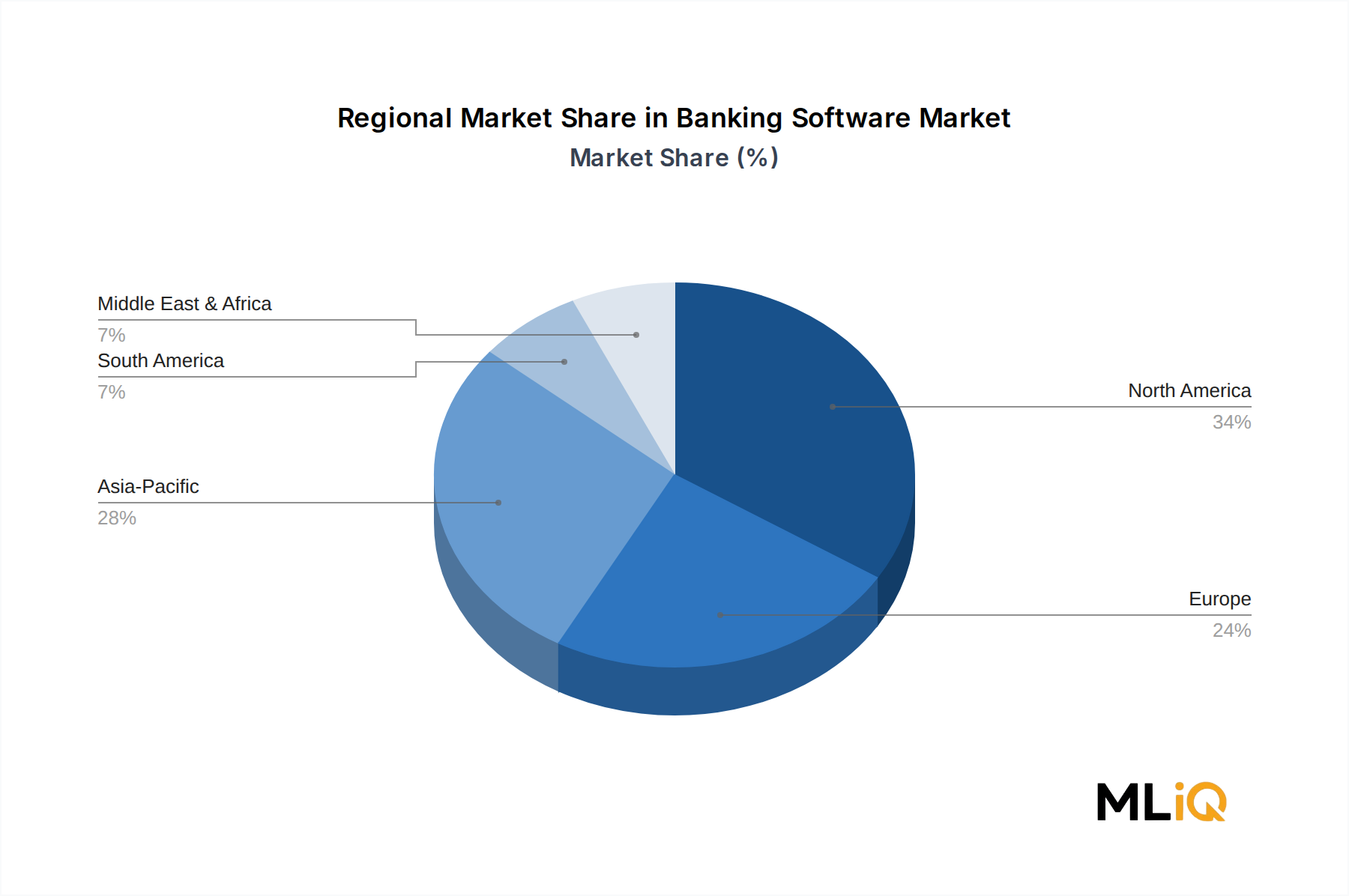

地理的には、北米が依然として主要な収益貢献地域である一方、インド、中国、東南アジアでの急速な銀行部門拡大に牽引されるアジア太平洋地域が最も急速に成長している地域として浮上しています。競争環境は上層部では断片化されており、Fiserv Inc、Fidelity National Information Services Inc、Oracle Corporationといった確立されたプレイヤーが、専門性の高いディスラプターや地域チャンピオンと競合しています。全体として、2033年までのバンキングソフトウェア市場の見通しは、景気循環的な脆弱性がほとんど見られない構造的な需要ドライバーに支えられ、非常に良好です。

バンキングソフトウェア市場において、クラウド導入セグメントは、あらゆる規模の銀行や金融機関の間で好ましいアーキテクチャモデルとしてオンプレミス設置を抜き去り、収益シェアと成長速度の両方で支配的な勢力として浮上しています。この構造的変化は、クラウドネイティブプラットフォームが、レガシーなオンプレミスインフラと比較して、優れたスケーラビリティ、新製品機能の市場投入期間の短縮、および実質的に低い総所有コストを提供するという、より広範な業界コンセンサスを反映しています。

クラウドへの移行は、制度的、規制的、競争的な圧力の収束によって推進されています。制度的観点からは、大手商業銀行はハイブリッドクラウド戦略をますます採用しています。機密性の高いワークロードをプライベートクラウド環境で維持しつつ、顧客向けアプリケーション、分析エンジン、コンプライアンスツールをAmazon Web Services、Microsoft Azure、Google Cloud Platformなどのパブリッククラウドハイパースケーラーに移行しています。このハイブリッドな姿勢により、銀行は規制上のデータ主権要件と、パブリッククラウドエコシステムが実現するイノベーション速度のバランスを取ることができます。

規制面では、欧州銀行監督機構(EBA)、通貨監督庁(OCC)、シンガポール金融管理局(MAS)などの機関によって発行されたクラウドリスク管理フレームワークは、2020年以降大幅に成熟し、銀行にクラウド導入のためのより明確なコンプライアンスガイドレールを提供しています。この規制の明確化は、これまで監督上の曖昧さからクラウド移行を遅らせていたリスク回避型機関にとって重要な解除要因となりました。

競争面では、本質的にクラウドネイティブであるネオバンクやデジタルファーストのチャレンジャーが、クラウドアーキテクチャが従来のメインフレーム環境よりも劇的に低い単位コストで毎秒数百万のトランザクションをサポートできることを実証しました。このパフォーマンスベンチマークは、既存の銀行に構造的なコスト不利を解消するために、自身のクラウド移行を加速するよう促しています。

クラウドセグメントを牽引する主要プレイヤーには、Azure for Financial Servicesプログラムを通じてAzureベースの銀行特化型ソリューションを提供するMicrosoft Corporation、AI機能と統合されたハイブリッドクラウドバンキングプラットフォームを提供するIBM Corporation、ティア1およびティア2銀行に広く採用されているクラウドベースの金融管理モジュールを提供するSAP SEが含まれます。Finastra International Limitedも、オープンバンキングクラウドプラットフォームであるFusionFabric.cloudを通じて重要な地位を築いており、これによりサードパーティのフィンテック開発者はFinastraのバンキングソフトウェアエコシステム内で直接アプリケーションを構築および展開できます。

バンキングソフトウェア市場全体におけるクラウドセグメントのシェアは、全体の市場平均である19.8%を実質的に上回るCAGRで拡大していると推定されており、一部のアナリストは、クラウド特有のCAGRを2033年まで22~25%の範囲と見積もっています。このプレミアムな成長率は、新規導入だけでなく、既存のオンプレミス契約のクラウドサブスクリプション相当への移行も反映しており、このダイナミクスはクラウド収益認識を押し上げる一方で、オンプレミス保守収益ストリームを圧縮しています。

クラウドセグメント内のサービス収益(実装、カスタマイズ、システム統合、マネージドサービスを含む)は、ソリューション収益と並行して成長しています。これは、マルチクラウドバンキングアーキテクチャの複雑さにより、専門的なプロフェッショナルサービスへの需要が高まっているためです。Tata Consultancy Services LimitedやEdgeVerve Systems Limitedなどのベンダーは、専用のバンキングクラウドプラクティスグループを通じてこのサービス収益の増加を捉えており、多くの場合、アドバイザリー、移行、およびマネージドオペレーション機能を複数年契約にバンドルし、持続的な収益の可視性を生み出しています。

今後、クラウドセグメントの優位性はさらに強固になると予想されます。ソフトウェア定義のバンキングインフラストラクチャが新規市場参入者のデフォルトアーキテクチャとなり、確立された銀行が複数年にわたる近代化プログラムを完了するにつれて、クラウド導入とリアルタイム決済レール、組み込み金融、AI駆動型パーソナライゼーションエンジンの交差点は、クラウドネイティブとオンプレミスバンキングソフトウェアスタック間の機能ギャップを拡大し続けるでしょう。

バンキングソフトウェア市場は、投資サイクル、ベンダーのポジショニング、および地域ごとの採用パターンを決定する、定量化可能な一連の推進要因と構造的な制約によって形成されています。

推進要因1 — デジタル変革への支出:業界推定によると、銀行機関による世界のIT支出は2023年に6,500億ドルを超え、ソフトウェアおよびクラウドサービスがその予算の中で拡大するシェアを占めています。フィンテックおよびネオバンクの参入企業からの競争圧力に対応して銀行の取締役会が発行するデジタル化の義務は、持続的なソフトウェア調達サイクルを支える複数年の設備投資コミットメントを生み出しています。

推進要因2 — 規制遵守要件:コンプライアンス追跡プラットフォームによると、銀行に影響を与える世界的な規制変更の量は2015年以降約40%増加しています。これにより、AMLモニタリング、顧客確認(KYC)自動化、バーゼルIV資本計算エンジン、ストレステストモジュールなど、バンキングソフトウェアに組み込まれた自動化されたRegTech市場ソリューションへの需要が高まっています。欧州のDORAから米国のCRA改革まで、各新しい規制指令は、個別のソフトウェア支出イベントを生み出します。

推進要因3 — リアルタイム決済インフラストラクチャ:2024年現在、60カ国以上がリアルタイム決済ネットワークを開始または積極的に開発しており、それぞれが銀行にコア決済処理能力のアップグレードを要求しています。リアルタイムグロス決済システムおよび即時決済レールの拡大は、決済処理ソフトウェア市場および隣接するバンキングミドルウェアへの需要を直接刺激します。

制約1 — レガシーシステム統合の複雑さ:世界の銀行取引の約70~80%が依然としてCOBOLベースのメインフレームシステムを経由しており、最新のソフトウェア導入にとって深刻な統合摩擦を生み出しています。移行プロジェクトは予算を2~4倍超過することが頻繁にあり、小規模な金融機関が完全なコアシステム交換を行うことを躊躇させています。

制約2 — サイバーセキュリティとデータプライバシーのコスト:金融サービス部門におけるデータ侵害の平均コストは、2023年に1件あたり590万ドル(約8億8,500万円)に達し(IBMデータ侵害コストレポート)、銀行はソフトウェア予算のますます多くの割合をイノベーションではなくセキュリティに割り当てることを余儀なくされており、機能開発支出に対する機会費用制約を生み出しています。

制約3 — 人材不足:金融テクノロジー分野で50万人を超える未充足のポジションが推定される、資格のあるバンキングソフトウェア開発者およびシステムインテグレーターの世界的な不足は、実装期間を長期化させ、プロフェッショナルサービスのコストを膨らませており、最新のバンキングソフトウェアプラットフォームが提供するように設計されている効率化のメリットを部分的に相殺しています。

バンキングソフトウェア市場は、グローバルな技術大手企業が専門性の高いフィンテックベンダーや地域チャンピオンと競合する、集中度の高い上位層を特徴としています。以下のプロファイルは、市場の主要参加者の戦略的ポジショニングを示しています。

Microsoft Corporation: Azureクラウドインフラストラクチャと、コンプライアンス、リスク、顧客データプラットフォーム機能をバンドルした業界固有のMicrosoft Cloud for Financial Servicesを通じて競争しています。MicrosoftのISVとのパートナーシップエコシステムは、その実質的なソフトウェア到達範囲を大幅に拡大しています。

(日本マイクロソフト株式会社として日本市場に深く関与しており、Azureを基盤とした金融機関向けソリューションを多数提供しています。)

IBM Corporation: IBM Cloud for Financial ServicesとWatsonベースのAIツールを活用し、ハイブリッドクラウドとAIを搭載したバンキングソリューションを通じてポジショニングしています。IBMが規制産業とデータ主権に注力していることは、システム上重要な金融機関(SIFI)の間で好まれる理由となっています。

(日本IBM株式会社として日本の大手金融機関に長年サービスを提供しており、クラウドとAIを活用したデジタル変革を支援しています。)

Oracle Corporation: Oracle Banking PlatformおよびOracle Financial Services Analytical Applications (OFSAA) スイートを通じて、バンキングソフトウェアの重要なプロバイダーです。Oracleの自律型データベースインフラストラクチャは、銀行のリスクおよびコンプライアンス分析ワークフローにますます統合されています。

(日本オラクル株式会社は、多くの日本の金融機関にデータベースや基幹系ソリューションを提供し、その技術は広く採用されています。)

SAP SE: 銀行向け金融管理およびエンタープライズリソースプランニングソフトウェアの主要プロバイダーです。SAPのFSDP (Financial Services Data Platform) とS/4HANA for Bankingは、大手銀行のデジタル変革エンゲージメントにおける戦略の中心です。

(SAPジャパン株式会社は、日本の主要銀行や金融機関向けにERP、財務管理、データ分析ソリューションを提供し、デジタルトランスフォーメーションを支援しています。)

Tata Consultancy Services Limited: TCSは、コアバンキング、決済、ウェルスマネジメント、保険をカバーする包括的なバンキングソフトウェアスイートとしてBaNCSプラットフォームを提供しています。BaNCSは世界中の500以上の金融機関にサービスを提供しており、特に欧州、アジア太平洋、中東で強いプレゼンスを持っています。

(日本法人である日本TCSは、TCS BaNCSを日本の金融機関に提供し、グローバルな知見と技術でサポートしています。)

EdgeVerve Systems Limited: Finacleコアバンキングプラットフォームを含む銀行および金融サービスソフトウェアに特化したInfosysの子会社であり、100カ国以上で展開され、13億以上の銀行口座をサポートしています。

(Infosysの日本法人であるインフォシスジャパンは、EdgeVerveのFinacleソリューションを日本市場にも展開し、金融業界のデジタル化を支援しています。)

Salesforce.com, Inc.: 主にFinancial Services Cloud製品を通じてポジショニングされており、Salesforceは銀行やウェルスマネジメント企業がCRM主導の顧客エンゲージメントを大規模に提供することを可能にします。Einstein AIレイヤーは、リテールバンキングにおけるネクストベストアクションやパーソナライゼーションのユースケースでますます展開されています。

(株式会社セールスフォース・ジャパンは、日本の金融機関に対し、顧客関係管理(CRM)とクラウドベースのソリューションを広く提供しています。)

Finastra International Limited: 世界最大の純粋なバンキングソフトウェアベンダーの一つであり、FinastraのオープンプラットフォームアプローチとFusionFabric.cloudエコシステムは、クローズドアーキテクチャの競合他社との差別化を図っています。その製品ポートフォリオは、リテールバンキング、レンディング、財務、資本市場に及びます。

(フィナストラは日本にもオフィスを構え、オープンバンキング戦略に基づいたソリューションを日本の金融機関に提供しています。)

Fiserv Inc: 世界中の10,000以上の金融機関にコアバンキング、決済、金融犯罪管理ソリューションを提供する支配的なプロバイダーです。Fiservによる2019年のFirst Dataの220億ドルでの買収は、北米最大の統合決済・バンキングテクノロジー企業としての地位を確固たるものにしました。

Fidelity National Information Services Inc: FISとして運営されており、130カ国の20,000以上のクライアントにバンキングおよび決済テクノロジーを提供しています。SaaSベースのModern Banking Platformは戦略的優先事項であり、クラウドネイティブなコア代替を求める中堅銀行をターゲットにしています。

2024年1月:Fiserv Incは、NOW Gatewayリアルタイム決済プラットフォームをFedNow Service接続をサポートするように拡張し、金融機関クライアントが連邦準備制度が新たに開始したレールを通じて即時決済を処理できるようにすると発表しました。

2024年3月:Oracle Corporationは、Oracle Banking Cloud Servicesの機能強化を発表しました。これには、AI駆動の信用意思決定モジュールや、融資ポートフォリオのESG開示義務に対応するために設計された埋め込み型炭素排出量報告ツールが含まれます。

2024年5月:Finastra International Limitedは、Microsoft Corporationとの戦略的パートナーシップを完了し、Fusion PhoenixコアバンキングプラットフォームをAzureに移行することで、北米の地域銀行および信用組合クライアントへのクラウド提供を加速させました。

2023年8月:Tata Consultancy Services Limitedは、TCS BaNCSを使用したフルコアバンキング近代化のために、欧州の主要なティア1銀行と複数年契約を締結しました。これは、当該年に欧州市場で発表された最大のコアシステム交換プロジェクトの一つです。

2023年10月:SAP SEは、強化されたIFRS 17およびIFRS 9コンプライアンスモジュールを備えた次世代版Banking Analyzerをリリースし、欧州およびアジア太平洋地域の保険関連銀行グループの規制報告負担に対処しました。

2023年12月:IBM Corporationは、IBM Cloud for Financial Services上のIBM Financial Services Workbenchの一般提供を開始しました。これにより、銀行は事前認証された規制環境内で準拠したAIモデルを構築、テスト、展開できるようになります。

2024年2月:EdgeVerve Systems Limitedは、コアバンキングプラットフォームの最新バージョンであるFinacle 11をリリースしました。これには、ネイティブクラウドマイクロサービスアーキテクチャ、組み込み型リアルタイム不正検知、および400を超える事前統合されたフィンテックパートナーアプリケーションのオープンAPIサポートが含まれています。

バンキングソフトウェア市場は、成長率、成熟度、および需要ドライバーの点で地域的に大きな異質性を示しており、地域ごとの銀行部門のデジタル化および規制発展段階の違いを反映しています。

北米 — 主要な収益地域:北米は、世界のバンキングソフトウェア市場の総市場価値の約35~38%を占める最大の単一地域シェアを保持しています。米国がこの貢献の大部分を牽引しており、世界最大の銀行部門(資産ベース)と、マネーセンター銀行および地域金融機関の両方における広範なテクノロジー支出に支えられています。地域のCAGRは、相対的な市場成熟度のため、世界の平均をわずかに下回る2033年まで約17~18%と推定されています。主要な需要ドライバーは、コアシステムの近代化とリアルタイム決済インフラの構築です。

アジア太平洋 — 最も急速に成長する地域:アジア太平洋地域は最も急速に成長している地域市場であり、2033年まで約23~25%のCAGRで、世界の平均を大幅に上回ると推定されています。中国、インド、日本、およびASEANブロックが主要な成長エンジンです。インドの銀行デジタル化推進は、インド準備銀行の規制近代化アジェンダとJan Dhan金融包摂プログラムによって推進されており、実質的なグリーンフィールドソフトウェア需要を生み出しています。中国の国有銀行近代化プログラムと東南アジアの急速に拡大するデジタルバンキングライセンスエコシステムは、地域の成長モメンタムをさらに増幅させています。

欧州 — 規制主導の需要:欧州は、世界の市場価値の約25~28%を占める、収益シェアで2番目に大きな地域市場です。この地域の成長は主に規制主導であり、PSD2のオープンバンキング要件、DORAの運用レジリエンス義務、およびEU AI法が持続的なコンプライアンスソフトウェア支出を生み出しています。英国、ドイツ、フランスが主要な貢献国です。地域CAGRは18~20%と推定されており、中堅欧州銀行におけるコアバンキングソフトウェア市場近代化への多大な投資に支えられています。

中東・アフリカ — 新興の機会:中東・アフリカ地域は、特にVision 2030に沿ったデジタル化プログラムが銀行部門の変革を推進している湾岸協力会議(GCC)諸国内で、バンキングソフトウェアの採用が加速しています。この地域のCAGRは20~22%と推定されており、サウジアラビア、UAE、南アフリカが主要市場です。デジタルバンキングプラットフォーム市場ソリューションへの需要は、地域の銀行がテクノロジーに精通した若い人口層を巡って競争するにつれて特に強くなっています。

南米 — 萌芽期だが成長中:ブラジルとアルゼンチンに牽引される南米は、世界の市場の小さな部分を占めていますが、成長しています。ブラジルのPIX即時決済システムは、決済ソフトウェアへの大きな需要を生み出し、進行中の銀行部門の統合がコアシステム交換サイクルを推進しています。地域のCAGRは16~18%と推定されており、主要市場におけるマクロ経済の変動によって成長が制約されています。

バンキングソフトウェア市場は、2022年~2024年の期間に、ベンチャーキャピタル、プライベートエクイティ、戦略的M&Aチャネルを通じて多大な投資活動を引きつけており、このセクターの構造的な成長ダイナミクスに対する投資家の強い確信を反映しています。

M&Aの面では、製品の幅と地理的範囲を拡大しようとするコアバンキングソフトウェアベンダー間の継続的な統合が、最も変革的な取引の背景となっています。特にコンプライアンス自動化、不正分析、デジタルオンボーディングにおけるニッチなバンキングソフトウェアプロバイダーのプライベートエクイティ支援によるロールアップが特徴的なテーマでした。Vista Equity Partners、Thoma Bravo、Francisco Partnersはそれぞれ複数の買収を完了しています。

バンキングソフトウェアの日本市場は、アジア太平洋地域全体の急成長に貢献する重要なドライバーの一つとして位置付けられています。レポートによると、アジア太平洋地域は2033年まで年平均成長率(CAGR)23~25%と、グローバル平均を大きく上回るペースで成長すると予測されており、日本もこの流れに乗りデジタル変革への投資を加速させています。

日本市場の規模は、高齢化社会の進展、低金利環境下での収益多様化の必要性、そして顧客ニーズのデジタル化への対応という、日本経済特有の背景に深く根ざしています。金融庁(FSA)が主導する金融システム全体のデジタル化推進や、地域金融機関の経営統合、オープンAPIの推進といった動きが、バンキングソフトウェアへの需要を強く喚起しています。特に、レガシーシステムの刷新は喫緊の課題であり、メインフレームからの脱却を目指す動きが活発です。

日本市場で支配的な存在感を示す企業には、本レポートに記載されているグローバルベンダーの日本法人、例えば日本マイクロソフト、日本IBM、日本オラクル、SAPジャパン、セールスフォース・ジャパンなどが挙げられます。これらの企業は、クラウド基盤、AI、CRMソリューションなどを通じて、日本の大手銀行から地域金融機関まで幅広い顧客層にサービスを提供しています。また、インドに本拠を置くTata Consultancy Services(日本TCS)やInfosysの子会社であるEdgeVerve(インフォシスジャパン)も、そのグローバルな知見とバンキングソリューションを日本市場に展開し、存在感を増しています。国内ITベンダーでは、NTTデータ、富士通、日立、NECなども金融機関向けシステム開発やインテグレーションにおいて重要な役割を担っていますが、本レポートの趣旨に鑑み、グローバルプレイヤーの日本での活動に焦点を当てています。

規制および標準化の枠組みとしては、金融庁が「金融行政方針」を通じてサイバーセキュリティ対策やクラウド利用に関するガイドラインを策定しており、金融情報システムセンター(FISC)が「FISC安全対策基準」を公表し、金融機関の情報セキュリティ対策の指針を提供しています。これらは、バンキングソフトウェアの設計、導入、運用における重要な要件となっています。また、日本銀行が推進する次世代の資金決済システム構築に向けた取り組みも、決済処理ソフトウェアの進化を促しています。

流通チャネルと消費者行動のパターンを見ると、日本では伝統的に銀行窓口での対面サービスが重視されてきましたが、近年ではモバイルバンキングやインターネットバンキングの利用が急速に普及しています。特に若年層を中心に、利便性の高いデジタルチャネルを通じた金融サービスへの需要が高まっており、各銀行はユーザーエクスペリエンス(UX)の向上やパーソナライズされたサービスの提供に注力しています。また、日本の銀行は堅牢なセキュリティと信頼性を重視する傾向が強く、ソフトウェア選定においてもこれらの要素が重要な判断基準となります。約15兆円に達する可能性のある世界市場の中で、日本の金融機関はデジタル変革を通じて国際競争力を高めるべく、積極的な投資を継続すると見込まれています。

| 項目 | 詳細 |

|---|---|

| 調査期間 | 2020-2034 |

| 基準年 | 2025 |

| 推定年 | 2026 |

| 予測期間 | 2026-2034 |

| 過去の期間 | 2020-2025 |

| 成長率 | 2020年から2034年までのCAGR 19.8% |

| セグメンテーション |

|

当社の厳格な調査手法は、多層的アプローチと包括的な品質保証を組み合わせ、すべての市場分析において正確性、精度、信頼性を確保します。

プライマリーリサーチは、当社の市場分析の礎であり、調査全体の約75%を占めています。この広範な段階では、バンキングソフトウェア市場のバリューチェーン全体にわたる主要なステークホルダーとの直接的かつ詳細なインタビューおよび議論が含まれます。その目的は、一次情報を収集し、セカンダリー調査の結果を検証し、市場トレンド、競争環境、技術的進歩、および地域固有の特性に関する定性的な洞察を得ることにあります。当社のプライマリーリサーチは、北米、南米、欧州、中東・アフリカ、アジア太平洋を含む、言及されているすべての地域にわたって実施されます。

当社のプライマリーリサーチの主要参加者は以下の通りです。

インタビュー対象企業タイプ:

インタビュー対象の役職/ステークホルダー:

| Stakeholder Role | Interview Share (%) |

|---|---|

| デジタルトランスフォーメーション責任者 | 30% |

| 最高技術責任者(CTO)/最高情報責任者(CIO) | 25% |

| シニアプロダクトマネージャー - バンキングソリューション | 25% |

| コアバンキング導入リーダー | 20% |

| Company Type | Representation (%) |

|---|---|

| コアバンキングソリューションプロバイダー | 30% |

| フィンテックイノベーター | 25% |

| クラウドインフラプロバイダー | 15% |

| システムインテグレーターおよびITコンサルティングファーム | 15% |

| 銀行業務に特化したエンタープライズソフトウェアベンダー | 15% |

当社の調査手法の残りの25%は、包括的なセカンダリーリサーチと業界ベンチマーキングに充てられています。この段階では、企業の年次報告書、投資家向けプレゼンテーション、財務諸表、業界誌、政府刊行物など、公開されているデータの厳密なレビューが含まれます。このデータは、基本的な市場規模設定、プライマリーリサーチのインプットの検証、およびバンキングソフトウェア市場に影響を与える歴史的背景とマクロ経済要因を提供します。

当社のセカンダリーリサーチは、主要な金融データベースおよび公式情報源のスイートを活用し、データの信頼性と堅牢性を確保しています。

[米国財務省](https://home.treasury.gov)、[欧州中央銀行(ECB)](https://www.ecb.europa.eu))[アメリカ銀行協会(ABA)](https://www.aba.com)[欧州銀行連盟(EBF)](https://www.ebf.eu)[金融安定理事会(FSB)](https://www.fsb.org)[国際金融協会(IIF)](https://www.iif.com)決定的に重要なこととして、本レポート内のすべてのデータは購入日まで継続的に更新されており、お客様に最新の市場洞察が提供されることを保証しています。

当社の市場規模設定と予測は、トップダウンアプローチとボトムアップアプローチの相乗的な組み合わせを採用しており、多層的なデータトライアングル法によって強化されています。この堅牢な手法は、精度を確保し、潜在的なバイアスを低減します。

トップダウンアプローチ:これは、グローバルまたは地域レベルのマクロ経済指標、金融セクター全体のIT支出、および規制トレンドを分析することにより、総市場規模を推定し、その後、特定のセグメント(コンポーネント、展開モード、エンドユーザー)に落とし込むものです。

ボトムアップアプローチ:この手法は、詳細なデータポイントから市場規模を綿密に構築します。ボトムアップ市場規模算出に使用される主要な指標と変数には以下が含まれます。

データトライアングル法:トップダウンおよびボトムアップ分析の両方からの出力は、プライマリーリサーチの結果や専門家へのインタビューと相互参照され、信頼性が高く検証された市場推定値が導き出されます。その後、履歴データ分析、CAGR予測、および業界専門家からの定性的な洞察が統合され、2026年から2034年までの包括的な予測が策定されます。

当社は、本レポートに示されている市場数値について、推定88%のデータ精度を保証します。この高い精度は、厳格な多段階データ検証および品質チェックプロセスを通じて達成されます。

この綿密なアプローチにより、お客様は戦略的な意思決定に役立つ、信頼性が高く、実用的な、非常に正確な市場インテリジェンスを確実に受け取ることができます。

銀行や金融機関は、レガシーなオンプレミスシステムよりも、クラウドネイティブおよびAPIファーストのソフトウェア調達を優先する傾向を強めています。セルフサービス型のデジタルバンキング機能とリアルタイム決済処理が主要な購入要因となり、ベンダー選定サイクルが加速しています。フィサーブとFISは、SaaSベースのコアバンキングプラットフォームへの移行を捉えるため、製品ポートフォリオを再編成しました。

アジア太平洋地域は、インド、中国、ASEAN市場での急速なフィンテック採用に牽引され、デジタル専用銀行ライセンスが増加していることから、最も急速に成長しています。インドのUPI主導のオープンバンキングエコシステムと、中国の国家主導による銀行インフラのデジタル化が、集中した需要を生み出しています。この地域は世界市場シェアの約28%を占めると推定されており、2033年まで他のすべての地域を上回ると予測されています。

フィナストラ・インターナショナルは、オープンファイナンスプラットフォームを拡張し、世界中の8,500以上の金融機関をサポートすることで、エコシステムベースのソフトウェア提供を強化しました。マイクロソフトとSAP SEは、AzureクラウドインフラをコアバンキングERPモジュールと統合するための共同開発契約を深化させました。インフォシスの子会社であるエッジバーブ・システムズは、新興市場の中堅銀行を対象としたAI駆動型貿易金融自動化製品の発売を加速させました。

レガシーシステムとの統合が主要な制約であり、推定70%のティア1銀行が依然としてCOBOLベースのコアインフラを実行しており、現代のAPI接続に抵抗しています。バーゼルIV準拠(欧州)、ドッド・フランク法(米国)、および異なるAPACフレームワークを含む法域間の規制の断片化は、ソフトウェアのカスタマイズコストを増加させ、導入期間を延長します。クラウド移行フェーズ中のサイバーセキュリティの脆弱性は、IBMやオラクルなどのベンダーにとって、複合的な供給側のリスクとなります。

商業銀行は主要なエンドユーザーセグメントを構成し、コアバンキング、リスク管理、コンプライアンスモジュールに割り当てられるソフトウェア調達予算の大部分を占めています。保険会社、信用組合、資産運用会社などの非銀行金融機関は、銀行グレードのソフトウェアスタックを採用するにつれて、より急速に成長している下流セグメントとなっています。タタ・コンサルタンシー・サービシズとSAP SEは、従来の個人向け銀行業務以外のミッドマーケット金融機関を対象とした製品層を特別に拡大しました。

北米は、ティア1金融機関の集中とSaaSベースのコアバンキングインフラの早期採用に支えられ、世界の銀行ソフトウェア市場シェアの推定34%を占めています。OCC、FDIC、連邦準備制度理事会(Fed)のデジタル資産ガイダンスに牽引される米国の規制環境は、継続的なソフトウェアコンプライアンスアップグレードを義務付けており、フィサーブやFISなどのベンダーに高い経常収益をもたらしています。さらに、米国でのベンチャー支援を受けたネオバンクの成長は、従来の商業銀行をはるかに超えて、獲得可能な顧客基盤全体を拡大しました。