Dominance of Power and Control Segments in the North America Electric Control Panel Market

Within the North America Electric Control Panel Market, the Power and Control segment — anchored by Motor Control Centers — commands the largest revenue share and continues to consolidate its leadership position. This segment's dominance is attributable to its indispensable role in industrial operations: MCCs serve as the centralized hub for managing, protecting, and distributing power to electric motors across a facility, making them non-negotiable infrastructure in manufacturing plants, water treatment facilities, oil and gas installations, and data centers.

The structural growth drivers for this segment are compelling. North American manufacturing output has been on an upswing driven by reshoring incentives, and every new or expanded manufacturing facility requires a fully specified MCC installation. The U.S. Department of Energy's revised energy efficiency standards for electric motors, implemented in recent years, have also prompted plant operators to upgrade aging MCC infrastructure to accommodate newer, higher-efficiency motor classes — particularly IE3 and IE4 premium efficiency motors.

The Motor Control Center Market globally is experiencing parallel growth, and the North American slice of this market is disproportionately large given the region's industrial base. Domestically, the segment benefits from stringent safety standards enforced by NFPA, NEC (National Electrical Code), and UL listing requirements, which effectively raise barriers to entry for non-certified manufacturers and sustain pricing power for established vendors.

Key players dominating this segment include ABB Ltd, which offers its MNS and UniGear MCC product families with integrated digital monitoring capabilities; Eaton, whose Freedom and Ampgard MCCs are widely specified in heavy industrial and utility applications; Schneider Electric, which has leveraged its EcoStruxure platform to embed IoT connectivity directly into MCC architectures; and Rockwell Automation Inc., whose IntelliCenter intelligent MCC series integrates seamlessly with its FactoryTalk software ecosystem.

The Automation and Instrumentation sub-segment, covering PLC panels and instrument panels, is the fastest-growing category within the broader Power and Control grouping. The Programmable Logic Controller Market is experiencing strong secular demand as manufacturers accelerate automation investments to offset labor cost pressures and meet throughput targets. PLC panels are increasingly specified with redundant processor modules, industrial Ethernet communication ports, and cybersecurity hardening features — reflecting the convergence of operational technology (OT) and information technology (IT) environments.

The DG Control segment, encompassing AMF (Auto Mains Failure) panels and DG synchronizing panels, is gaining traction as organizations invest in backup power resilience following high-profile grid disruption events across Texas, California, and Eastern Canada. This trend is reinforcing the already-robust demand for comprehensive control panel solutions that span both primary and backup power management.

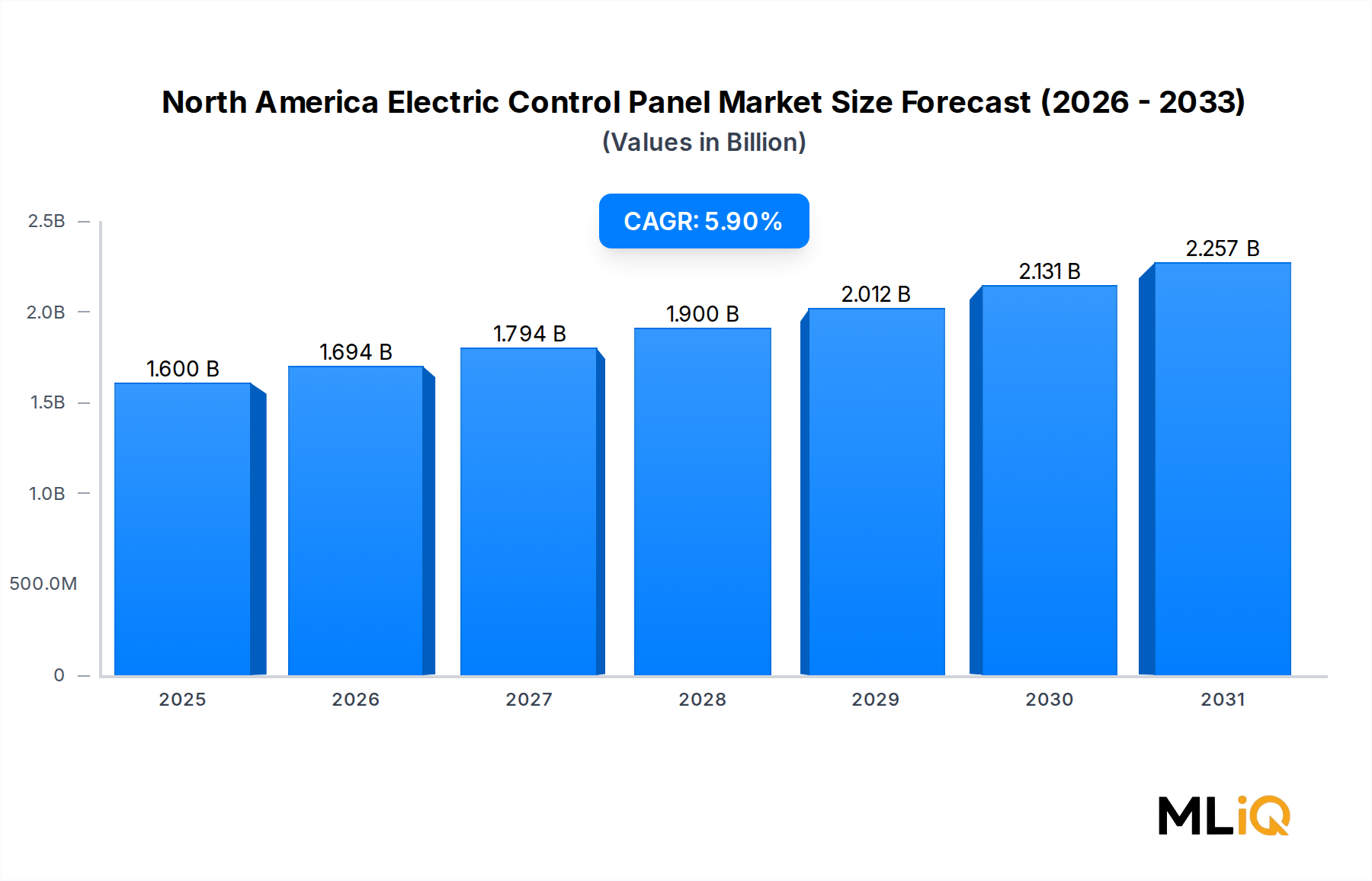

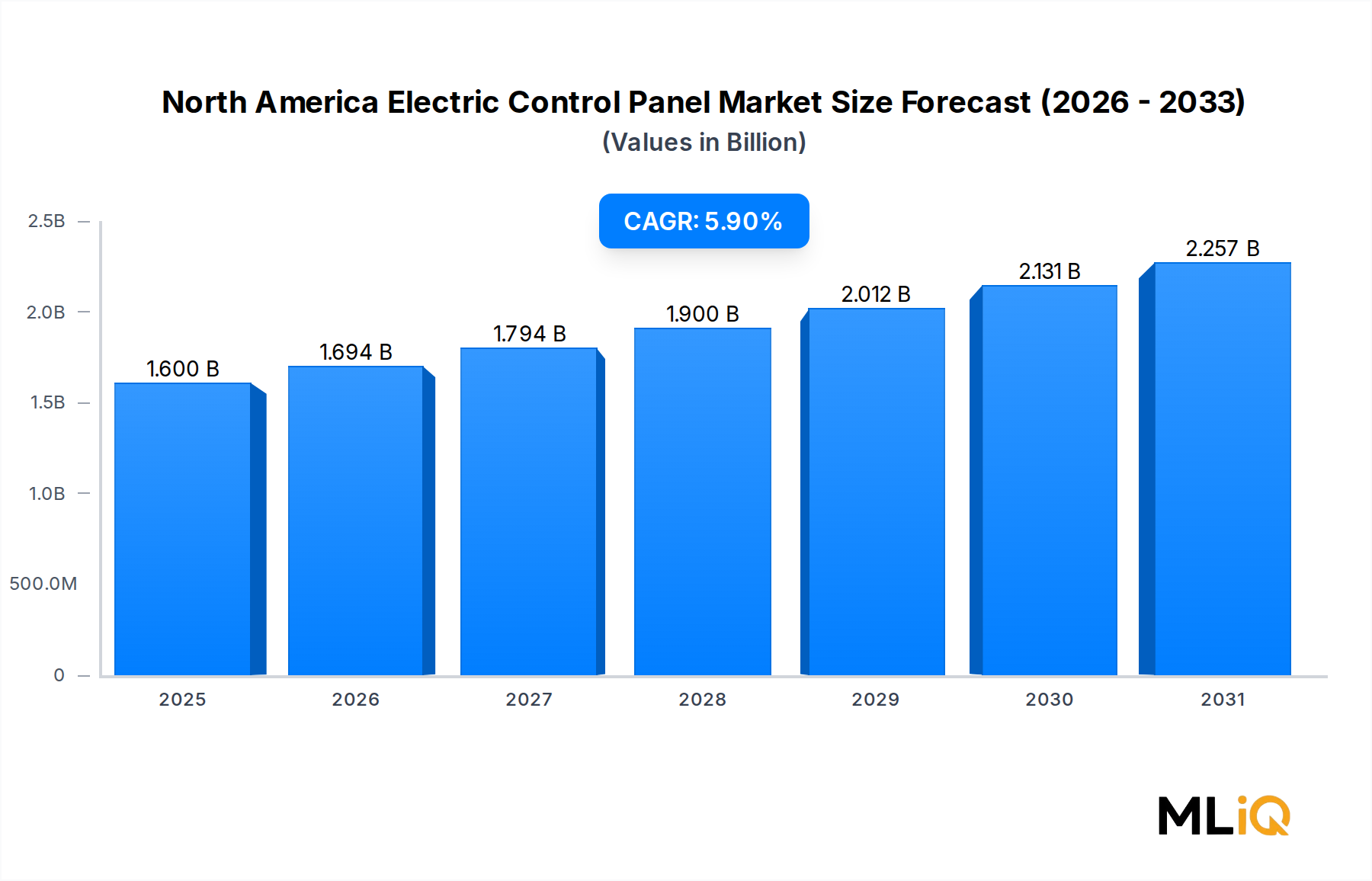

Revenue share within the Power and Control segment is estimated to represent over 45% of total North America Electric Control Panel Market revenues, with share remaining stable or modestly growing as industrial end-use demand outpaces growth in commercial and residential segments. The segment's consolidation is further reinforced by long-cycle capital procurement processes in utilities and heavy industries, which favor incumbent, certified vendors over new entrants.