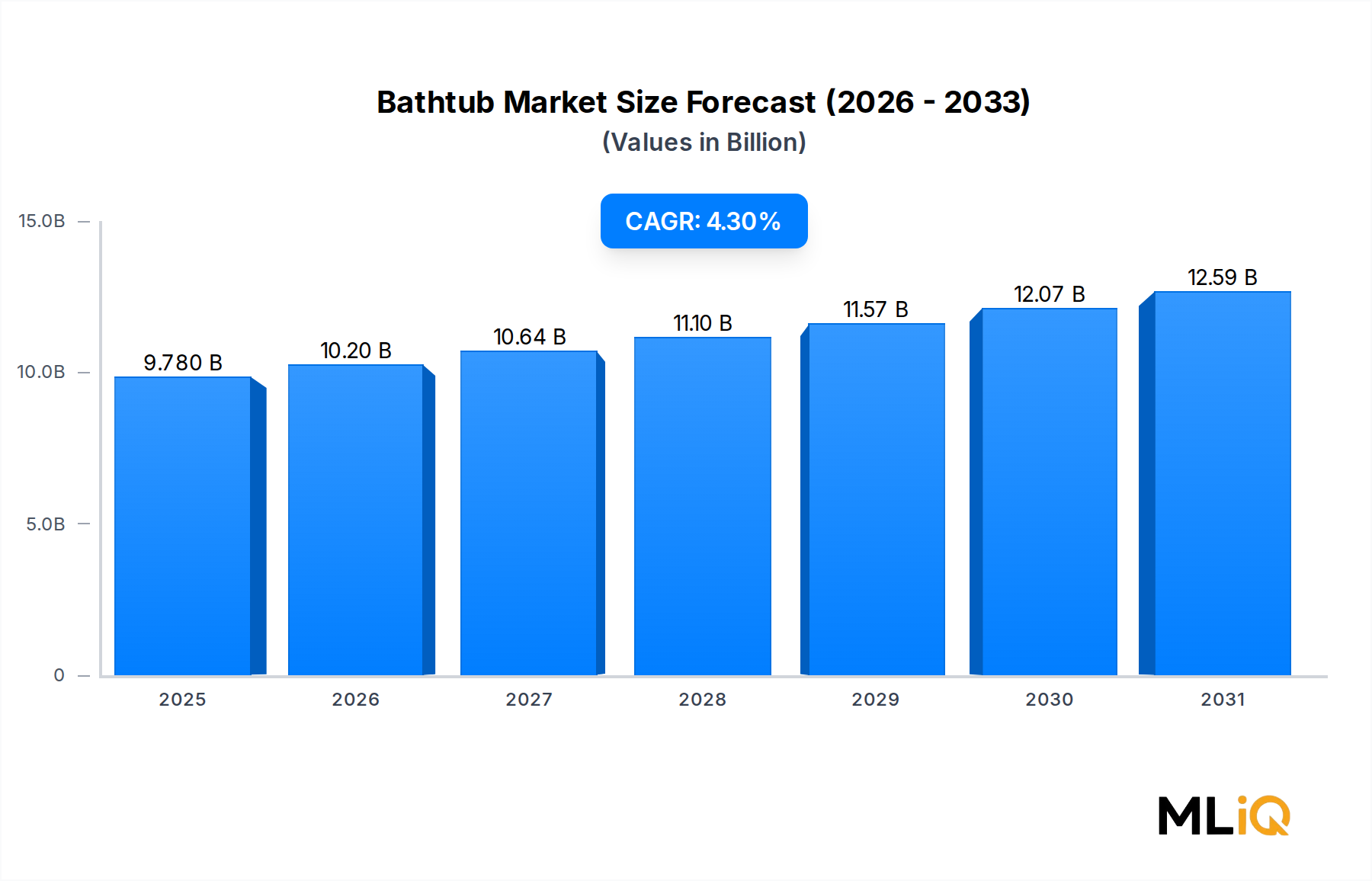

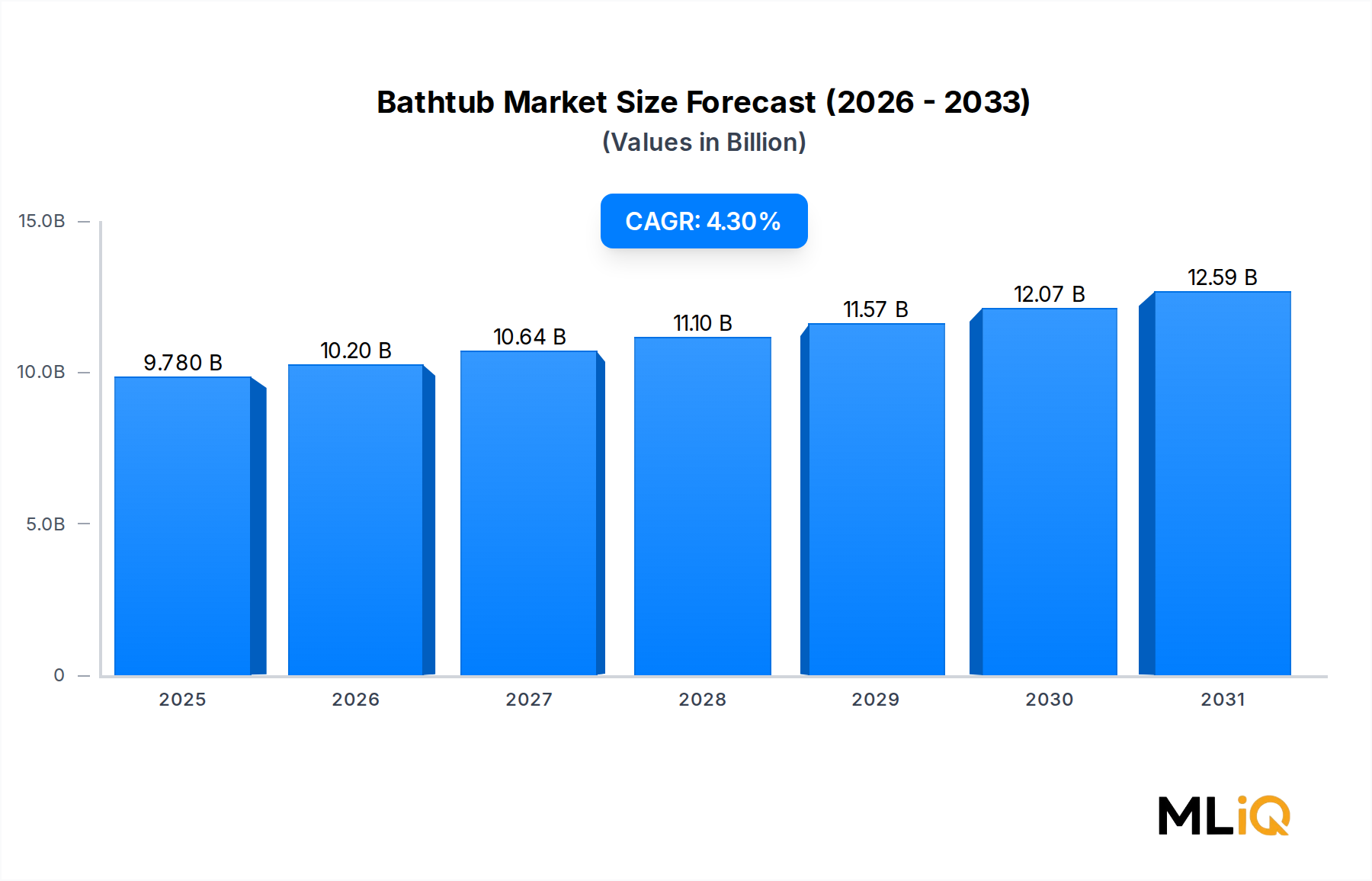

The Bathtub Market is shaped by a well-defined set of growth drivers and structural constraints, each with quantifiable dimensions that inform investment and operational strategy.

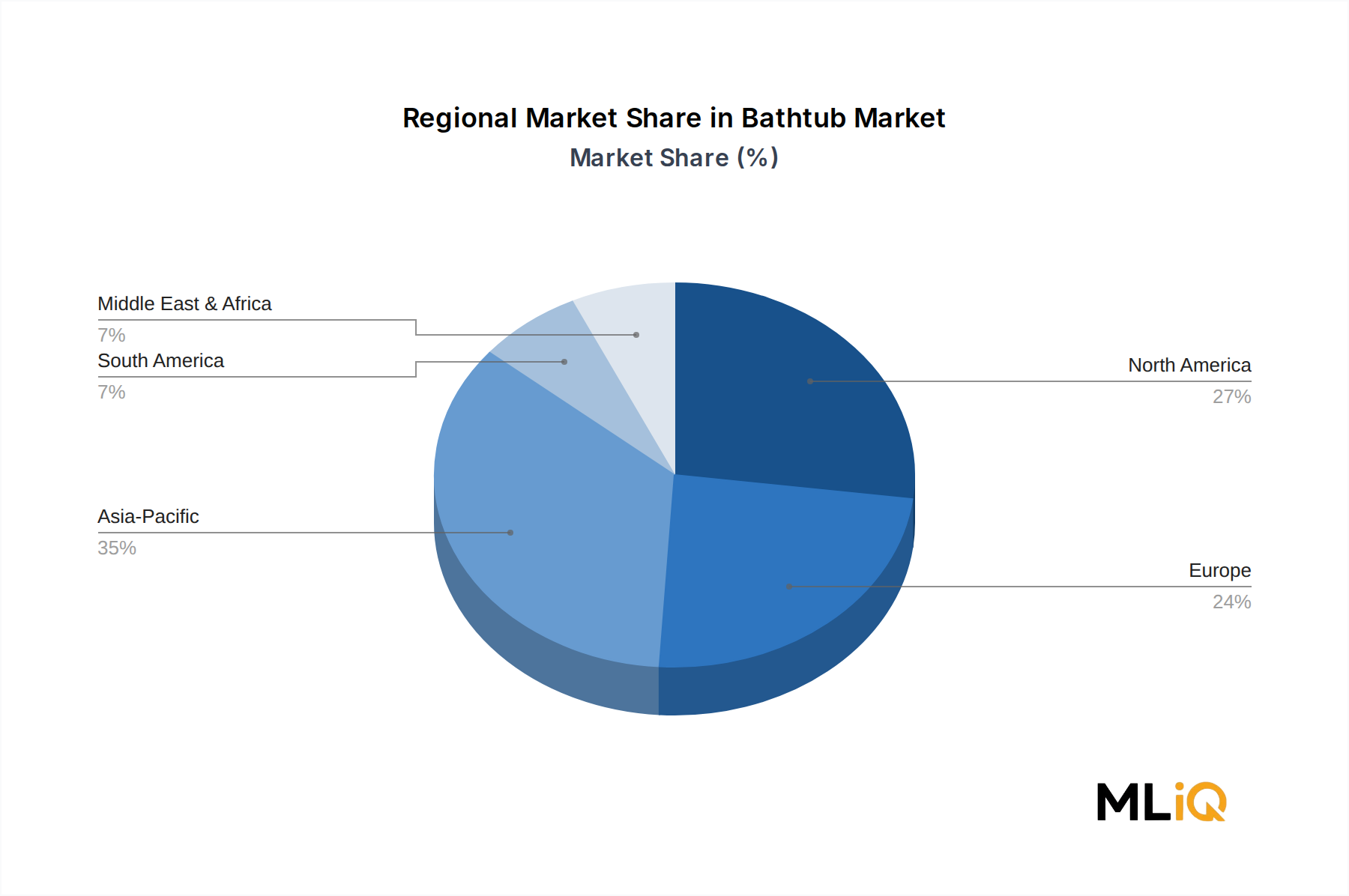

Residential construction and renovation activity is the primary demand driver. Global residential construction output has been recovering post-pandemic, with significant activity in Asia-Pacific markets where urbanization rates exceed 2% annually in countries such as India and Vietnam. In the United States alone, bathroom remodel completions have consistently ranked among the top three most common home improvement projects, with the National Association of Home Builders reporting over 10 million bathroom remodels annually in recent years. Each remodel represents a direct replacement opportunity for bathtub manufacturers.

The wellness and self-care megatrend is a structural tailwind. The global wellness economy, valued at over $5 trillion, has elevated the bathroom's role as a health and relaxation space. This has translated into measurable premiumization: average selling prices for bathtubs in the premium and ultra-premium tiers have grown at a rate exceeding the broader market CAGR, as consumers invest in hydrotherapy-enabled, chromotherapy-integrated, and ergonomically optimized designs.

Hospitality sector expansion is a significant commercial demand driver. The global hotel industry, recovering robustly post-2022, is increasing capital expenditure on guest bathroom upgrades to differentiate the in-room experience. Luxury and boutique hotel operators are specifying free-standing and spa-style bathtubs as standard, creating a reliable high-value B2B demand channel.

On the constraint side, raw material price volatility presents a persistent margin challenge. Acrylic resin, derived from petrochemical feedstocks, is subject to crude oil price cycles. Marble and stone materials face supply chain and logistics cost pressures. These input cost fluctuations compress manufacturer margins, particularly for mid-tier producers lacking the scale to absorb cost shocks.

Water scarcity concerns and regulatory pressure on water consumption in drought-affected regions—particularly parts of the United States, Australia, and Southern Europe—create headwinds for bathtub adoption relative to shower systems. Building codes in several jurisdictions increasingly mandate low-flow fixtures, and while this does not prohibit bathtubs, it raises the compliance cost for installation.

Labor costs for installation, which are disproportionately high for heavier or more complex bathtub formats, also constrain demand elasticity in cost-sensitive markets.