1. What are the major growth drivers for the Kraft Lignin Products Industry market?

Factors such as ; Rising Demand for Carbon Fibers are projected to boost the Kraft Lignin Products Industry market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

Kraft Lignin Products Industry

Kraft Lignin Products Industry+1 2315155523

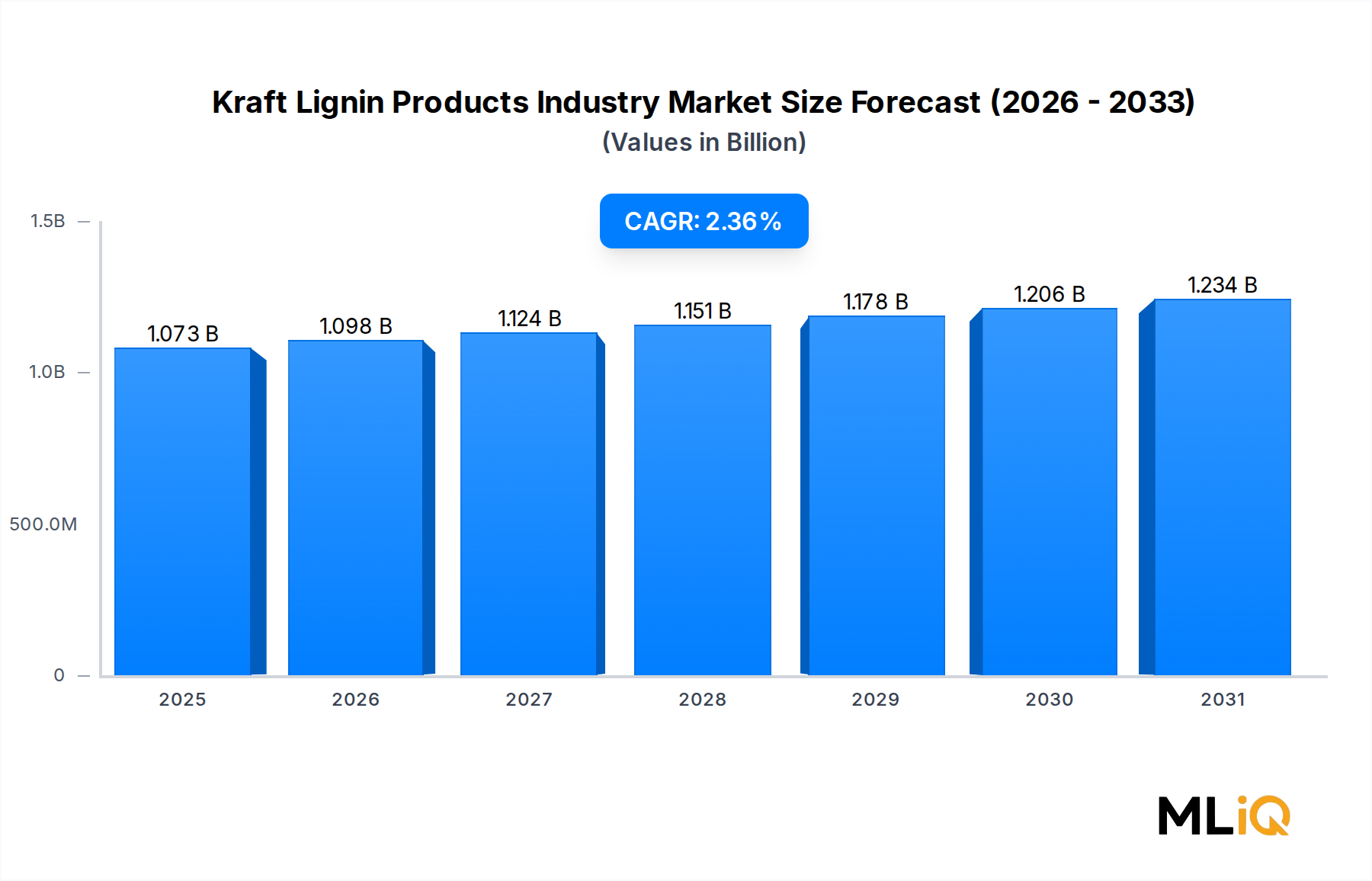

The global Kraft Lignin Products Industry Market is valued at approximately $1,072.51 million in 2025, the designated base year for this analysis. Projecting forward through 2033, the market is forecast to expand at a compound annual growth rate (CAGR) of 2.37%, reflecting steady but measured growth across its diversified application portfolio. While the headline CAGR appears moderate compared to high-growth specialty chemical sectors, the underlying demand dynamics are structurally robust, underpinned by a global push toward bio-based and circular economy solutions.

Kraft lignin, a byproduct of the kraft pulping process in the pulp and paper industry, has historically been combusted for energy recovery within pulp mills. However, advances in extraction, purification, and functionalization technologies have unlocked its commercial potential across a spectrum of value-added applications. These include carbon fibers, activated carbon, phenol derivatives, binders and resins, and fertilizer adjuvants, among others. The transition from a low-value byproduct to a high-value feedstock is the central demand driver reshaping this market through the forecast horizon.

Rising demand for sustainable alternatives to petroleum-derived chemicals is a principal macro tailwind. Regulatory frameworks in Europe, North America, and parts of Asia Pacific are incentivizing bio-based chemical adoption, reducing carbon footprints, and discouraging single-use petrochemical derivatives. These policies are directly expanding the addressable market for kraft lignin derivatives.

The carbon fiber application segment stands out as a particularly dynamic growth vector. With lightweighting requirements intensifying across automotive, aerospace, and wind energy sectors, lignin-based carbon fiber has emerged as a cost-competitive alternative to polyacrylonitrile (PAN)-based carbon fiber. This sub-segment is attracting significant research and development investment from both established pulp producers and specialty chemical companies.

From a competitive standpoint, the market is moderately consolidated, with large integrated pulp and paper companies retaining significant upstream advantages. However, emerging biochemical startups and research-backed spin-offs are increasing competitive pressure in higher-margin application niches.

Geographically, Europe leads in both market share and regulatory sophistication, while Asia Pacific represents the fastest-growing regional opportunity due to expanding industrial output and increasing bio-economy policy support in China, India, and South Korea. North America remains a key innovation hub, particularly in lignin valorization technologies.

Looking ahead to 2033, the market is anticipated to approach approximately $1,290 million, contingent on continued commercialization of lignin-to-carbon-fiber pathways, expanded agricultural applications, and scale-up of bio-refinery infrastructure. Investment in upstream extraction efficiency and downstream formulation capabilities will be critical to sustaining this trajectory.

Among all application segments tracked within the Kraft Lignin Products Industry Market, binders and resins represent the single largest revenue-generating category. This dominance is attributable to the chemical versatility of lignin macromolecules, their inherent adhesive properties, and the well-established commercial precedent for lignin-based binders in wood panel manufacturing, foundry sand casting, and pellet production.

Lignin's aromatic structure, rich in phenolic hydroxyl and aliphatic hydroxyl groups, makes it a natural candidate for substituting formaldehyde-based phenol-formaldehyde (PF) resins. In wood composite panels — including medium-density fiberboard (MDF), particleboard, and oriented strand board (OSB) — lignin-based binders offer a pathway to significantly reduced formaldehyde emissions, a critical regulatory compliance driver in markets governed by CARB (California Air Resources Board) Phase II standards and the European REACH regulation.

The global wood panel manufacturing sector consumes millions of metric tons of synthetic binders annually. Even partial substitution of PF resins with kraft lignin-derived alternatives translates into substantial volumetric demand. Leading producers such as Stora Enso and Borregaard Lignotech have made significant investments in scaling up lignin binder product lines, targeting wood panel manufacturers in Europe and North America as primary customers.

In foundry applications, lignosulfonate-based binders — a closely adjacent product to kraft lignin derivatives — have long been used as core sand binders. Kraft lignin's utility in this space is growing as producers refine fractionation processes to deliver consistent molecular weight distributions, which are essential for predictable binding performance under high-temperature casting conditions.

From a competitive standpoint, the binders and resins segment features both large integrated producers and mid-tier specialty chemical formulators. Domtar Corporation, Rayonier Advanced Materials, and UPM Biochemicals are among the key participants with active product development programs in this category. These companies leverage their kraft pulping operations to secure a cost-advantaged lignin feedstock supply, creating a structural barrier for pure-play chemical companies attempting to enter the space.

The segment's revenue share is assessed to be consolidating rather than expanding, as downstream customers increasingly demand standardized, application-specific lignin grades rather than commodity bulk material. This trend is accelerating vertical integration among large producers, who are building formulation and application testing capabilities to retain customer relationships and command premium pricing.

Investment in bio-based binder certification schemes — such as those administered by the Forest Stewardship Council (FSC) and emerging EU Green Deal procurement frameworks — is further entrenching kraft lignin binders as a preferred solution in sustainability-conscious supply chains. Panel manufacturers operating in export markets with stringent emission regulations represent the most price-inelastic buyer segment, ensuring sustained revenue floors for the dominant binders and resins category throughout the forecast period.

Technological advancements in lignin depolymerization and re-polymerization are beginning to unlock application extensions within the resins category, including epoxy resin partial substitutes and polyurethane precursors. These adjacencies, while still at pilot or early commercial scale, represent incremental revenue opportunities that could further reinforce the segment's leadership position by 2030.

The primary demand driver for the Kraft Lignin Products Industry Market is the intensifying global interest in carbon fiber production using bio-based precursors. Traditional carbon fiber manufacturing relies predominantly on polyacrylonitrile (PAN), a petroleum-derived polymer that accounts for approximately 51% of final carbon fiber production costs. Lignin-based carbon fiber precursors have been demonstrated to reduce raw material costs by an estimated 30–40% under optimized processing conditions, a figure that has attracted both government-funded research programs and private capital in the United States, Germany, Finland, and Japan. Rising demand for carbon fiber in wind turbine blades, electric vehicle structural components, and aerospace interiors is therefore a high-impact indirect driver for kraft lignin offtake volumes.

Increasing demand for fertilizers and pesticides formulated with biostimulant lignin additives represents a second demand driver. Lignin-based slow-release fertilizer coatings and chelating agents are gaining traction among precision agriculture practitioners seeking to reduce nutrient runoff and improve nitrogen use efficiency. With global fertilizer markets under price pressure following geopolitical supply disruptions, the cost-effectiveness of lignin additives has improved in relative terms.

On the restraint side, stringent government regulations, while generally supportive of bio-based chemistry, impose compliance costs and testing requirements that can delay product commercialization. In the European Union, regulatory classification of novel lignin-derived compounds under REACH necessitates extensive toxicological dossiers. Additionally, inconsistency in lignin quality between pulp mill sources — driven by differences in wood species, pulping chemistry, and extraction technology — creates formulation challenges for end-users, constraining adoption rates in precision applications such as carbon fiber spinning and pharmaceutical excipients.

Declining demand in certain legacy application areas, including photographic films and traditional industrial binders, has historically created revenue displacement that tempers net market growth. However, the aggregate impact of these legacy declines is being more than offset by emergent bio-economy applications through 2033.

The competitive landscape of the Kraft Lignin Products Industry Market is characterized by integrated pulp and paper conglomerates with lignin valorization divisions, specialized biochemical producers, and emerging bio-refinery companies. Key participants include:

Borregaard Lignotech: A global leader in lignin-based specialty chemicals, Borregaard operates one of the world's most advanced lignocellulosic bio-refineries in Sarpsborg, Norway, producing a broad portfolio of lignosulfonate and kraft lignin derivatives for markets spanning construction, agriculture, and animal feed.

Domtar Corporation: A major North American integrated pulp and paper company, Domtar has developed commercial kraft lignin extraction capabilities at its Plymouth, North Carolina facility, marketing lignin under the BioChoice brand for use in carbon products, polymers, and energy applications.

Innventia Group: A Swedish research and innovation organization, Innventia has been instrumental in developing lignin fractionation and carbon fiber precursor technologies, operating as a technology enabler and licensor to commercial producers.

NIPPON PAPER INDUSTRIES CO LTD: One of Japan's largest paper manufacturers, Nippon Paper has invested in lignin valorization as part of its broader biomass business strategy, targeting Asian markets with lignin-based adhesives and functional chemicals.

Rayonier Advanced Materials: A specialty cellulose producer with lignin co-product capabilities, Rayonier Advanced Materials is pursuing high-value lignin applications in polymers and specialty chemicals as part of its diversification strategy.

Resolute Forest Products: A North American pulp, tissue, and wood products company, Resolute Forest Products generates lignin as a co-product of its kraft pulping operations and is evaluating commercial valorization pathways to improve operational economics.

Stora Enso: A leading renewable materials company headquartered in Helsinki, Stora Enso operates a commercial-scale lignin extraction plant in Sunila, Finland, producing Lineo branded kraft lignin for binder, resin, and carbon applications.

Suzano: The world's largest eucalyptus pulp producer, Suzano holds a strategic advantage in lignin supply volume and feedstock consistency, and is actively developing lignin-to-chemicals pathways through its innovation pipeline.

UPM Biochemicals: A division of UPM-Kymmene, UPM Biochemicals is commercializing bio-based chemicals including lignin derivatives as part of its Beyond Fossils strategy, with operations centered in Germany and Finland.

West Fraser: A diversified North American wood products company, West Fraser's kraft pulp operations generate lignin co-products with increasing focus on valorization opportunities.

WestRock Company: A major packaging and paper solutions company, WestRock's kraft pulp integration positions it as a potential lignin feedstock supplier as valorization economics improve.

Weyerhaeuser Company: A large timberlands and forest products company, Weyerhaeuser is exploring lignin valorization as part of its wood products and cellulose fibers strategy.

January 2024: Stora Enso announced an expansion of its Lineo kraft lignin production capacity at the Sunila mill in Finland, targeting increased supply to European carbon fiber and binder resin customers amid growing bio-based material demand.

March 2024: UPM Biochemicals commissioned additional pilot-scale infrastructure at its Leuna, Germany bio-refinery complex to accelerate the development of lignin-derived functional chemicals, targeting the coatings and adhesives sectors.

June 2024: Domtar Corporation reported advances in BioChoice lignin quality consistency protocols, reducing inter-batch variability to below 5% by key functional group metrics, a milestone that addresses a longstanding barrier to adoption in precision polymer applications.

September 2024: Borregaard Lignotech partnered with a European agricultural inputs company to develop new lignin-based slow-release fertilizer formulations, with field trials conducted across 12 countries in the European Union.

November 2024: Rayonier Advanced Materials released a technical white paper demonstrating lignin-to-carbon-fiber conversion efficiency improvements of 18% relative to 2022 baseline trials, positioning the company as a technical leader in this emerging application.

February 2025: Suzano announced a strategic review of its lignin valorization business, with indications that a dedicated bio-based chemicals subsidiary could be established by late 2026 to pursue external sales of lignin derivatives.

April 2025: The European Commission finalized updated REACH guidance on kraft lignin polymer classifications, reducing regulatory uncertainty and expected to catalyze new product registrations from Q3 2025 onward.

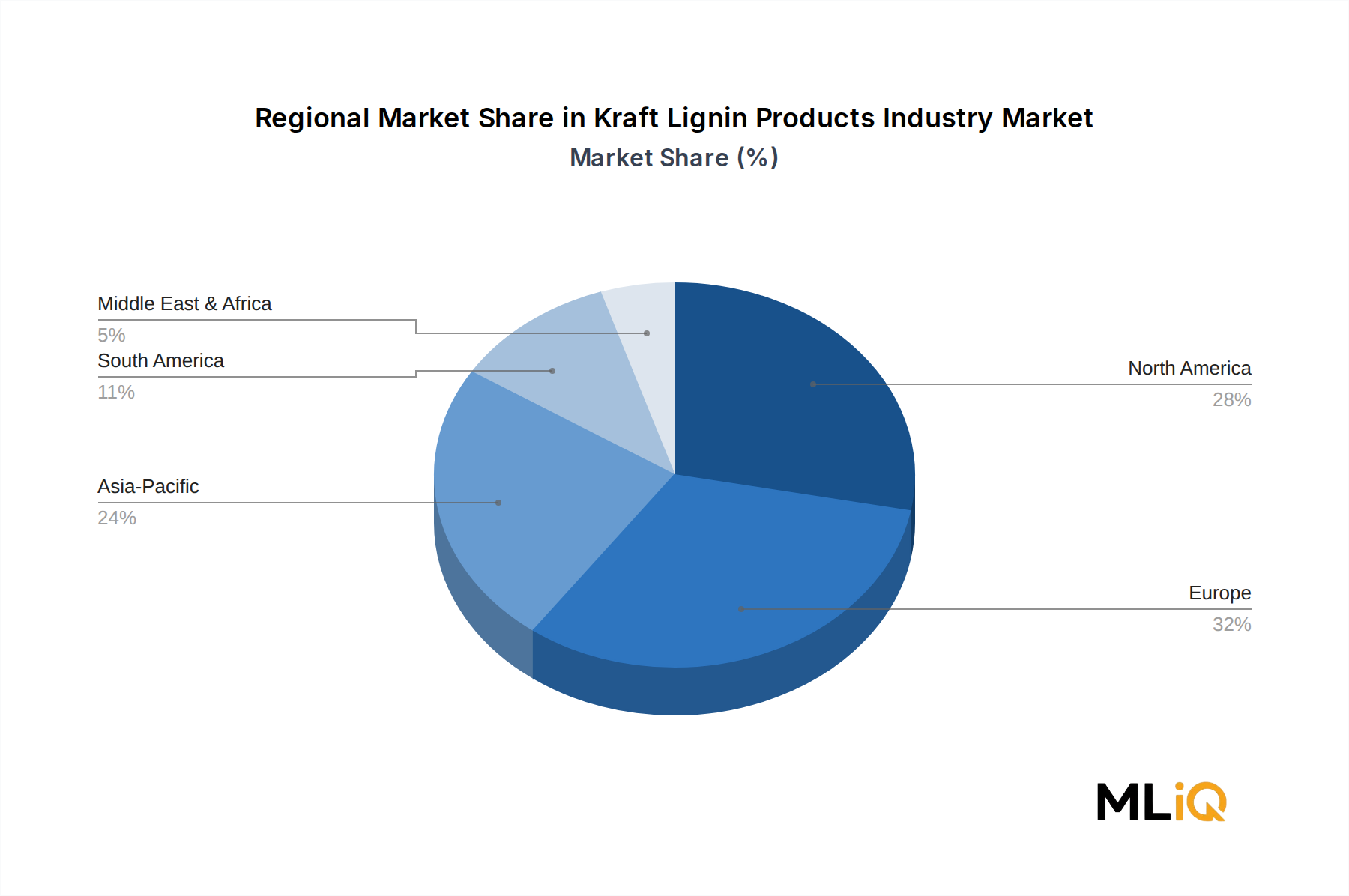

Europe dominates the global Kraft Lignin Products Industry Market, commanding an estimated revenue share of approximately 38–42% of total market value in 2025. The region's leadership is anchored by its dense concentration of kraft pulp mills in Scandinavia and Finland, mature bio-economy policy frameworks including the EU Bioeconomy Strategy and Green Deal, and a sophisticated downstream chemicals industry capable of absorbing lignin-derived intermediates. Germany, Finland, Sweden, and Norway are the four highest-revenue national markets within Europe. The regional CAGR is estimated at approximately 2.1% through 2033, reflecting market maturity and high baseline penetration.

North America represents the second-largest regional market, accounting for approximately 28–32% of global revenue. The United States leads within the region, driven by Domtar's commercialized lignin extraction operations, substantial Department of Energy (DOE) funding for lignin valorization research, and demand from the carbon fiber and wood composites industries. The North American regional CAGR is estimated at 2.3%, with Canada contributing meaningfully through its integrated pulp sector. Mexico remains a nascent contributor.

Asia Pacific is assessed as the fastest-growing regional market, with a projected CAGR of approximately 3.1% through 2033. China's expanding bio-chemical policy agenda, India's growing agricultural chemicals sector, and Japan's longstanding advanced materials industry are the three primary national growth engines. South Korea's carbon fiber ambitions, particularly for wind energy and electric vehicle applications, are creating incremental pull for lignin-based precursor materials. The region's current revenue share stands at approximately 18–22%, with significant upside potential through the forecast period.

South America, led by Brazil — home to Suzano, the world's largest eucalyptus pulp producer — holds approximately 6–8% of global market revenue. Brazil's unique eucalyptus kraft lignin characteristics, particularly its favorable molecular weight profile and low sulfur content relative to softwood kraft lignin, are a differentiating factor for certain specialty applications. Regional CAGR is estimated at 2.8%.

Middle East and Africa currently represent the smallest regional share at approximately 2–4%, with growth driven primarily by South Africa's established pulp sector and increasing investment in bio-based agriculture inputs across the African continent.

The supply chain for the Kraft Lignin Products Industry Market is structurally upstream-dependent on the kraft pulping process, which generates black liquor as a co-product stream containing dissolved lignin. The commercial extraction of kraft lignin from black liquor — most commonly via the LignoBoost or LignoForce precipitation technologies — introduces a series of operational dependencies that shape market supply dynamics.

Wood fiber is the foundational raw material. Pricing and availability of softwood (primarily pine and spruce) and hardwood (eucalyptus, birch, acacia) feedstocks directly influence pulp production economics, and by extension, lignin co-product availability. Global wood fiber prices have exhibited an upward trend since 2021, driven by increased demand for sustainable packaging, bioenergy, and lumber, creating cost pressure on integrated producers. Kraft lignin extraction competes with black liquor combustion for energy recovery within the mill energy balance, meaning that lignin extraction volumes are partially constrained by mill energy optimization decisions rather than solely by market demand.

Sulfur chemistry is a key upstream input. The kraft process uses sodium sulfide and sodium hydroxide as delignification

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.37% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as ; Rising Demand for Carbon Fibers are projected to boost the Kraft Lignin Products Industry market expansion.

Key companies in the market include Borregaard Lignotech, Domtar Corporation, Innventia Group, NIPPON PAPER INDUSTRIES CO LTD, Rayonier Advanced Materials, Resolute forest products, Stora Enso, Suzano, UPM Biochemicals, West Fraser, WestRock Company, Weyerhaeuser Company*List Not Exhaustive.

The market segments include Application.

The market size is estimated to be USD 1072.51 million as of 2022.

; Rising Demand for Carbon Fibers.

Increasing demand for Fertilizers and Pesticides.

Stringent Government Regulations Regarding Tobacco Usage; Declining Demand for Photographic Films.

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Kraft Lignin Products Industry," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Kraft Lignin Products Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.