Cancer Segment Dominance in the Critical Illness Insurance Market

Among all application segments — Cancer, Heart Attack, Stroke, and Others — cancer consistently commands the largest revenue share within the Critical Illness Insurance Market, a position it has held for over a decade and one that is expected to consolidate further through 2033.

Cancer's dominance is rooted in several structural realities. First, it is the most prevalent qualifying critical illness category by claim frequency. The International Agency for Research on Cancer (IARC) reported approximately 20 million new cancer cases globally in 2022, a figure projected to climb to 35 million by 2050. This epidemiological trajectory ensures that cancer-related claims constitute the plurality of all critical illness payouts, typically ranging between 55% and 65% of total claims depending on the market.

Second, the economic severity of cancer treatment is unmatched among qualifying illnesses. Advanced oncological therapies — including immunotherapy, targeted molecular agents, and CAR-T cell treatments — carry annual treatment costs that routinely exceed $200,000 per patient in high-income markets. This financial magnitude creates strong policyholder motivation to maintain coverage, resulting in persistency rates for cancer-inclusive critical illness products that outperform multi-cause peer products by approximately 8–12 percentage points.

Third, insurer product strategy has deliberately amplified cancer's centrality. The proliferation of early-stage cancer riders and carcinoma-in-situ covers, introduced at marginal premium increments, has extended the triggerable benefit window earlier in the disease continuum. This reduces the moral hazard associated with delayed diagnosis and simultaneously broadens the actionable claims universe, making cancer-related critical illness products more commercially attractive to distribution partners and policyholders alike.

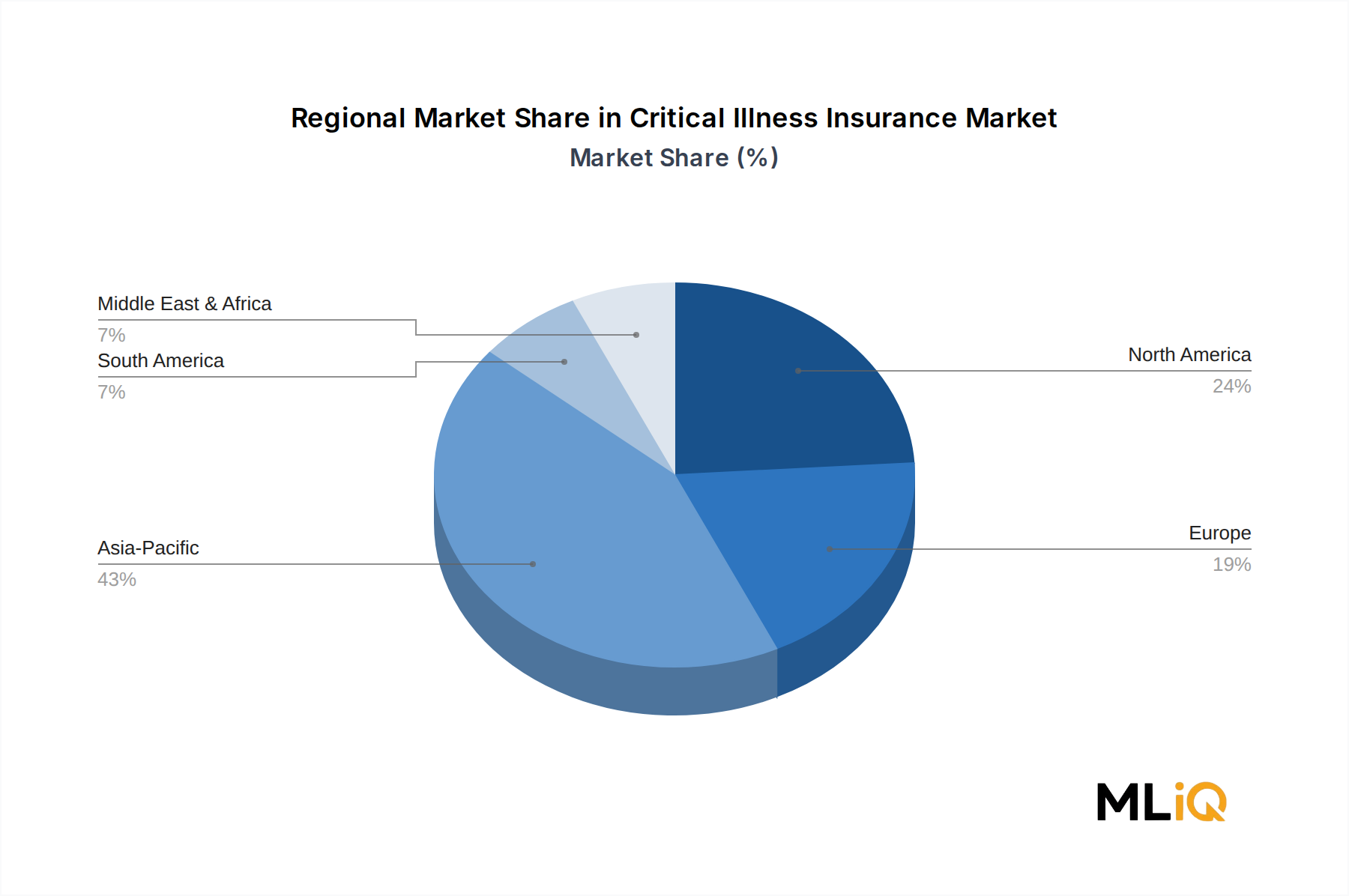

From a competitive standpoint, leading insurers including Prudential plc, AIA Group, MetLife, Sun Life Financial, and Ping An Insurance have each built dedicated cancer-focused critical illness product lines. In Asia-Pacific markets — which collectively represent the largest cancer insurance premium pool globally — cancer-specific riders generate 40–50% of total critical illness rider revenues within life insurance portfolios. China alone accounts for more than 1 in 4 global critical illness cancer claims by volume, driven by a combination of population scale, improving diagnostic penetration, and mandatory critical illness coverage requirements embedded within certain social insurance frameworks.

The segment's share is not merely holding — it is actively growing. Advances in early detection technology, including liquid biopsy and AI-assisted imaging diagnostics, are reducing the average age at first cancer diagnosis, thereby expanding the insurable population into younger, previously under-targeted demographic cohorts. Insurers are responding by recalibrating underwriting models and launching wellness-integrated products that link cancer screening participation to premium discounts, driving policy activation among millennials and Generation X consumers who have historically been underinsured.

Regulatory tailwinds are also reinforcing cancer's segment leadership. Several Asian and Latin American governments have introduced mandatory or subsidized cancer insurance schemes that leverage private insurer infrastructure for underwriting and claims management, further cementing the segment's revenue dominance. In aggregate, the cancer application segment is expected to sustain a CAGR approximating 12–13% through 2033, modestly outpacing the overall market rate of 11.2% and widening its share advantage over heart attack and stroke sub-segments.