Within the product type segmentation of the Pump Coffee Machines Market, the automatic sub-segment — encompassing both semi-automatic and super-automatic (fully automatic) machines — commands the largest share of global revenue and continues to consolidate its leadership position. This dominance is attributable to a fundamental shift in consumer preference away from manual operation toward programmable, one-touch convenience, particularly among time-constrained urban professionals and households where multiple users require consistent output quality.

Super-automatic machines, which integrate a built-in burr grinder, automated tamping, brewing, and milk frothing functions into a single unit, have seen the most pronounced growth within this sub-segment. These devices eliminate the skill barrier associated with manual espresso preparation, democratizing access to café-quality beverages. The typical retail price range for super-automatic units spans from approximately $400 to over $3,000, creating a wide addressable consumer band that stretches from mass-market aspirational buyers to premium enthusiasts.

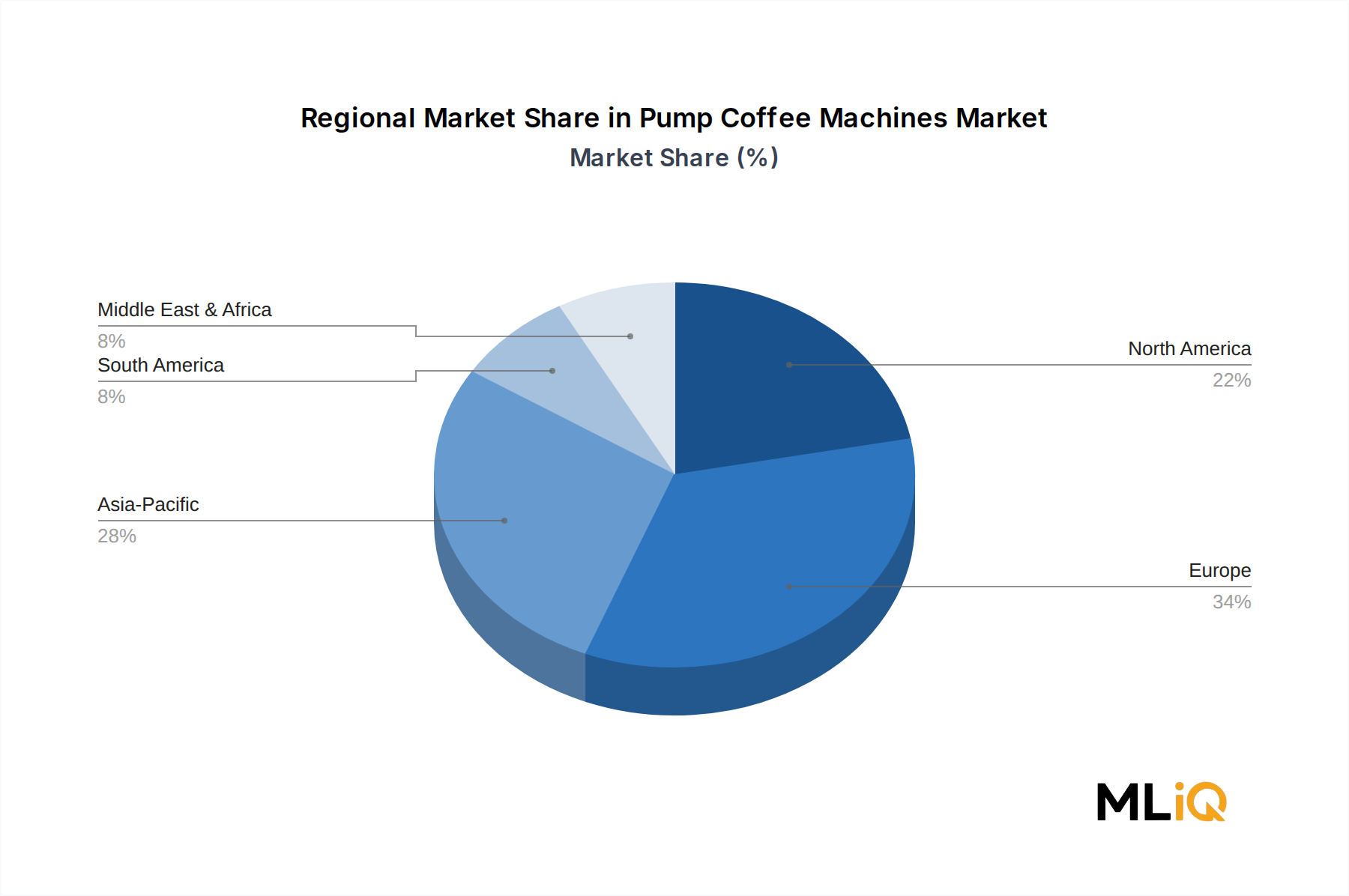

Semi-automatic machines occupy a slightly different value proposition, offering the control and ritual associated with manual preparation while automating the pressure delivery and pump mechanism. This segment is particularly strong in Europe, where espresso culture is entrenched and consumers exhibit higher willingness to invest in the preparation process itself. Countries such as Italy, Germany, and France account for a disproportionate share of semi-automatic unit sales relative to their population sizes.

Key players are competing aggressively within the automatic segment on the basis of proprietary brewing algorithms, patented milk-frothing technologies, and connected app ecosystems. De' Longhi SpA has extended its leadership through its Dinamica and Eletta product lines, both of which feature its LatteCrema milk system and are compatible with the De' Longhi Coffee Link app. Sage Appliances (marketed as Breville in non-European markets) competes on precision engineering credentials, offering adjustable pre-infusion, temperature control to within ±1°C, and barista-grade portafilter compatibility. Philips leverages its LatteGo system and broad retail footprint to maintain strong volume share in the mid-tier automatic segment.

The competitive dynamics within the automatic segment are also being shaped by the emergence of AI-assisted brewing personalization. Machines equipped with machine learning capabilities can now adapt grind coarseness, extraction time, and water temperature based on user feedback loops — a feature set that is becoming a key differentiator in the $1,000–$2,500 price band. Groupe SEB, through its Krups and Rowenta subsidiaries, has accelerated investment in this area, aiming to capture premium share from incumbent leaders.

From a distribution standpoint, the automatic segment benefits disproportionately from online retail channels, where detailed product specifications, video demonstrations, and customer review ecosystems lower the information asymmetry that previously favored in-store purchases for high-consideration products. The shift to online purchasing, accelerated by the 2020–2021 pandemic period, has not meaningfully reversed, with online channels now accounting for an estimated 38–42% of automatic machine sales globally.

The automatic segment's share is not merely large — it is expanding. As manufacturing efficiencies and component standardization drive down the cost of integrating automated functions, price points are gravitating downward, pulling previously price-excluded consumer cohorts into the category. This dynamic is expected to sustain the segment's revenue leadership through the 2033 forecast horizon.