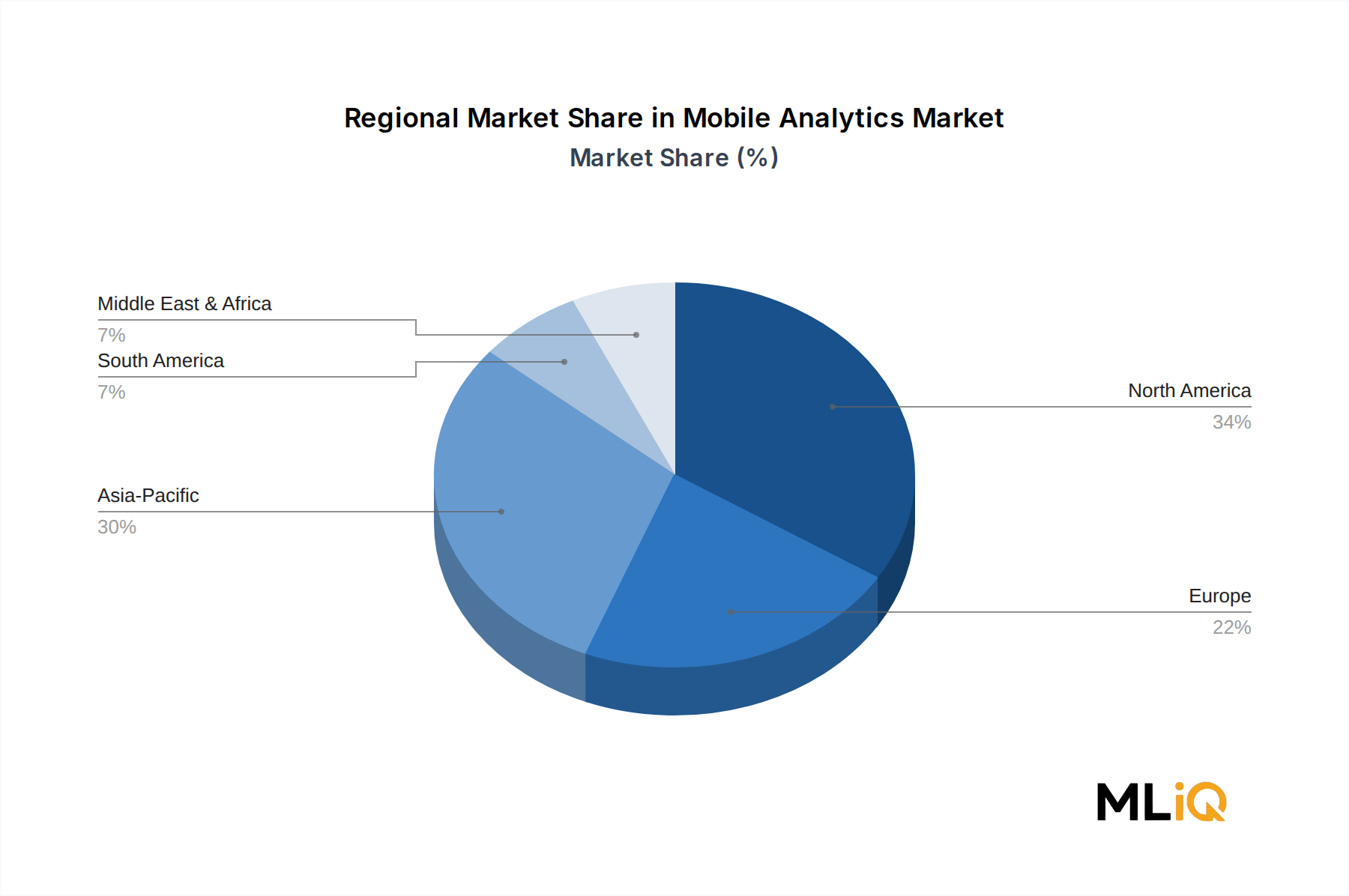

The Mobile Analytics Market exhibits pronounced regional variation in maturity, growth velocity, and the primary demand drivers shaping investment patterns.

North America commands the largest regional revenue share, estimated at approximately 38% of global market value in 2024. The United States is the epicenter of mobile analytics vendor concentration, housing the headquarters of Google, Adobe, Salesforce, Oracle, and Splunk, among others. High enterprise technology spending, sophisticated digital marketing ecosystems, and advanced mobile commerce infrastructure drive sustained demand. The regional CAGR for North America is estimated at 16.8% through 2033, reflecting a relatively mature but still-expanding market where growth is increasingly driven by platform upgrades, AI feature adoption, and privacy-compliant measurement solution transitions.

Asia Pacific is the fastest-growing regional market, with a projected CAGR of 23.1% through 2033. China, India, Japan, South Korea, and ASEAN economies collectively represent a massive and rapidly mobilizing user base. India alone surpassed 700 million smartphone users by 2024, with mobile internet penetration accelerating in Tier 2 and Tier 3 cities. The region's mobile-first consumer behavior — where a significant proportion of the population accessed the internet exclusively via mobile devices — has created exceptional demand for mobile advertising analytics, app performance monitoring, and behavioral analytics platforms. The relationship between the Mobile Analytics Market and the Mobile Advertising Market is particularly evident in Asia Pacific, where programmatic mobile advertising spend is growing at double-digit rates annually.

Europe accounts for approximately 22% of global market revenue, with a CAGR of 17.2%. GDPR compliance requirements have uniquely shaped the European market, driving demand for privacy-native analytics platforms, server-side tagging solutions, and consent management integrations. Germany, France, and the United Kingdom are the largest national markets, with strong adoption across financial services, retail, and media sectors.

Middle East & Africa represents an emerging growth pocket, with a CAGR of 21.4%, driven by GCC nations investing in smart city infrastructure, digital government services, and mobile commerce ecosystems. Mobile penetration rates in Saudi Arabia and the UAE exceed 90%, creating a sophisticated mobile analytics demand base.

South America, led by Brazil and Argentina, is growing at approximately 18.6% CAGR, driven by fintech adoption and mobile payment ecosystem expansion. The relationship between the Mobile Analytics Market and the Customer Analytics Market is particularly salient in Brazil, where customer data platform investments are accelerating among retail banks and e-commerce operators.