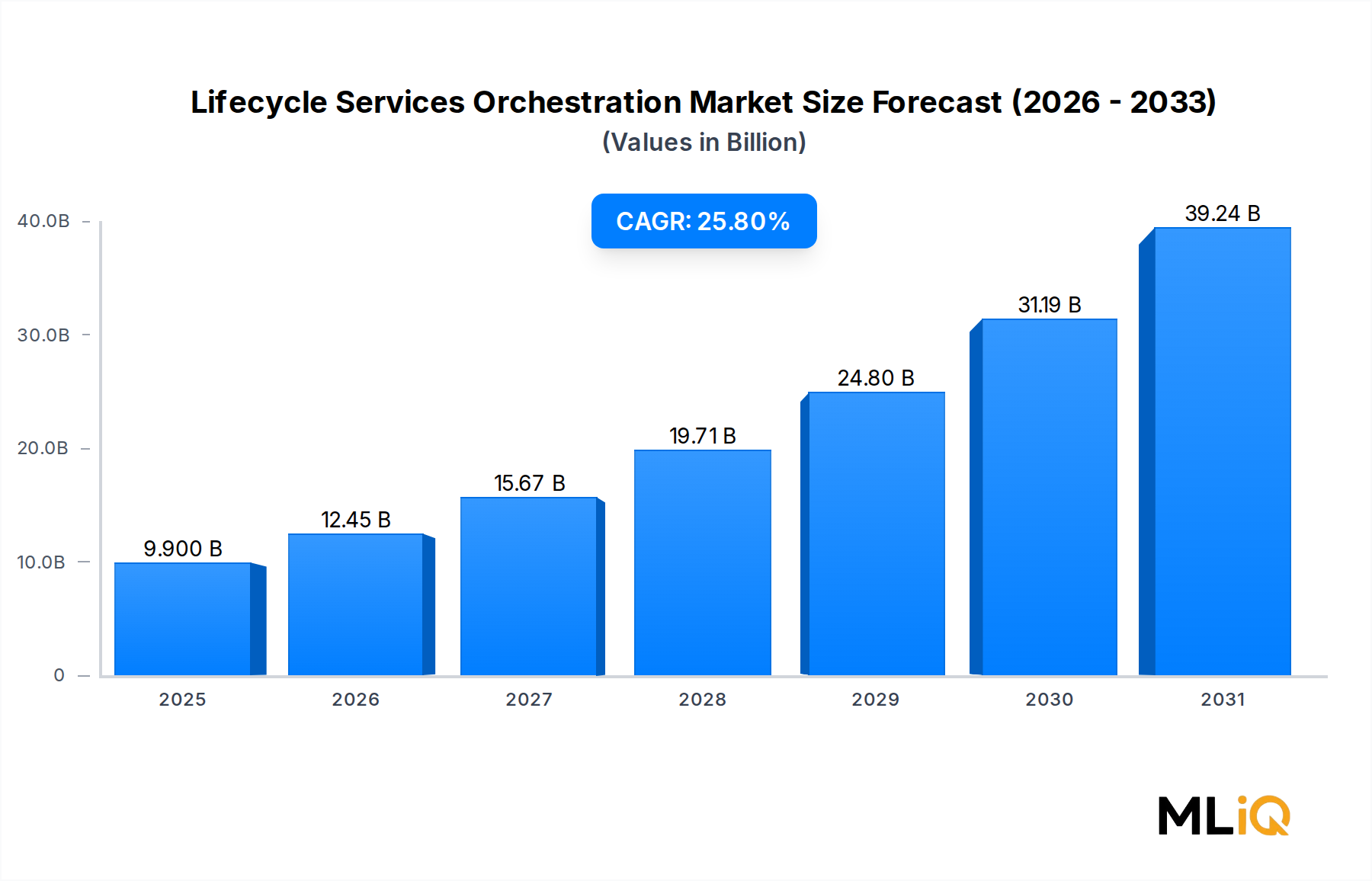

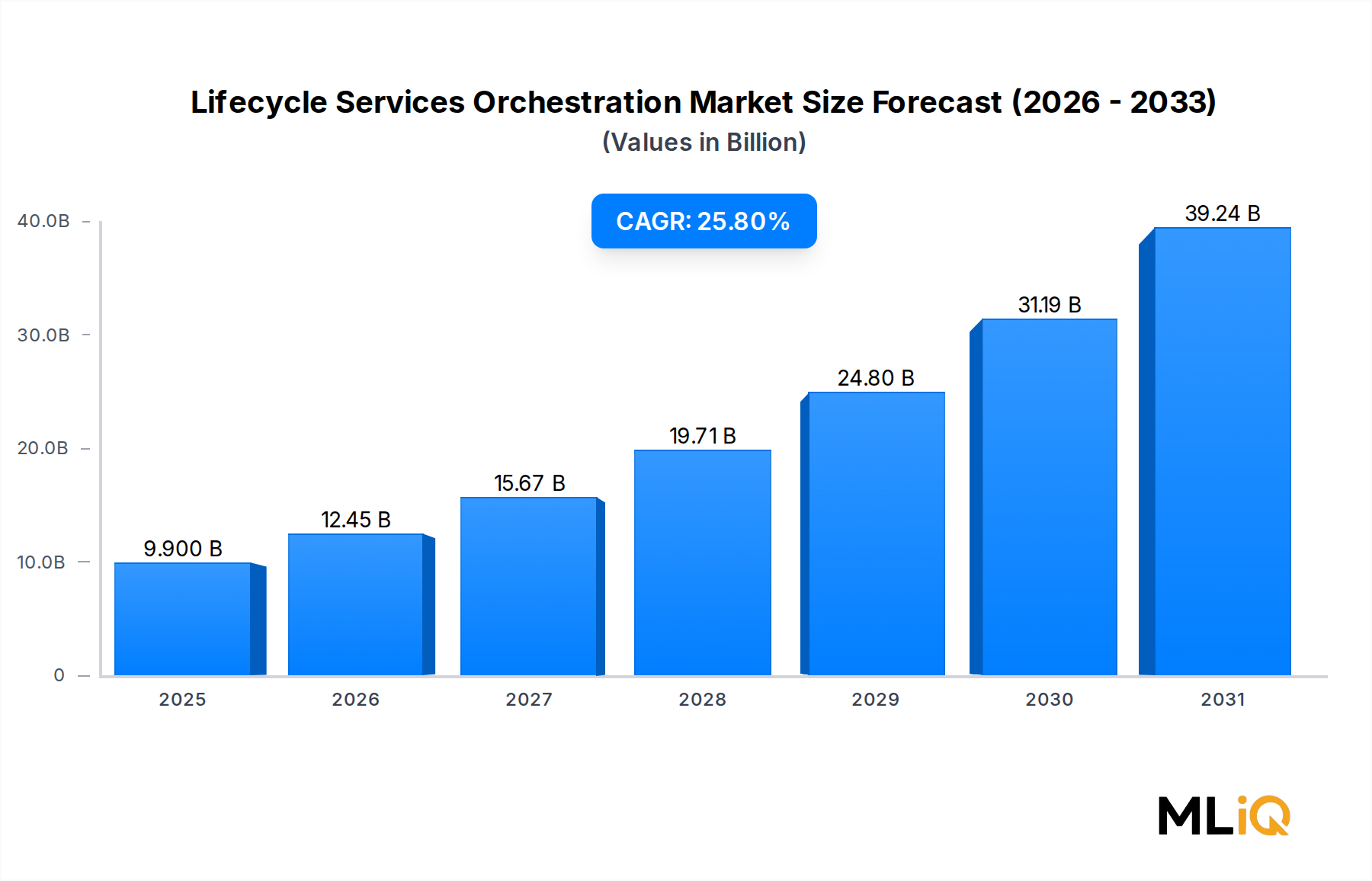

The global Lifecycle Services Orchestration Market is positioned at a pivotal inflection point, with a base valuation of $9.9 billion in 2025 and a projected compound annual growth rate (CAGR) of 25.8% through 2033. At this trajectory, the market is expected to surpass $62 billion by the end of the forecast period, reflecting an extraordinary expansion driven by the global telecommunications and enterprise IT sectors' urgent need for automated, end-to-end service management frameworks.

The convergence of 5G deployment cycles, cloud-native infrastructure adoption, and the exponential growth of virtualized network functions is fundamentally reshaping how service providers and enterprises conceive, deploy, monitor, and retire digital services. Lifecycle Services Orchestration (LSO) platforms sit at the center of this transformation, enabling organizations to manage service lifecycles spanning provisioning, assurance, activation, and decommissioning through a unified, automated layer.

Key demand drivers include the accelerating rollout of 5G networks globally, which is generating unprecedented complexity in service layer management. Operators are under mounting pressure to reduce time-to-market for new services while simultaneously cutting operational expenditures — a dual mandate that manual processes cannot satisfy. LSO platforms directly address this challenge by automating workflows across multi-domain, multi-vendor environments.

Macro tailwinds further amplifying market momentum include rising enterprise cloud migration rates, the proliferation of IoT endpoints requiring dynamic service provisioning, and the growing adoption of zero-touch network operations philosophies. Regulatory mandates in several jurisdictions for open interfaces and interoperability — particularly aligned with MEF (Metro Ethernet Forum) standards — are also catalyzing LSO adoption among tier-1 and tier-2 carriers.

The software segment continues to capture the largest share of revenue within the market, owing to the recurring nature of SaaS-based licensing models and the increasing preference for platform-based orchestration over point solutions. Meanwhile, the services segment — encompassing professional services, managed services, and support contracts — is the fastest-growing sub-category as operators seek implementation expertise and ongoing operational support.

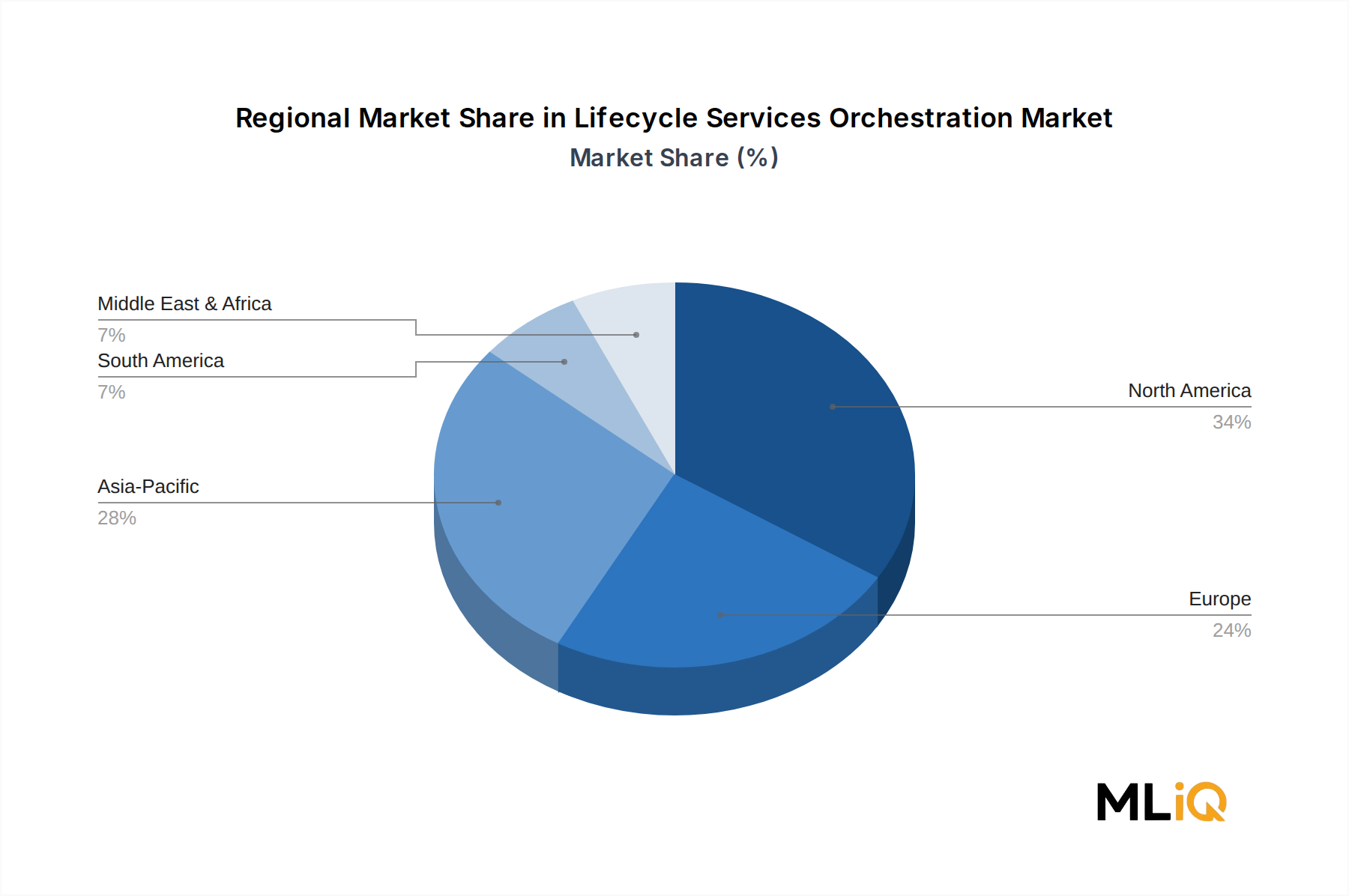

From a deployment standpoint, native deployments are gaining ground over migration-based implementations, particularly among greenfield 5G operators in Asia Pacific and the Middle East who are building orchestration frameworks from the ground up. North America remains the most mature market by revenue contribution, while Asia Pacific is registering the highest growth velocity.

Looking ahead through 2033, the Lifecycle Services Orchestration Market will be increasingly defined by artificial intelligence integration within orchestration engines, enabling predictive service lifecycle management, autonomous fault remediation, and self-healing network architectures. The competitive landscape is intensifying, with both established telecom software vendors and cloud-native challengers vying for platform dominance.