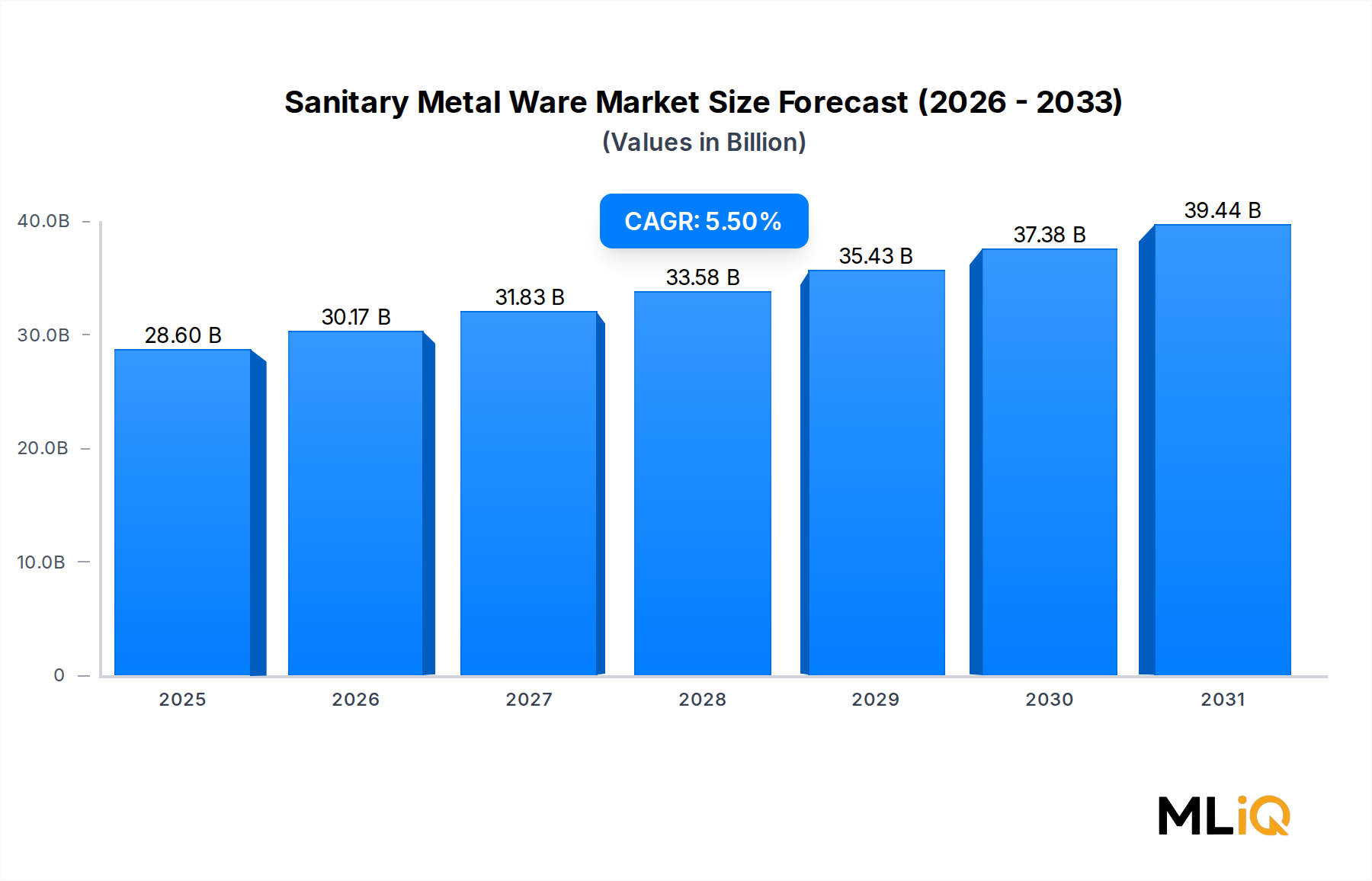

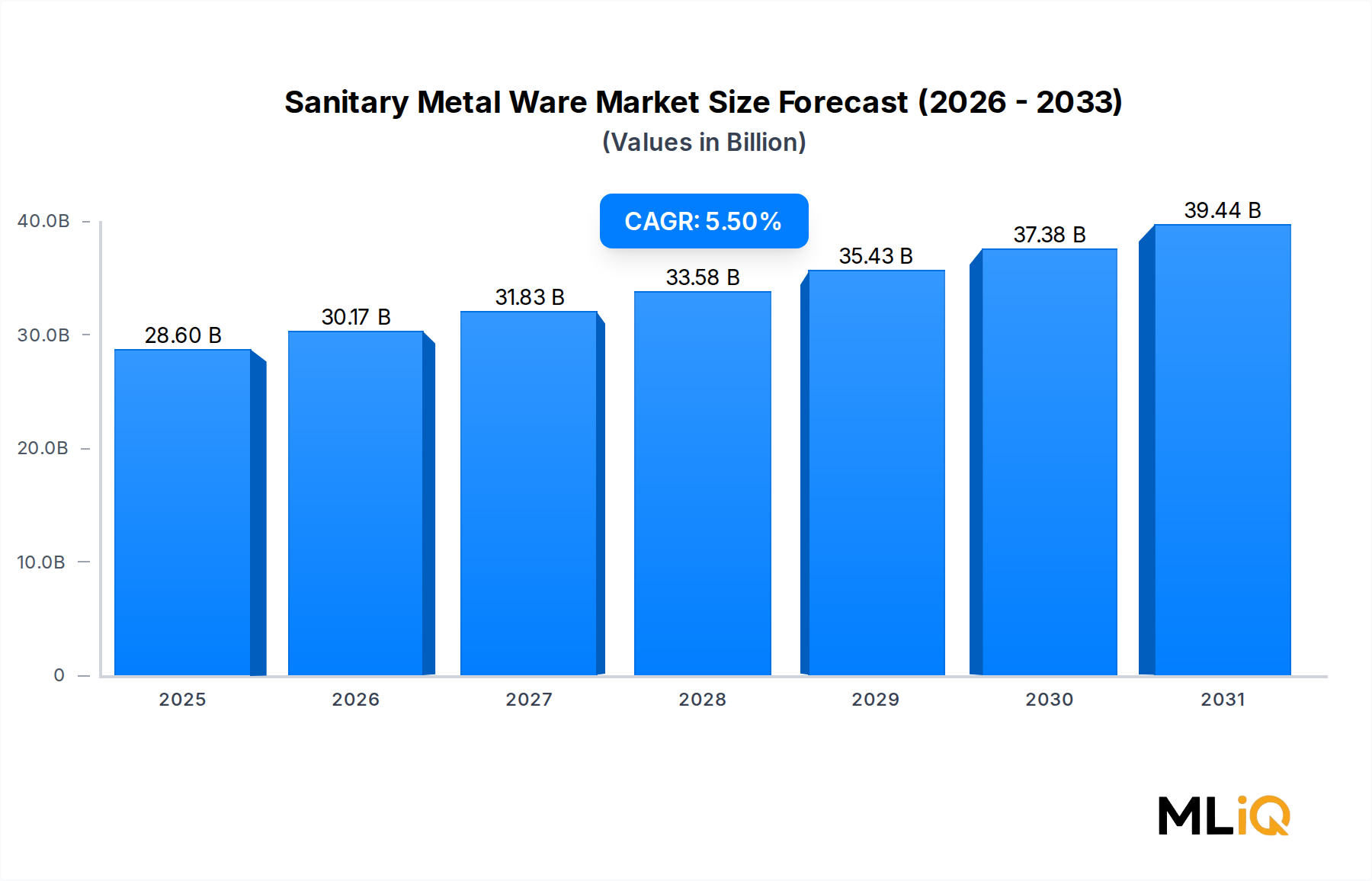

The global Sanitary Metal Ware Market is valued at $28.6 billion in 2025, underpinned by a compound annual growth rate (CAGR) of 5.5% projected through the forecast horizon. This market encompasses a broad spectrum of metal-based sanitary products including showers, faucets, floor drains, towel racks, toilet paper holders, glass platforms, and sanitary pendants, all deployed across household, commercial, and real estate project applications.

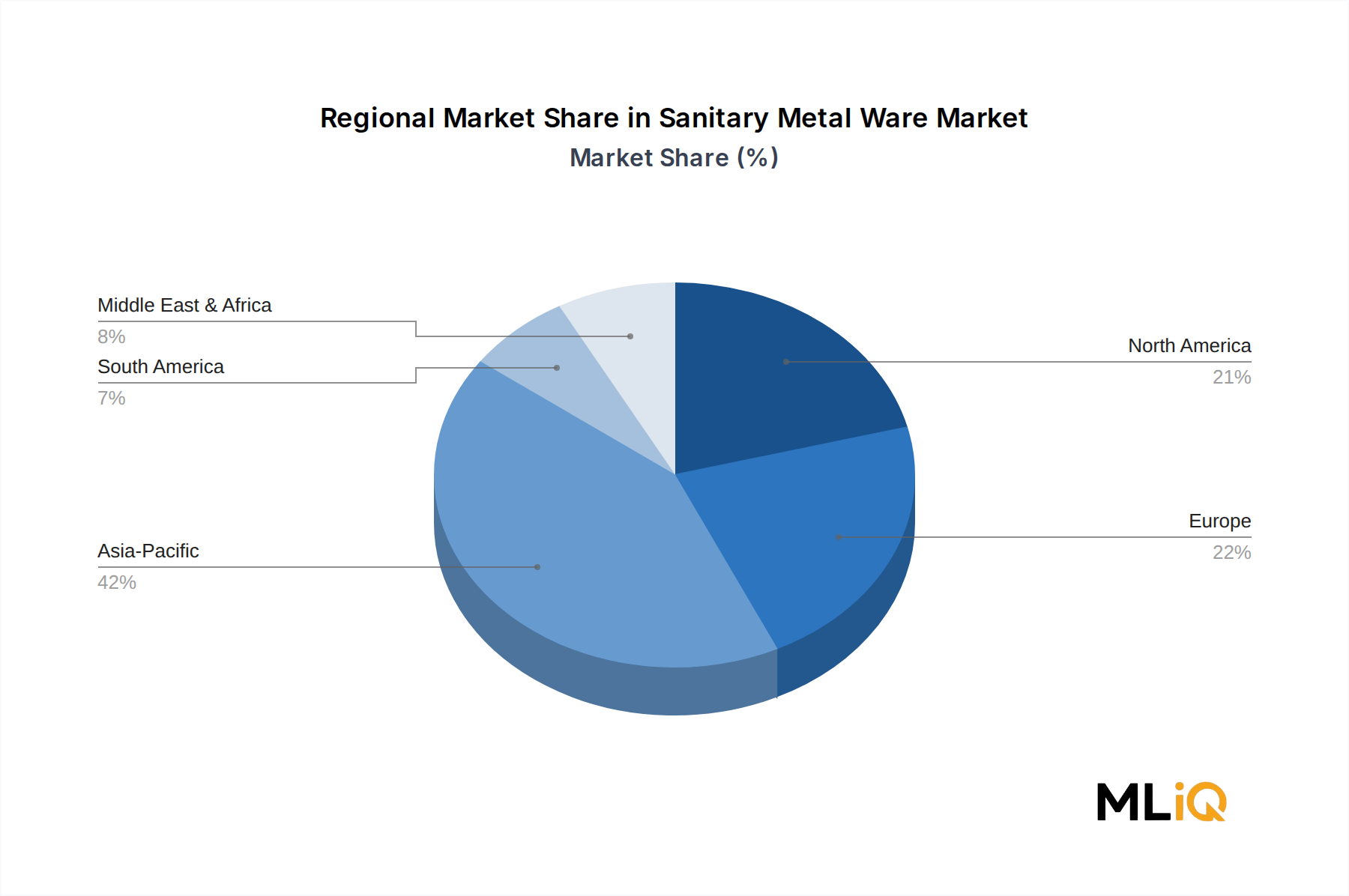

The primary demand catalysts shaping this market's expansion include accelerating urbanization across Asia Pacific and the Middle East, government-backed housing incentive programs, and a paradigm shift among consumers toward premium, design-forward bathroom fixtures. Public-private partnerships in infrastructure development — particularly in emerging economies — are unlocking previously latent demand corridors that are expected to sustain volume growth over the medium term.

From a macro perspective, the post-pandemic renovation wave has significantly elevated consumer spending on home improvement, with bathrooms consistently ranking among the top renovation priorities. Simultaneously, commercial real estate recovery — particularly in the hospitality, healthcare, and corporate sectors — is generating sustained procurement demand for high-specification sanitary metal ware. Real estate project pipelines in China, India, and Southeast Asia are providing further structural tailwinds, as large-scale residential and mixed-use developments specify metal sanitary products as standard-grade installations.

On the supply side, manufacturers are investing in advanced surface finishing technologies, antimicrobial coatings, and water-conservation features to comply with tightening regulatory standards and to differentiate in an increasingly competitive marketplace. The integration of digital manufacturing processes, including CNC machining and precision casting, is enabling tighter tolerances, more complex geometries, and faster time-to-market cycles.

The competitive landscape is highly fragmented at the regional level but exhibits oligopolistic tendencies at the premium tier, where brands such as Kohler, Hansgrohe, Grohe, and TOTO command disproportionate pricing power and brand equity. Consolidation activity remains an ongoing feature, with larger players acquiring regional manufacturers to expand geographic footprints and production capacities.

Looking forward, the Sanitary Metal Ware Market is poised for sustained structural growth, driven by demographic trends, rising middle-class aspirations in developing markets, and regulatory pressure toward water-efficient and sustainable products. The convergence of aesthetics, technology, and environmental compliance is expected to redefine value propositions across all segments through 2030 and beyond, positioning early innovators for outsized market share gains.