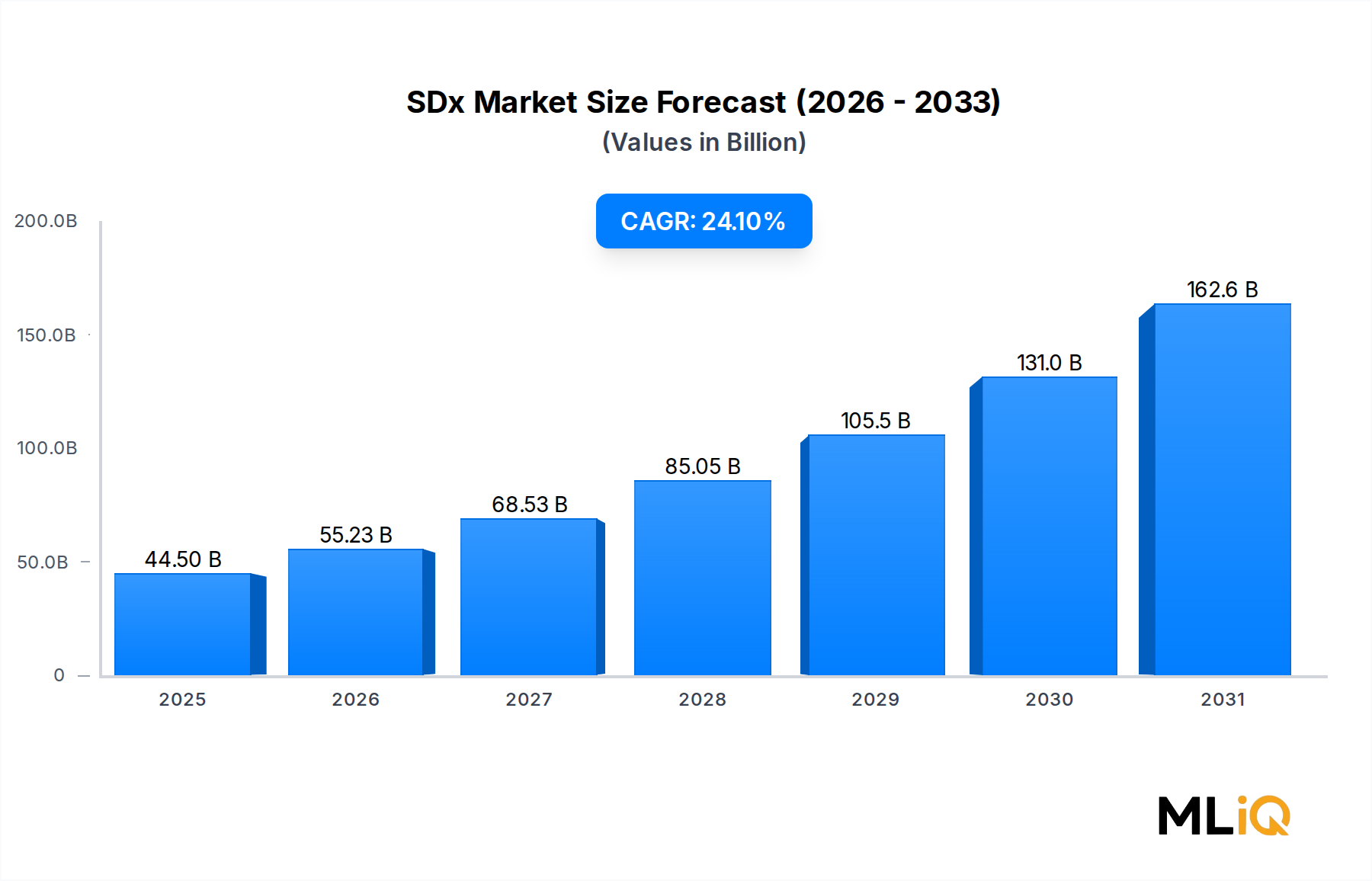

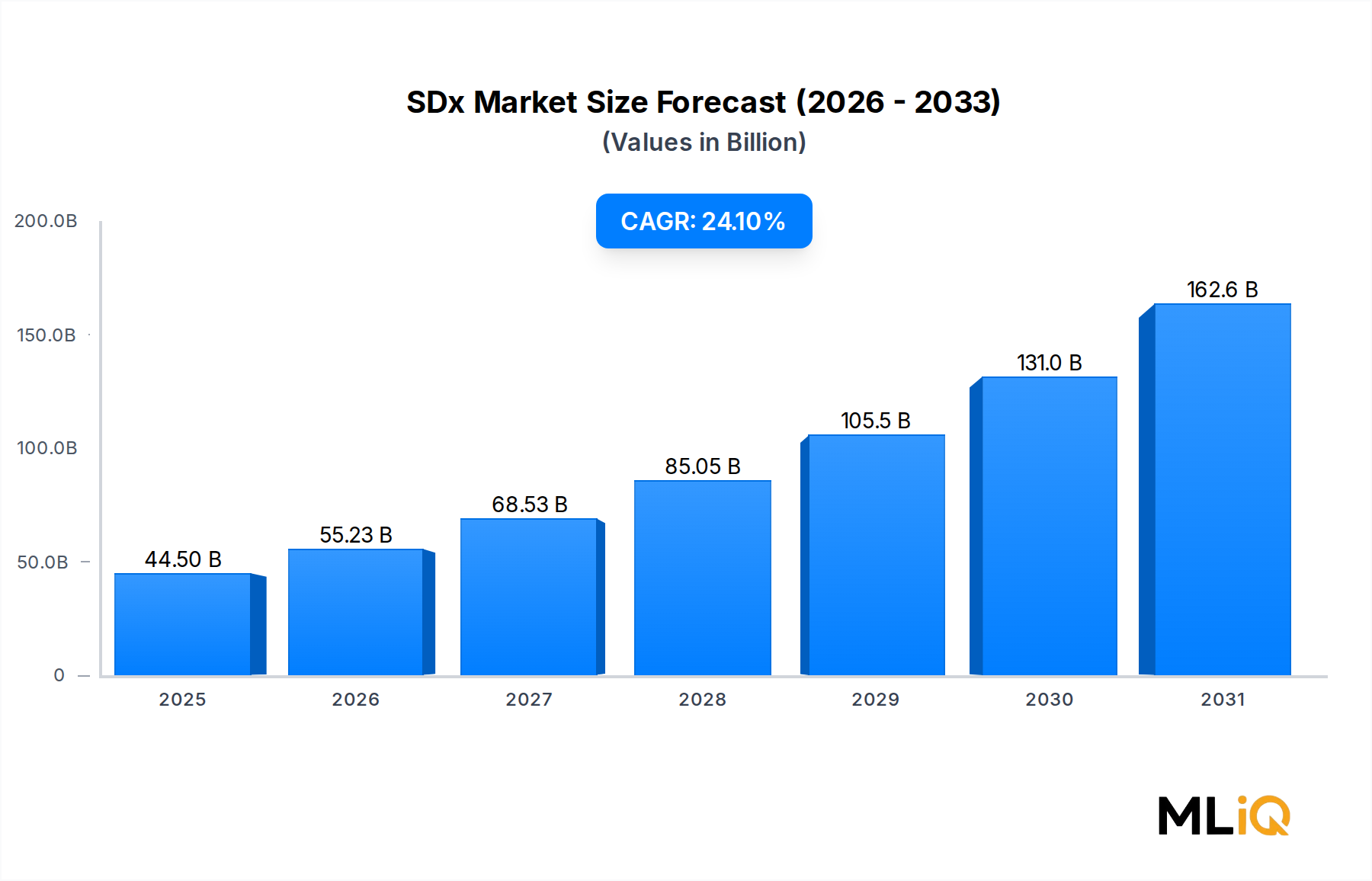

The global SDx market is positioned at a compelling inflection point, with a base valuation of $44.5 billion in 2024 and a projected compound annual growth rate (CAGR) of 24.1% through 2033. At this trajectory, the market is expected to surpass $280 billion by the end of the forecast period, driven by the accelerating enterprise shift toward software-centric IT architectures. SDx — encompassing Software-Defined Networking (SDN), Software-Defined Storage (SDS), and the Software-Defined Data Center (SDDC) — is rapidly displacing traditional hardware-centric infrastructure models across both enterprise and service provider segments.

The macro tailwinds underpinning this expansion are robust. Digital transformation initiatives have intensified post-pandemic, with organizations across verticals prioritizing agility, automation, and cost efficiency in their infrastructure stacks. Hyperscale cloud providers and telecom operators are investing aggressively in programmable infrastructure, directly fueling SDx adoption. The proliferation of edge computing, 5G network rollouts, and multi-cloud strategies has further amplified demand for flexible, policy-driven network and storage architectures.

Key demand drivers include the exponential growth in enterprise data volumes, the urgent need to reduce operational expenditure (OpEx) through automation, and the strategic imperative to enable zero-trust security frameworks that are more readily deployable over software-defined layers. The transition from CapEx-heavy hardware refresh cycles to subscription-based software models has also lowered the barrier to adoption for mid-market enterprises.

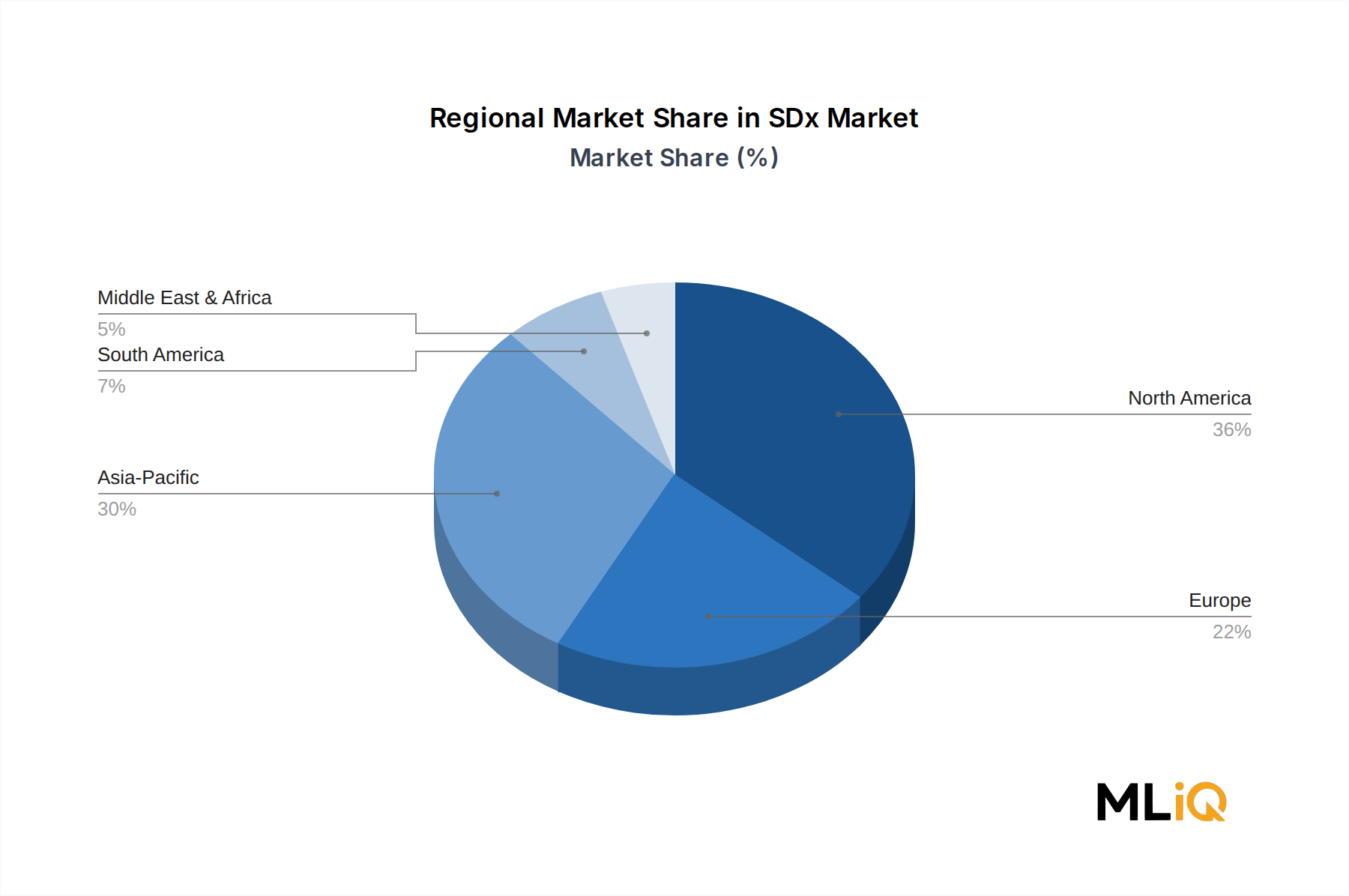

North America maintains its dominance as the highest-revenue region, underpinned by technology-forward enterprises and a mature cloud ecosystem. Asia Pacific is emerging as the fastest-growing region, fueled by hyperscale data center construction in China, India, and Southeast Asia. Europe's regulatory environment, particularly around data sovereignty and GDPR, is accelerating demand for private SDDC deployments.

From a competitive standpoint, the landscape is shaped by established technology giants including IBM Corp., Dell Technologies Inc., Intel Corp., and Hewlett Packard Enterprise, alongside specialized software innovators. Strategic partnerships, acquisitions, and platform integrations are reshaping market boundaries, with vendors increasingly offering converged SDx platforms rather than point solutions.

Looking ahead to 2033, the SDx market will be defined by AI-driven orchestration, intent-based networking, and the deep convergence of networking, storage, and compute into unified software planes. Organizations that invest early in SDx foundations will be structurally advantaged in managing hybrid IT environments at scale.