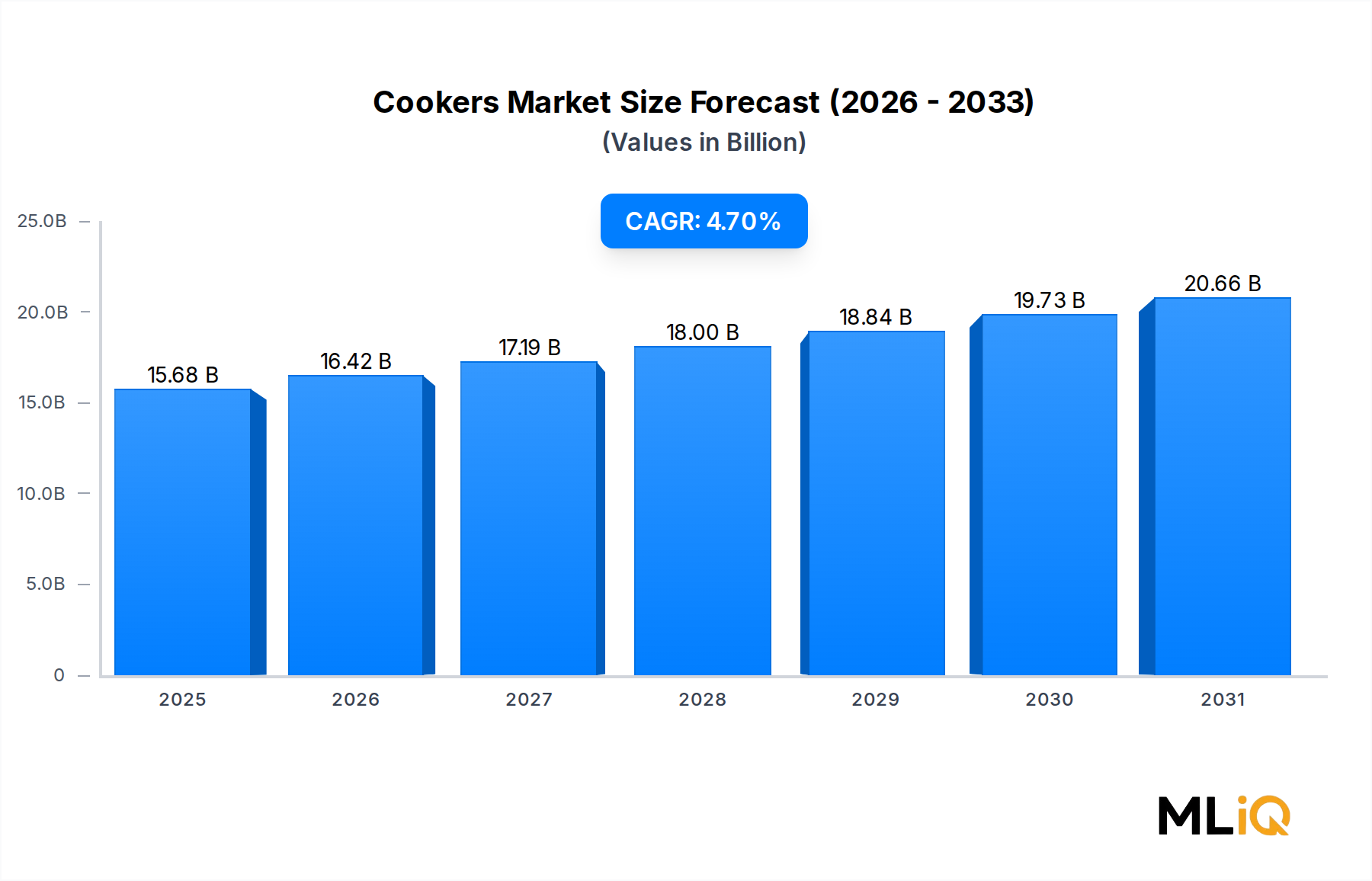

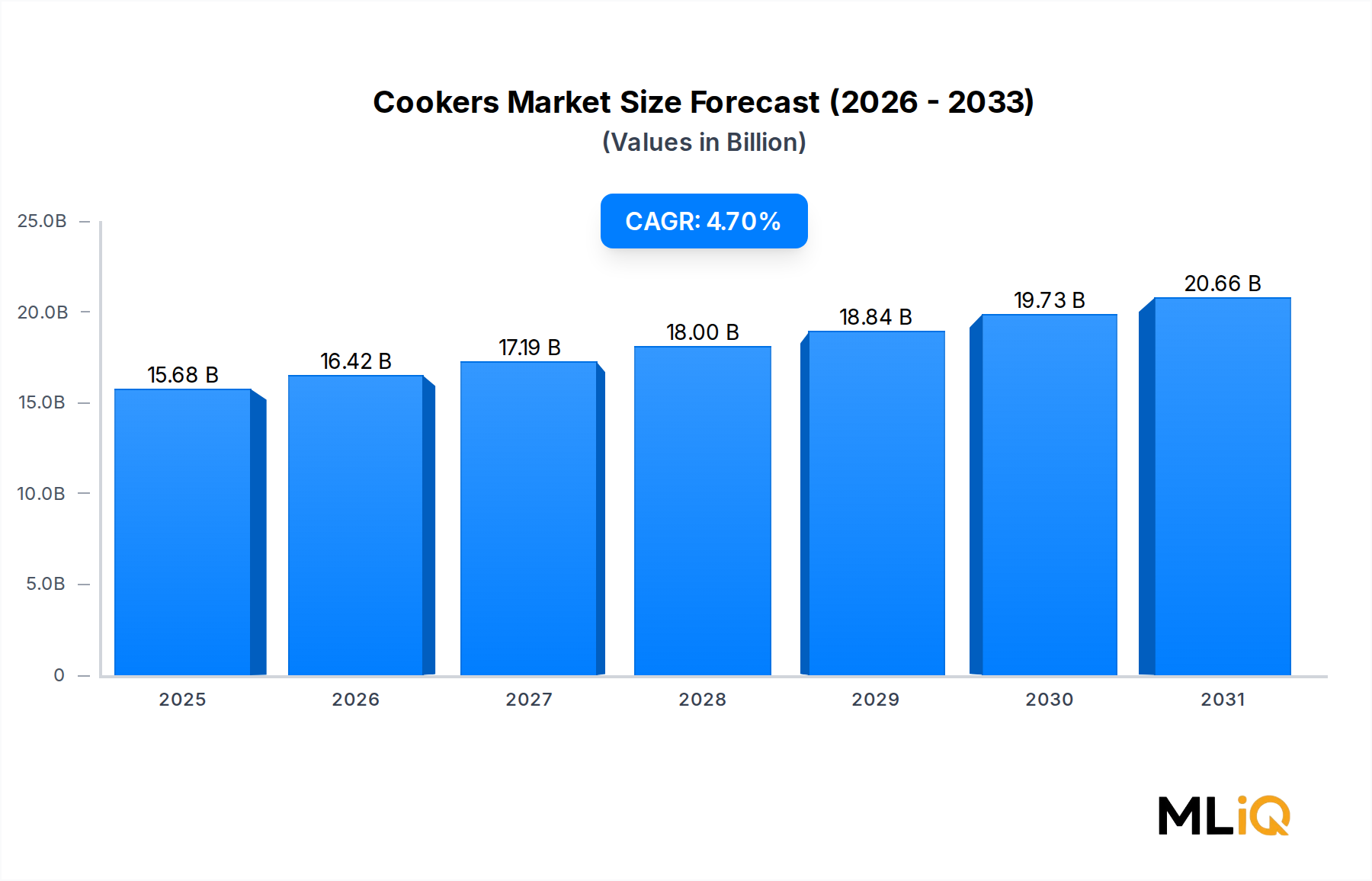

The global Cookers Market was valued at $15.68 billion in the base year and is projected to expand at a compound annual growth rate (CAGR) of 4.7% over the forecast period, reflecting sustained momentum across residential and commercial end-use segments. This growth trajectory is underpinned by an accelerating convergence of consumer demand for time-efficient cooking, rising urbanization rates, and the proliferation of smart kitchen technologies across mature and emerging economies alike.

Several macro tailwinds are reinforcing market expansion. First, global household formation rates—particularly in Asia Pacific and Sub-Saharan Africa—are driving appliance penetration into previously underserved demographics. Second, the post-pandemic normalization of home cooking habits has created a structural uplift in demand for versatile cooking appliances, particularly multi-function units capable of slow cooking, pressure cooking, and steaming within a single platform. Third, the rapid growth of online retail channels has dramatically lowered the cost of customer acquisition for mid-tier and premium brands, enabling greater geographic reach.

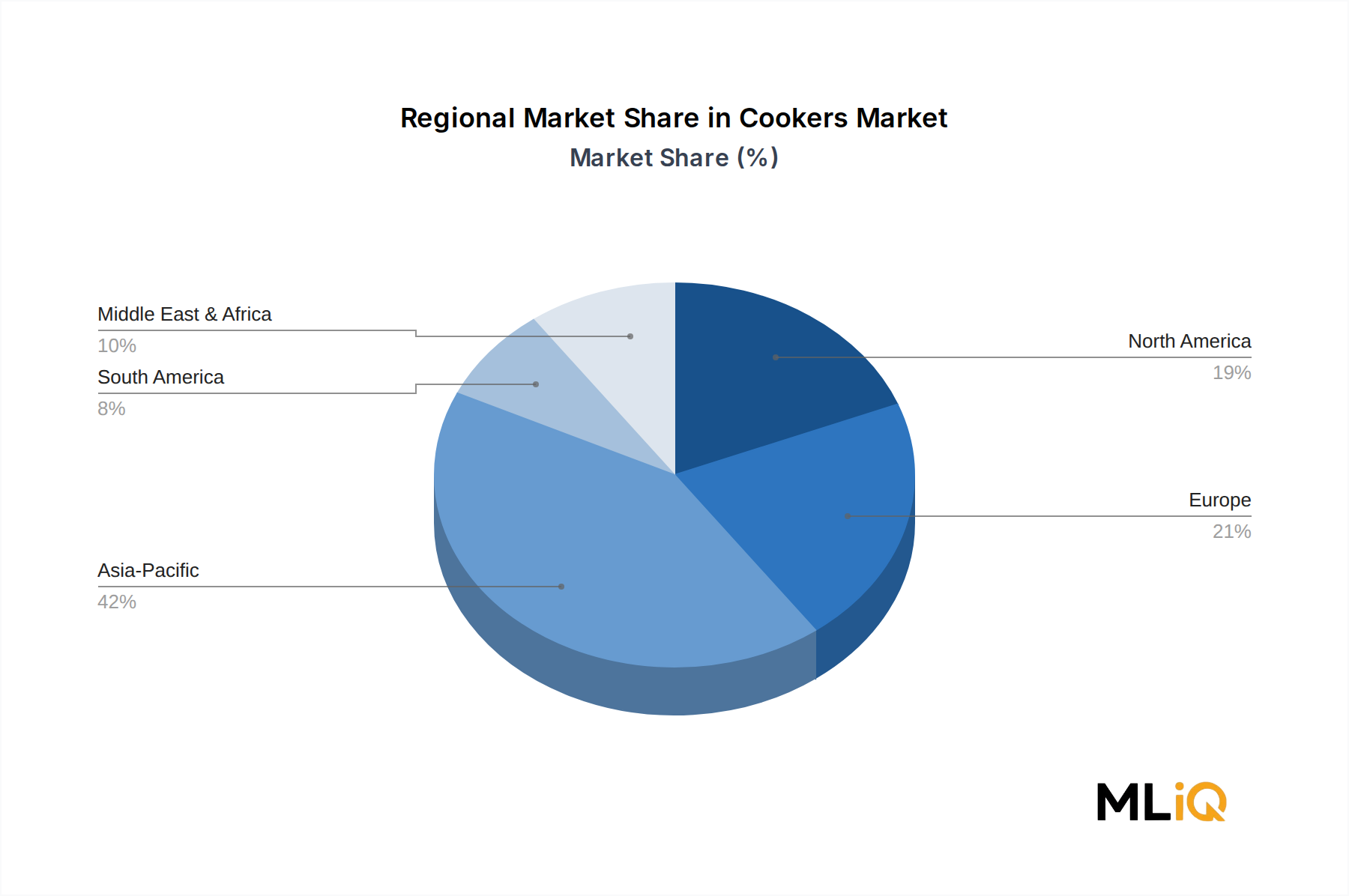

By 2030, the market is forecast to surpass a valuation commensurate with a 4.7% annualized growth rate applied from the $15.68 billion base, implying a market size approaching $22 billion under conservative assumptions. Revenue concentration remains highest in Asia Pacific, driven by entrenched rice cooker and pressure cooker cultures across China, India, and Southeast Asia. North America and Europe continue to represent high-value markets where premium positioning and smart connectivity features command significant average selling price premiums.

Product innovation is a central competitive differentiator. Leading manufacturers are investing heavily in IoT-enabled appliances that integrate with smart home ecosystems, offering programmable cooking cycles, remote monitoring, and AI-assisted recipe guidance. These features are increasingly standard in the premium segment, while functional improvements such as non-stick inner pots, stainless steel construction, and energy-efficient heating elements are filtering down to the mass market.

The competitive landscape features a mix of global conglomerates and regional specialists. Groupe SEB SA, Midea Group Co. Ltd., and TTK Prestige Limited anchor the upper tier, leveraging extensive distribution networks and strong brand equity. Meanwhile, niche players focused on specific product categories—such as Hawkins Cookers Limited in the pressure cooker segment—maintain loyal customer bases through consistent quality and value positioning.

Looking forward, the Cookers Market is expected to benefit from favorable demographic trends, rising disposable incomes in developing markets, and continued product category expansion. The multi cooker segment, in particular, represents the highest-growth sub-category as consumers seek consolidation of kitchen appliances to maximize counter space and utility.