1. What are the major growth drivers for the Polyaspartic Coatings Market market?

Factors such as are projected to boost the Polyaspartic Coatings Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

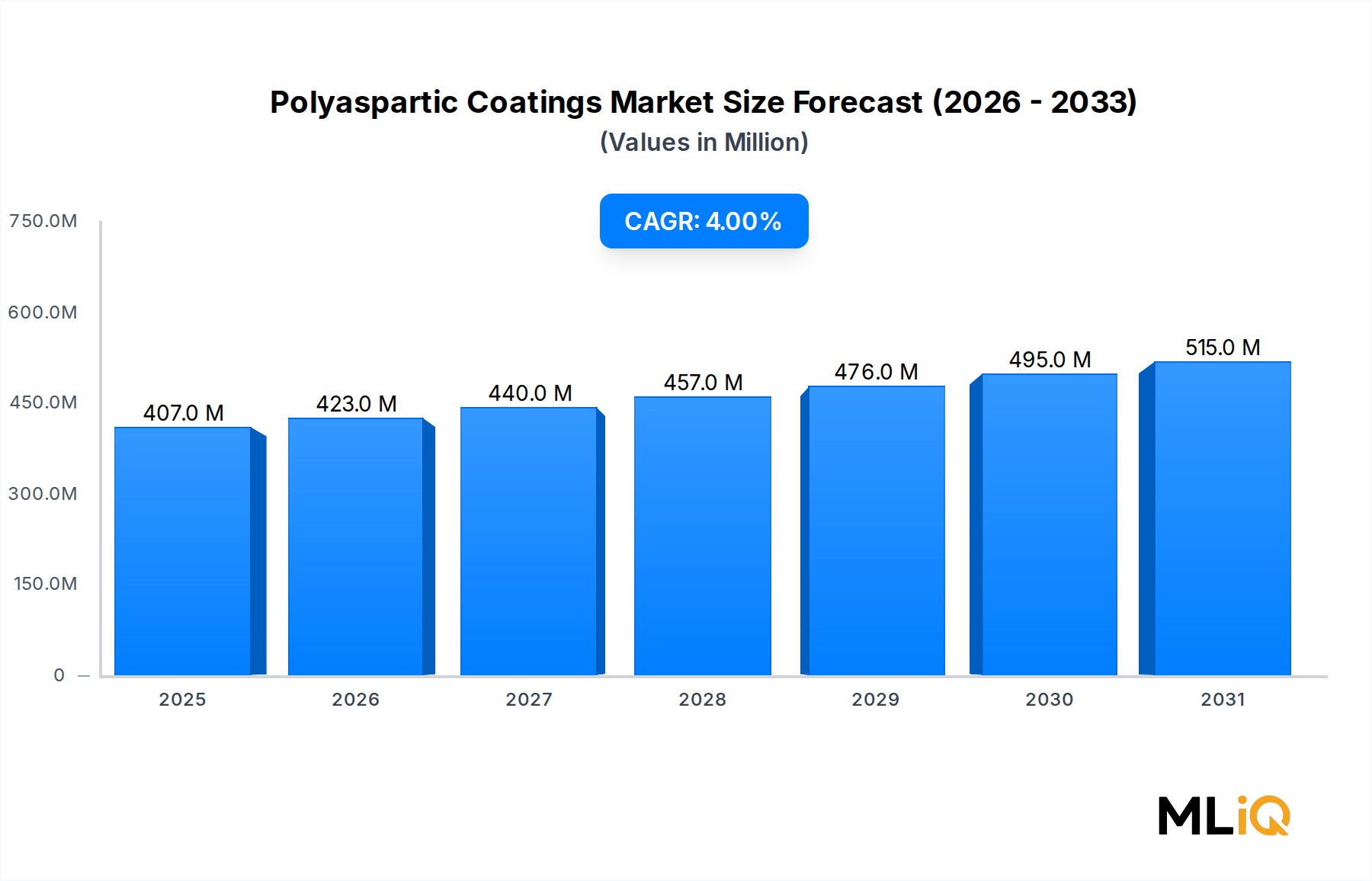

The global Polyaspartic Coatings Market is valued at $406.64 million as of the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 4% through 2033, reflecting steady demand driven by construction activity, infrastructure rehabilitation, and industrial floor protection requirements. Polyaspartic coatings, derived from the reaction of aliphatic polyisocyanates with polyaspartic acid esters, have established themselves as a high-performance alternative to conventional epoxy and polyurethane systems, offering superior UV resistance, rapid cure times, and broad temperature application windows.

Macro tailwinds underpinning this trajectory include rising global infrastructure spending, growing regulatory pressure to reduce volatile organic compound (VOC) emissions from industrial coatings, and an accelerating shift toward high-solids and solvent-free formulations in commercial and residential flooring applications. The building and construction sector remains the single most significant demand engine, accounting for a dominant revenue share, as polyaspartic chemistries are increasingly specified for garage floors, warehouse decking, stadium concourses, and bridge decks.

From an application standpoint, the 100% solids segment is gaining disproportionate traction as applicators seek zero-VOC compliance and faster return-to-service timelines, particularly in the transportation and power generation sub-verticals. Hybrid formulations, which blend polyaspartic chemistry with epoxy or urethane intermediates, continue to serve cost-sensitive projects where performance trade-offs are acceptable.

Geographically, North America commands the largest revenue share, supported by a mature construction renovation cycle, active military and federal infrastructure programs, and a well-developed network of professional applicators. Asia Pacific is emerging as the fastest-growing regional market, propelled by rapid urbanization in China, India, and ASEAN economies, alongside expanding manufacturing and logistics infrastructure requiring durable floor protection.

Key competitive dynamics are shaped by a blend of global specialty chemical conglomerates and nimble regional formulators. Companies such as BASF SE, Covestro AG, PPG Industries, AkzoNobel, and The Sherwin-Williams Company compete on formulation depth, raw material integration, and technical service capabilities, while regional players such as Resinwerks and IndMar Coatings Corporation compete on application expertise and turnaround flexibility.

Looking forward through 2033, the market outlook is constructive. Continued product innovation targeting self-leveling, anti-static, and antimicrobial variants, combined with growing awareness of life-cycle cost advantages over conventional coatings, is expected to sustain the 4% CAGR trajectory and push the market toward an estimated $550–$580 million valuation range by the end of the forecast period.

Among all end-use verticals served by the Polyaspartic Coatings Market, the building and construction segment commands the highest revenue share and is expected to maintain its leadership position throughout the 2025–2033 forecast window. This dominance is rooted in a convergence of technical performance advantages, favorable regulatory trends, and secular demand for durable, aesthetically superior floor and surface protection systems across residential, commercial, and institutional construction projects.

Polyaspartic coatings address one of the most persistent pain points in construction finishing: the need to apply, cure, and return a surface to service within compressed project timelines. Unlike conventional epoxy coatings that require 24–72 hours of cure time depending on ambient temperature, polyaspartic systems can achieve full pedestrian traffic readiness in as little as 2–4 hours and vehicular traffic readiness within 24 hours, even in low-temperature conditions approaching -25°C. This characteristic makes them particularly attractive for renovation and retrofit projects in occupied facilities, where downtime carries direct economic consequences.

Within building and construction, the commercial flooring sub-segment — encompassing retail showrooms, healthcare facilities, educational campuses, and logistics warehouses — represents the highest-value application cluster. The growth of e-commerce-driven warehouse construction across North America and Europe has created sustained demand for high-performance floor systems capable of withstanding heavy forklift traffic, chemical spills, and thermal cycling. Polyaspartic top-coat systems, often applied over epoxy base coats in a hybrid architecture, are increasingly the specification of choice for such environments.

Residential garage floor coatings represent another high-growth niche within the building and construction segment. Consumer awareness of polyaspartic chemistry — driven by social media content, home improvement programming, and contractor marketing — has elevated polyaspartic systems beyond the professional-only channel into the prosumer and DIY retail market. Companies such as Rust-Oleum Corporation have successfully commercialized one-component and simplified two-component polyaspartic kits targeting the residential consumer segment, broadening the addressable market considerably.

Bridge decks, parking structures, and stadium concourses represent the infrastructure sub-segment, where polyaspartic coatings compete directly with conventional polyurethane and epoxy coal-tar formulations on the basis of UV stability, crack-bridging flexibility, and chemical resistance. Public sector procurement cycles in North America, supported by infrastructure legislation allocating substantial funding to bridge and highway rehabilitation, are creating multi-year demand visibility for polyaspartic manufacturers with certified systems in these applications.

Key players driving revenue in the building and construction segment include BASF SE, which leverages its Desmodur isocyanate portfolio to support formulation development; PPG Industries, which distributes polyaspartic systems through its professional contractor network; and LATICRETE International Inc., which integrates polyaspartic chemistry into its broader tile and flooring installation ecosystem. AkzoNobel and The Sherwin-Williams Company compete through specification pull strategies targeting architecture and design communities.

The segment's share is consolidating rather than fragmenting, as increasing technical complexity — particularly around application temperature windows, pot life management, and compatibility with concrete surface profiles — favors experienced, well-resourced formulators over commodity suppliers. This dynamic is reinforcing the competitive position of established players and creating barriers to entry for new market participants.

Several well-defined demand drivers and structural constraints shape the growth trajectory of the Polyaspartic Coatings Market and must be analyzed with quantitative grounding to avoid mischaracterizing market dynamics.

On the demand side, VOC regulatory pressure is arguably the most consequential structural driver. Regulatory frameworks in the United States — particularly California's South Coast Air Quality Management District (SCAQMD) Rule 1113 — and analogous European Union directives under the Decorative Paints Directive (2004/42/EC) are progressively tightening permissible VOC limits for architectural and industrial coatings. Polyaspartic 100% solids formulations, which emit negligible or zero VOCs during application, are direct beneficiaries of this regulatory trajectory. As conventional solvent-borne systems face reformulation costs or market access restrictions, polyaspartic alternatives gain competitive parity on a total cost-of-compliance basis.

Infrastructure investment cycles represent a second quantifiable driver. The U.S. Infrastructure Investment and Jobs Act (IIJA), signed into law in November 2021, allocated $1.2 trillion in total infrastructure spending over a five-year horizon, with meaningful allocations to bridge rehabilitation, highway resurfacing, and public building renovation — all high-affinity applications for polyaspartic protective coatings. Similar infrastructure stimulus programs in the European Union and GCC countries are creating analogous demand impulses.

Rapid cure time economics constitute a third driver. Studies by flooring contractors document that polyaspartic systems reduce project cycle times by 30–50% relative to epoxy alternatives on commercial floor projects, translating directly into higher applicator throughput and margin expansion. This economic incentive is accelerating adoption among professional flooring contractors.

On the constraint side, raw material cost volatility poses the most significant headwind. Polyaspartic coatings are derivative of aliphatic diisocyanate chemistry, particularly hexamethylene diisocyanate (HDI) and isophorone diisocyanate (IPDI), which are produced by a concentrated group of global chemical manufacturers. Supply disruptions — such as those experienced during the 2020–2022 global supply chain dislocation — caused HDI spot prices to spike by 40–60%, compressing formulator margins and triggering price increases passed to end users.

Application skill barriers represent a second constraint. Polyaspartic systems require precise mixing ratios, surface preparation to SSPC SP-6 or better standards, and humidity and temperature monitoring during application. Shortage of certified applicators in emerging markets limits geographic penetration.

The competitive landscape of the Polyaspartic Coatings Market is characterized by a tiered structure comprising global specialty chemical manufacturers, diversified coatings conglomerates, and focused regional formulators. The following profiles capture the strategic positioning of the ten principal participants identified in the market dataset.

IndMar Coatings Corporation: A specialized formulator focused on high-performance polyaspartic and polyurea systems for commercial and industrial flooring, IndMar competes on technical application depth and regional contractor partnership networks rather than broad distribution scale.

BASF SE: One of the world's largest chemical companies, BASF provides core polyaspartic intermediates — including aliphatic polyisocyanates under its Desmodur brand — to both internal formulation units and third-party customers, giving it upstream influence across the entire value chain.

PPG Industries: A global coatings leader, PPG distributes polyaspartic flooring and protective coating systems through its industrial and architectural channels, leveraging its extensive contractor network and specification relationships to drive volume across North America and Europe.

AkzoNobel: Through its Performance Coatings division, AkzoNobel markets polyaspartic-based protective coatings for marine, infrastructure, and industrial maintenance applications, competing on global brand equity and formulation innovation.

LATICRETE International Inc.: Focused on the construction materials segment, LATICRETE integrates polyaspartic chemistry into its flooring installation system portfolio, targeting the tile, stone, and specialty flooring professional contractor community.

Covestro AG: A leading supplier of high-performance polymers and isocyanate raw materials, Covestro supplies aliphatic diisocyanate building blocks essential to polyaspartic formulation, making it a critical upstream partner and indirect competitive force across the market.

The Sherwin-Williams Company: With one of the largest professional coatings distribution networks in the world, Sherwin-Williams markets polyaspartic floor coating systems through its industrial and protective coatings segment, supported by technical specification programs targeting architects, engineers, and facility managers.

Rust-Oleum Corporation: A subsidiary of RPM International, Rust-Oleum has democratized polyaspartic coatings through consumer-accessible product lines sold via home improvement retail, significantly expanding the residential garage floor segment.

Resinwerks: A mid-size specialty formulator with deep expertise in commercial and industrial flooring chemistries, Resinwerks competes through technical differentiation, custom color capability, and strong relationships with flooring contractors in North America.

SIKA AG: A globally diversified construction chemicals company, SIKA offers polyaspartic coating systems within its broader flooring and waterproofing portfolio, leveraging project engineering capabilities and global construction site presence to drive specification and volume.

January 2023: BASF SE announced expanded production capacity for aliphatic diisocyanates at its Schwarzheide, Germany facility, targeting growing demand from the high-performance coatings sector, including polyaspartic formulations, with an investment of approximately €100 million.

March 2023: Covestro AG launched a new bio-based aliphatic isocyanate intermediate targeting polyaspartic and polyurethane coating applications, aligned with its "Sustainable Future" strategic roadmap and designed to reduce formulated coating carbon footprint by up to 20%.

June 2023: The Sherwin-Williams Company expanded its industrial protective coatings portfolio with a new generation of fast-cure polyaspartic topcoat systems targeting the transportation infrastructure vertical, specifically bridge deck and parking structure rehabilitation.

September 2023: PPG Industries entered a strategic supply agreement with a major U.S. logistics real estate developer to supply polyaspartic floor coating systems across a portfolio of 15+ new distribution center construction projects in North America.

February 2024: AkzoNobel announced R&D investment in waterborne polyaspartic hybrid technologies at its innovation center in Sassenheim, Netherlands, targeting European regulatory compliance markets and seeking to achieve performance parity with solvent-borne systems.

May 2024: SIKA AG completed the acquisition of a regional specialty flooring coatings company in Southeast Asia, strengthening its polyaspartic and epoxy flooring product presence across the ASEAN growth corridor.

November 2024: Rust-Oleum Corporation introduced a single-day application-and-cure polyaspartic garage floor kit targeting the consumer DIY channel, achieving national retail placement across major home improvement retailers ahead of the 2025 spring selling season.

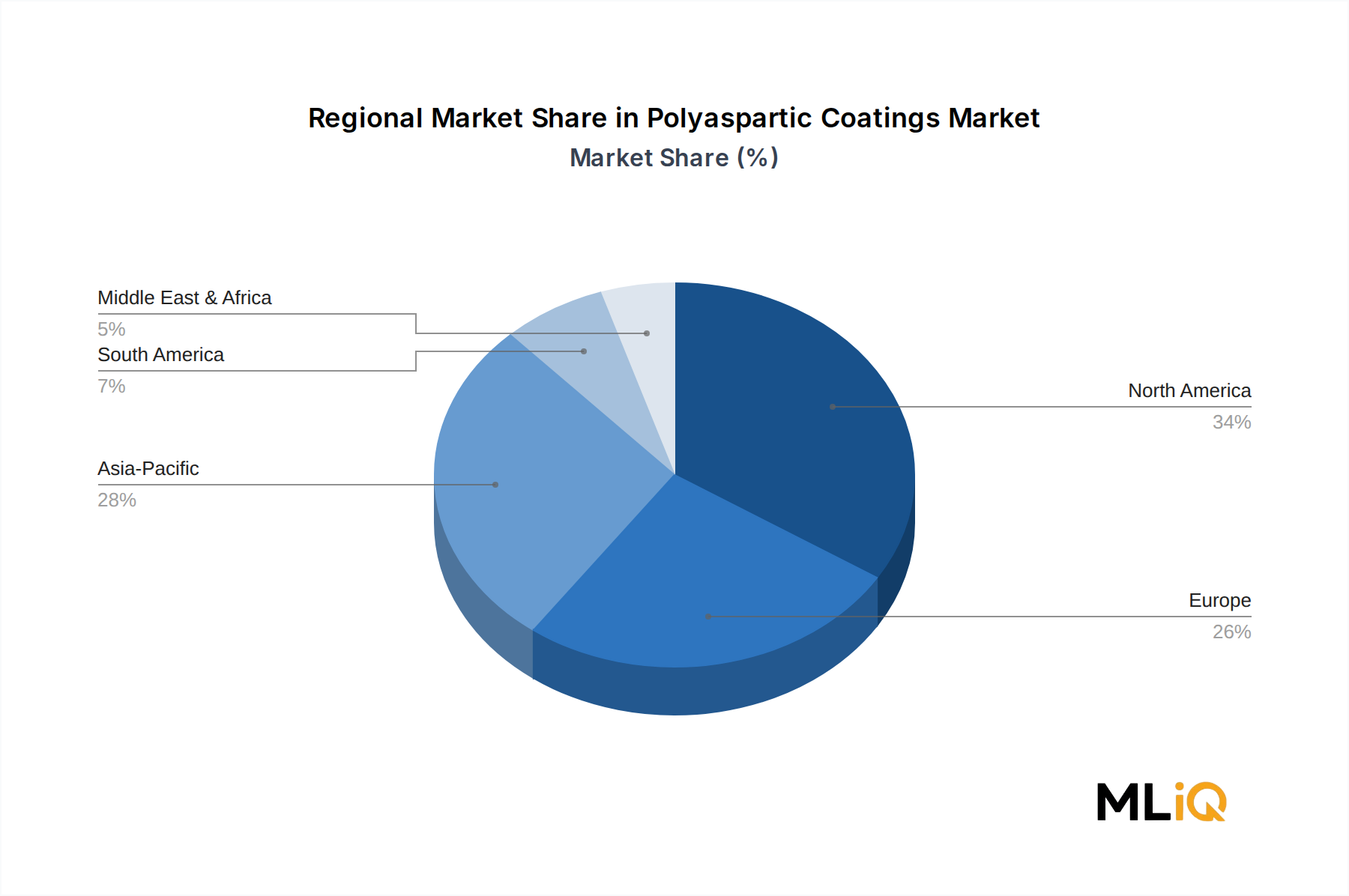

The Polyaspartic Coatings Market exhibits meaningful regional differentiation in terms of growth rates, revenue contribution, and primary demand drivers, reflecting divergent construction cycles, regulatory environments, and industrial infrastructure maturity profiles.

North America represents the most mature and largest revenue-generating region, accounting for an estimated 38–42% of global market revenue. The United States is the dominant national market within the region, supported by active federal and state infrastructure rehabilitation programs, a mature professional flooring contractor ecosystem, and among the most stringent VOC regulatory frameworks globally. The IIJA-related pipeline of bridge, highway, and public facility projects is expected to sustain elevated demand through 2027–2028. Canada and Mexico contribute incrementally, with Mexico showing above-average growth tied to nearshoring-driven industrial construction.

Europe holds the second-largest revenue position, estimated at 28–32% of global market share. Germany, the United Kingdom, France, and the Nordic countries are the primary demand markets, driven by renovation activity in commercial real estate, EU sustainability directives pushing adoption of low-VOC coatings, and robust automotive and manufacturing facility construction. Russia's contribution has declined materially following 2022 geopolitical developments and associated supply chain realignments.

Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR of approximately 5.5–6.5% through 2033, outpacing the global average. China remains the largest national contributor within the region, driven by logistics infrastructure, electric vehicle manufacturing facility construction, and government-supported industrial park development. India is emerging as a high-growth secondary market, with rapidly expanding warehousing, pharmaceutical, and food processing facility construction driving polyaspartic floor coating demand. ASEAN economies, particularly Vietnam, Thailand, and Indonesia, are benefiting from manufacturing investment redirection and present greenfield opportunity for market participants.

The Middle East and Africa region, anchored by GCC countries — particularly Saudi Arabia and the UAE — represents a growing opportunity market tied to Vision 2030-aligned megaprojects, new city construction, and industrial diversification initiatives. South America, led by Brazil and Argentina, is a smaller but incrementally growing market, constrained by economic volatility and currency risk but supported by agricultural processing infrastructure and mining sector demand for protective coatings.

Technology innovation in the Polyaspartic Coatings Market is advancing along three primary vectors: waterborne polyaspartic formulations, bio-based raw material integration, and smart or functional coating capabilities. Each trajectory carries distinct implications for incumbent business models and competitive positioning.

Waterborne polyaspartic hybrids represent the most commercially proximate innovation frontier. Traditional polyaspartic systems rely on solvent-free 100% solids chemistry or low-solvent formulations, but the development of stable waterborne polyaspartic dispersions opens new regulatory-compliant pathways for application in highly sensitive environments such as occupied healthcare facilities and food production spaces.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Polyaspartic Coatings Market market expansion.

Key companies in the market include IndMar Coatings Corporation, BASF SE, PPG Industries, AkzoNobel, LATICRETE International Inc., Covestro AG, The Sherwin-Williams Company, Rust-Oleum Corporation, Resinwerks, SIKA AG.

The market segments include Type, End-use Industry.

The market size is estimated to be USD 406.64 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Polyaspartic Coatings Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Polyaspartic Coatings Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.